- The share of homeowners who are” in the money “for a refinance has hit its greatest level in over four years as home loan rates dip to around 6%.

- But less than 1 in 10 qualified house owners have actually re-financed, despite the fact that they stand to conserve cash.

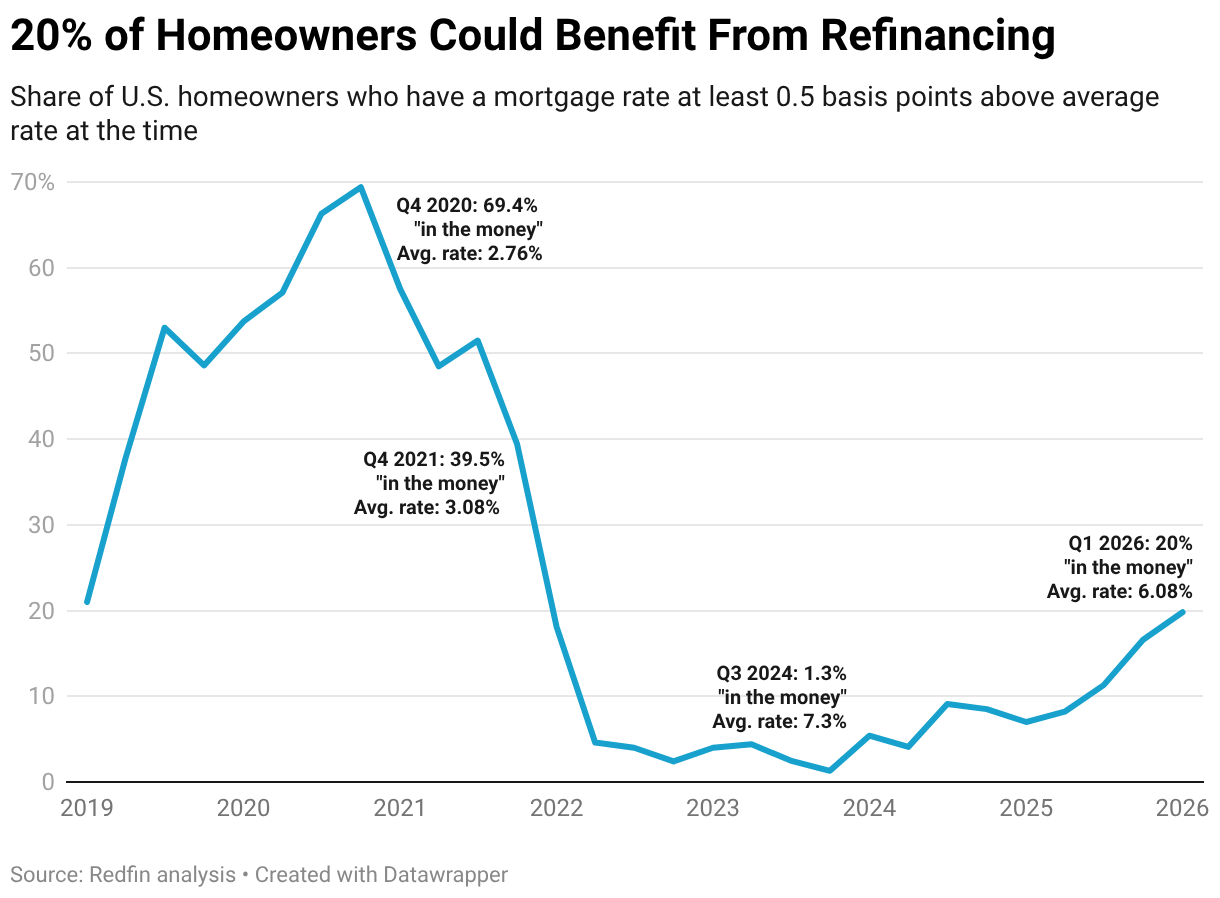

One in 5 (19.8%) U.S. homeowners with a mortgage might conserve money by re-financing to a lower rate, the greatest share in over four years and up from simply 7% a year earlier.

That’s based upon a 6.08% mortgage rate, the average so far this year. A house owner is “in the cash”– indicating they could save money by refinancing– if their current mortgage rate is at least 50 basis points above the fundamental home loan rate; for instance, if they have a 6.5% mortgage rate and the prevailing rate is 6%.

This is according to a Redfin analysis of house owners who could gain from refinancing since current home loan rates are lower than the rate on their existing loan. Throughout this report, when we refer to the share of “property owners “who remain in the cash for a refinance, we mean the share of U.S. mortgage financial obligation that remains in the cash to re-finance. The portion of those loans that were really refinanced(i.e. the take-up rate )is likewise a part of all “in-the-money” U.S. mortgage debt. The current re-finance take-up rate covers the very first quarter of 2026, using a theorized estimation. Please see completion of this report for more on methodology.

