According to brand-new data by Yardi Kube, the U.S. coworking sector posted another year of strong growth, strengthening its transition from a niche work environment option into a core component of the modern-day office market.

In between January 2025 and January 2026, the national coworking footprint grew to 8,973 locations, up from 7,776 a year earlier– a 15% boost. Overall versatile office stock likewise climbed up 16% to more than 161 million square feet, adding roughly 22.5 million square feet to the market.

While headline development stays robust, industry experts state the underlying information indicate a much deeper structural shift. What began as a workspace solution mainly for start-ups and freelancers has actually increasingly ended up being embedded in enterprise realty techniques, as corporations, remote teams and fast-growing business seek greater versatility in handling office portfolios.

“The conversation has shifted from ‘Should we utilize coworking?’ to ‘Just how much versatile area do we require?'” Yardi Kube scientists noted, reflecting a broader advancement in workplace technique.

Operator Development Signals Continued Market Entry

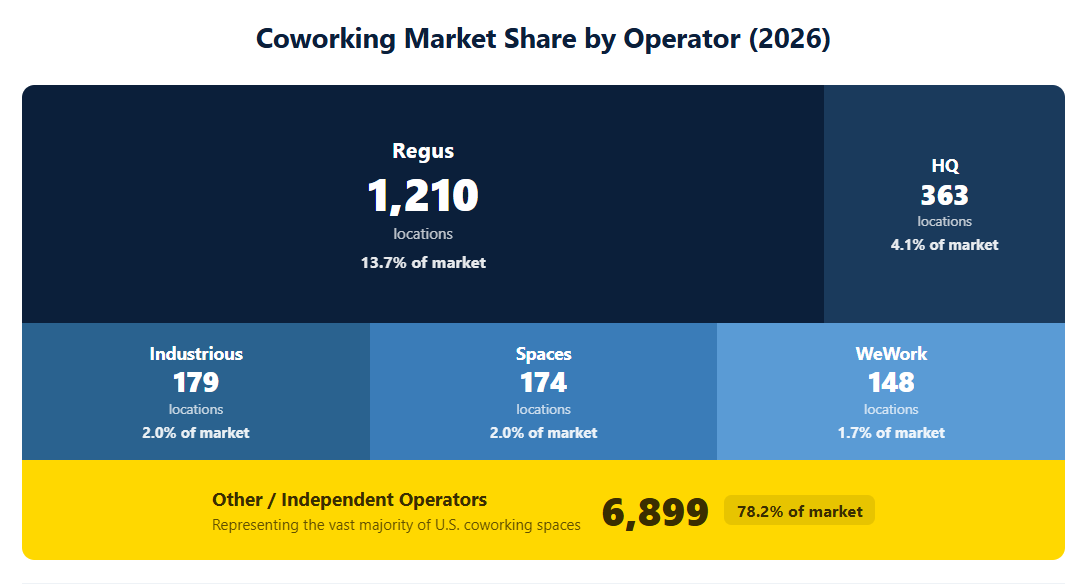

The variety of coworking operators broadened dramatically over the past year, with the nationwide operator base increasing from 3,729 to 4,338 unique operators, a net gain of 609 brand-new entrants, states Yardi Kube.

The increase underscores continued financier and entrepreneurial interest in the flexible workspace model, even as bigger incumbents refine their portfolios. The market’s largest operator increased its network to 1,210 areas, adding 164 brand-new websites, while numerous established brand names maintained or a little lowered their footprints as part of wider optimization efforts.

Taken together, the information recommends a market experiencing both expansion and maturation, with big international brand names scaling operations while smaller operators continue entering local and local markets.

Major City Areas Lead Expansion

Yardi Kube reports development throughout significant U.S. cities stayed broad-based, spanning conventional entrance cities and high-growth Sun Belt markets.

Los Angeles included 50 brand-new coworking places, bringing the overall to 343 websites, a 17% year-over-year boost.

Chicago recorded the biggest place gain among major markets, including 64 locations, a 24% jump, together with nearly 2 million square feet of extra area.

Dallas-Fort Worth continued its growth with 45 new places and 1.53 million square feet included, while Washington, D.C. grew by 28 places and almost 904,000 square feet.

Manhattan remained the largest coworking market in the nation by square video, with more than 12.4 million square feet of versatile office following the addition of 31 places.

Other significant growths consisted of Atlanta, which included 47 areas and more than 1 million square feet, and Boston, where 52 brand-new areas pushed total stock up 25% year over year.

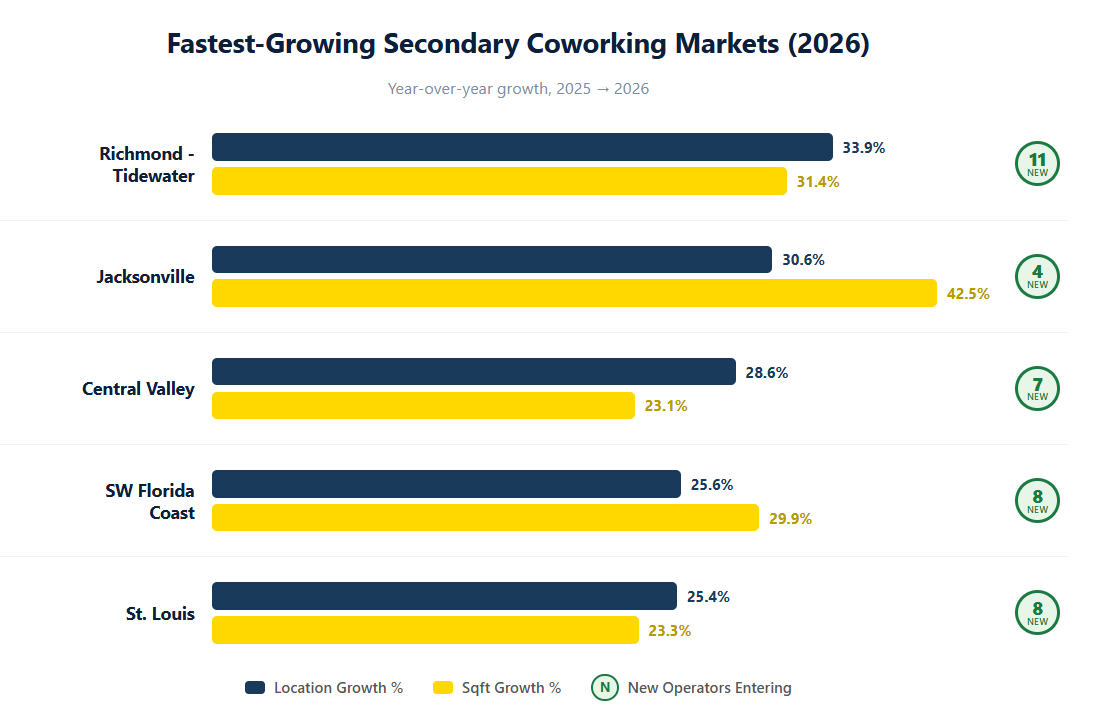

Secondary Markets Post the Fastest Development

While significant cities continued to expand, several smaller metros taped the most fast gains.

Richmond-Tidewater led the nation with a 34% boost in coworking locations, adding 20 new sites and more than 300,000 square feet of flexible workspace.

Jacksonville posted the biggest square-footage growth nationally, expanding its coworking footprint by over 241,000 square feet, a 43% increase.

In other places, California’s Central Valley recorded a 29% increase in coworking areas, while the Southwest Florida Coast region saw a 26% increase alongside more than 167,000 square feet of new space. St. Louis completed the fastest-growing markets with a yearly boost of 25% in place count.

The surge in secondary markets highlights how versatile office need is spreading out beyond standard coastal centers into mid-size local economies.

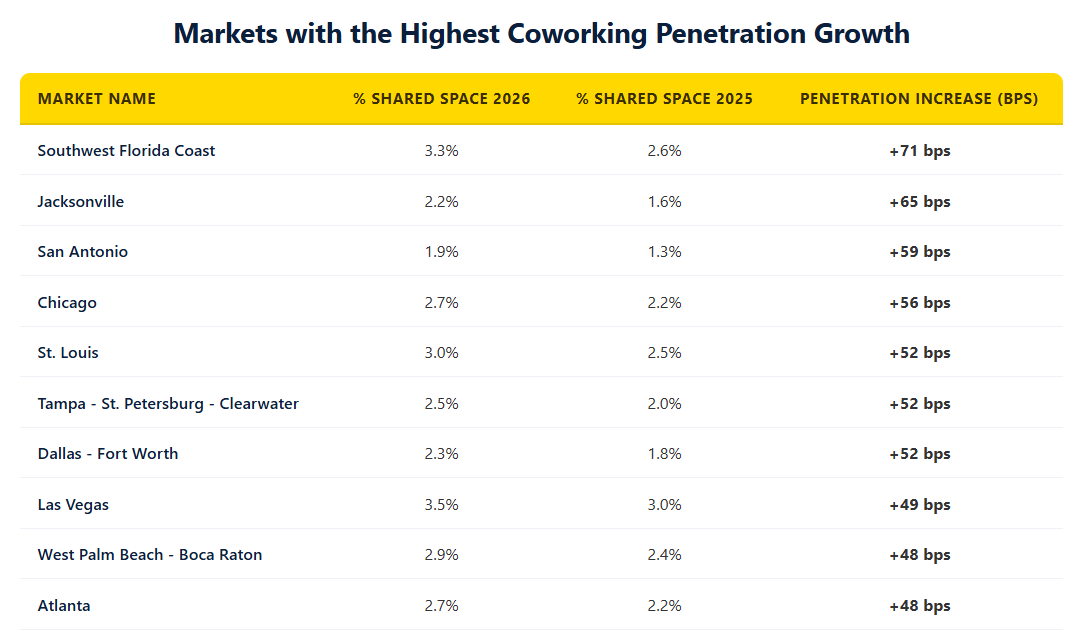

Coworking Penetration Continues to Increase

Coworking’s share of the wider U.S. office market likewise edged higher, says Yardi Kube.