There are 2 main factors more homeowners are in the cash for a refinance this year:

- Home mortgage rates fell to 6% in February and early March, the most affordable level in 3 and a half years.

- Home loan rates were elevated above 6% for so long that 21.2% of U.S. homeowners had a rate above 6% since the 3rd quarter of 2025, the greatest share in a decade. That marks the very first time in five years more customers have a rate above 6% than listed below 3%.

State somebody purchased a $500,000 home in October 2023, when rates strike a 20-year high of 7.8%. Their month-to-month home loan payment would have to do with $3,700, assuming a 20% down payment. Refinancing to a 6% rate would bring the payment down to about $3,200, saving $500 each month. If the homeowner pays $10,000 in re-finance costs, it would take less than two years– 20 months– for the monthly cost savings to pay for the charges.

The last time this numerous property owners remained in the money for a refinance was the end of 2021, when mortgage rates balanced 3.08% and roughly two in five (39.4%) would have gained from refinancing. The in-the-money share peaked at nearly 70% at the end of 2020, when mortgage rates plunged to 2.76% throughout the pandemic.

Regardless Of Prospective Savings, Just 9% of Qualified Debtors Have Re-financed

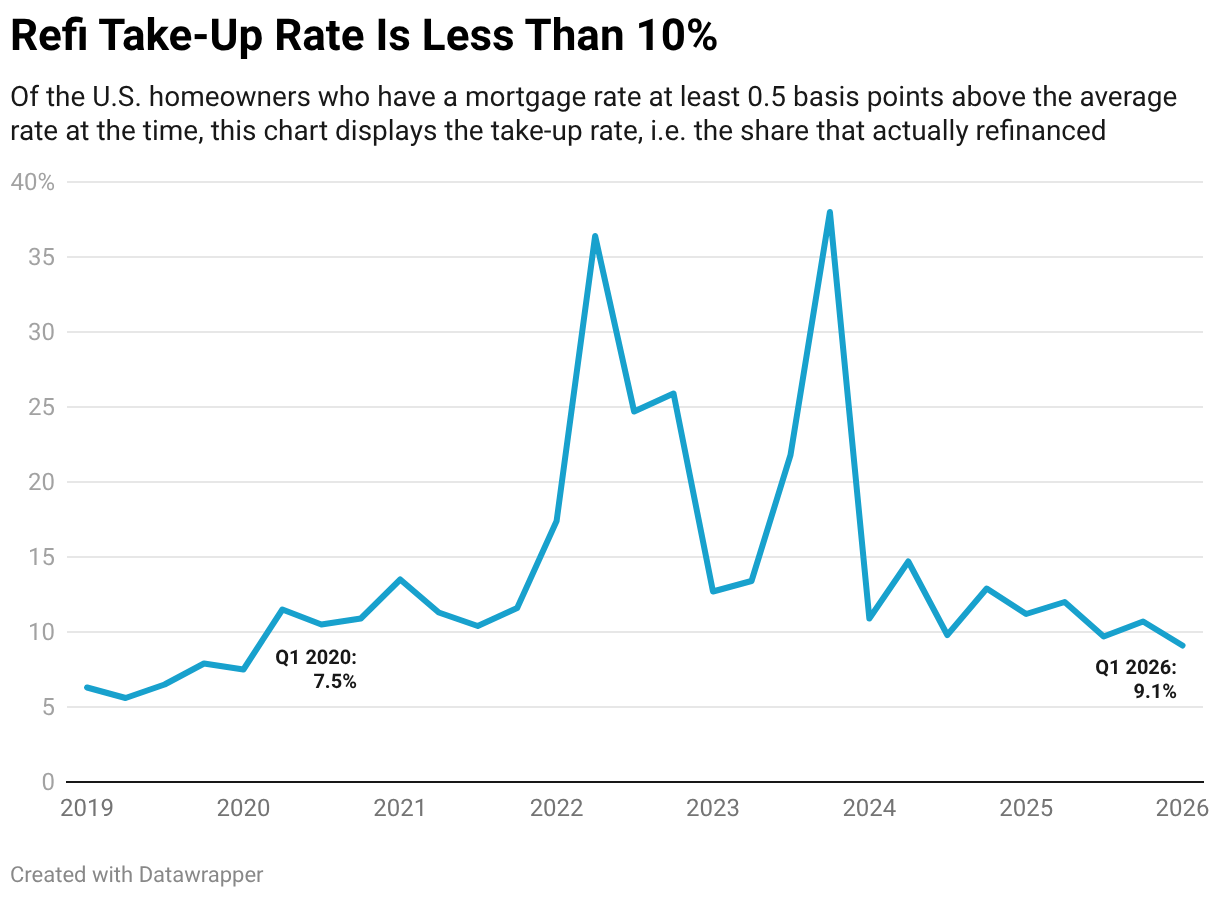

Just 9.1% of homeowners who might save cash by re-financing to today’s typical rate (6.08%) have actually done so, as of the very first quarter of this year. That’s the lowest “take-up rate” for property owners who could take advantage of refinancing because the start of 2020.