Flexible work space represented 2.2% of overall U.S. office stock at the start of 2026, up from 2.0% a year previously– indicating roughly one out of every 45 square feet of workplace nationwide is now coworking.

At the metro level, penetration rates differed considerably.

The Southwest Florida Coast recorded the biggest boost, climbing from 2.6% to 3.3% of office inventory. Las Vegas posted the highest general penetration among major markets at 3.5%, while Chicago, St. Louis, Dallas-Fort Worth, and Tampa-St. Petersburg-Clearwater each saw gains of approximately half a percentage point over the year.

Florida markets continued to stand apart as particularly strong adopters, with West Palm Beach-Boca Raton increasing to 2.9% penetration and Tampa-St. Petersburg-Clearwater reaching 2.5%.

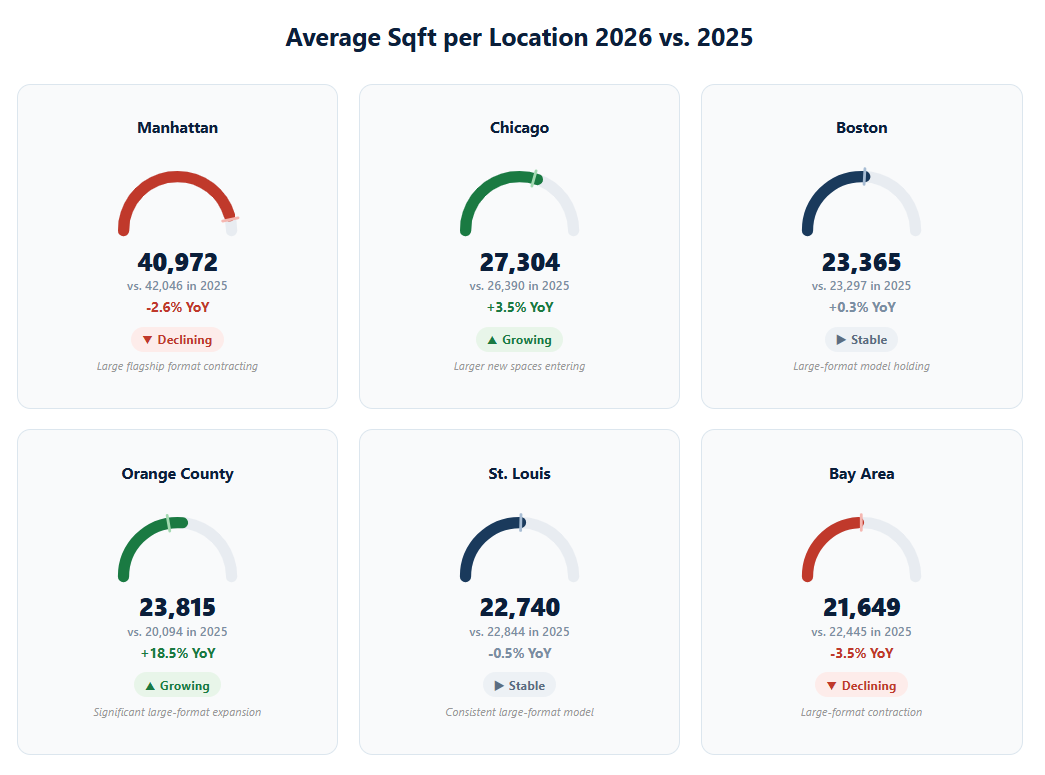

Market Maturity Emerges in Place Size Patterns

Typical coworking location sizes also revealed shifts in market dynamics.

Manhattan maintained the biggest typical coworking area size in the U.S. at approximately 40,972 square feet, regardless of a small year-over-year decrease.

On The Other Hand, Orange County, California, saw one of the most significant boosts, with typical area size rising 18.5% to almost 24,000 square feet, recommending the development of larger, enterprise-focused coworking hubs.

In contrast, the San Francisco Bay Area experienced a 3.5% decline in typical website size, possibly showing a shift towards smaller sized boutique operations or combination of larger areas.

Other fully grown markets, consisting of Boston and St. Louis, showed very little modifications in average location size, indicating relatively stable operating designs.

Flexible Work Area Goes Mainstream

Market observers progressively view the coworking sector as an established part of the commercial property landscape instead of a cyclical pattern.

“2025 represents progress for the market,” said Peter Kolaczynski, Director of Yardi Research Study. “Progress with thoughtful, constant development and progress in educating occupiers about the advantages that coworking and serviced office space provide.”

With business adopting hybrid work techniques and companies prioritizing versatility in unpredictable economic conditions, the expansion of coworking area appears likely to continue.

Yardi Kube’s most current information recommends the sector’s development is entering a brand-new stage– one where flexible workspace is no longer an alternative to traditional workplaces, however an incorporated layer of office infrastructure within the more comprehensive workplace market.