Zooming out to all mortgaged house owners in the U.S., 1.8% have actually re-financed so far in the very first quarter.

“For homeowners who remain in the cash, re-financing now might meaningfully lower monthly payments and overall interest expenses over the life of the mortgage,” said Costs Banfield, chief company officer at Rocket. “Even a modest rate decrease can add up to huge savings, helping free up cash, develop equity much faster, or better weather condition future monetary unpredictability. Property owners may also think about whether refinancing might have benefits aside from putting money back in their pocketbooks each month. For example, they might think about combining debt or changing their loan type. Some people make the most of lower rates to alter the length of their loan and pay it off quicker while keeping essentially the same month-to-month payment.”

While re-financing to a lower rate might conserve money in the long run for numerous property owners, there are numerous reasons so couple of individuals are in fact doing it:

- Waiting for lower rates. Home loan rates can shift rapidly; people may be hesitant to lock in a rate if they believe rates will dip further in the near future, even if they might conserve money now. However homeowners should likewise think about that rates might return up, which they can re-finance once again if rates fall significantly more.

- Limited awareness. Not all customers routinely examine home loan choices; lots of may just be uninformed they might conserve. House owners can save cash by paying attention to modifications in home loan rates.

- Closing costs and costs. While refinancing expenses can appear big on paper, many property owners will be able to pay them off quickly with the amount they’re saving money on interest monthly.When mortgage

rates were sitting at record lows throughout the pandemic, dipping listed below 3% for much of 2020 and 2021, the take-up rate hovered around 1 in 10 qualified debtors per quarter. The take-up rate peaked at 13.5% in the first quarter of 2021, when the typical rate was 2.88%.

Today’s take-up rate resembles what it was during each private quarter of 2020 and 2021. However taking a look at those eight quarters together, more than half of in-the-money customers re-financed throughout that time.

It’s likewise worth keeping in mind that the take-up rate leapt to 38% in the fourth quarter of 2023, when rates were at a two-decade high. That’s because simply 1.3% of house owners remained in the money for a refi; the real number of homeowners who re-financed is much lower than the 38% suggests.

House Owners Left Enormous Amounts of Potential Cost Savings Untapped

Americans re-financed an estimated $223 billion worth of home loans in the very first quarter.

But they might have refinanced $2.24 trillion worth of home loans. That $2.24 trillion represents the total loan value of the 90.9% of in-the-money homeowners who didn’t re-finance.

Approach

This is from a Redfin analysis of house owners who could gain from refinancing because present home mortgage rates are lower than the rate on their existing loan. Throughout this report, when we describe the share of “property owners” who are in the money for a refinance, we imply the share of U.S. home mortgage financial obligation that remains in the cash to re-finance. The portion of those loans that were in fact refinanced (i.e. the take-up rate) is also a part of all in-the-money U.S. home mortgage financial obligation. Rate distribution and overdue home mortgage balance information is since the third quarter of 2025, the most recent information available, while values for the fourth quarter of 2025 and the first quarter of 2026 are derived using direct extrapolation based on the trend from Q4 2023-Q3 2025. Re-finance volume information is available through the fourth quarter of 2025; re-finance volume for the very first quarter of 2026 is from a Fannie Mae housing forecast.

Mortgage-rate data is based on average 30-year fixed mortgage rates from Federal Reserve economic data. Mortgage-rate circulation and total overdue home loan balance data is from the Federal Real estate Financing Firm’s National Home mortgage Database.

The percentage of home mortgages that are in the cash is determined utilizing a consistent distribution assumption within each rate container. The home loan rate distribution data offers five pails: 6.0%– 8.0%, 5.0%– 5.9%, 4.0%– 4.9%, 3.0%– 3.9%, and 2.5%– 2.9%. To determine the in-the-money portion, we: 1) Identify the threshold rate (30-year rate + 0.5%), and 2) Identify which rate buckets are completely above, entirely listed below, or partially converge the threshold. For buckets completely above the limit, we added 100% of home loans because bucket to the in-the-money total. For buckets partially converging, we used uniform distribution to calculate the proportion above the limit. Buckets totally below are omitted from the estimation.