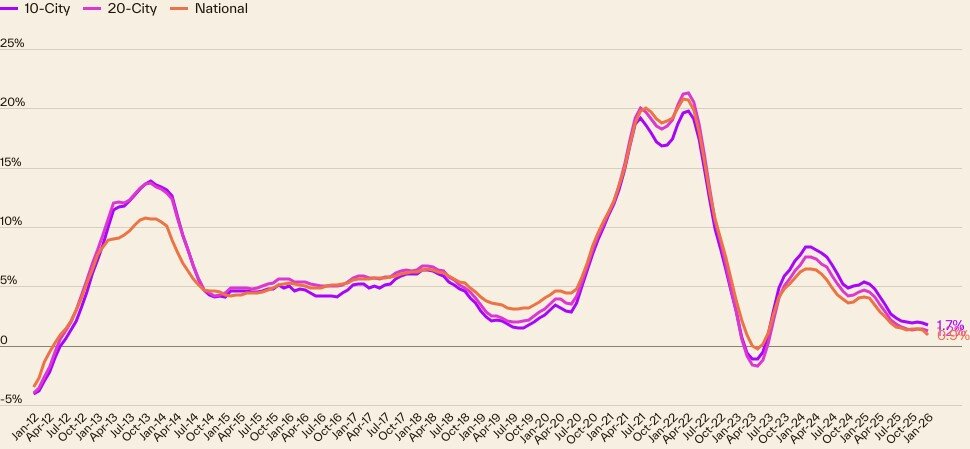

National prices rose simply 0.9% in January from a year earlier, marking a noteworthy deceleration from December and underscoring a market struggling to fix up raised home values with stagnant buying power. On a regular monthly basis, rates slipped 0.11%– a decline steeper than common seasonal patterns– highlighting softer need as buyers stay sidelined.

“We’re successfully in a low-velocity environment where both sales and price development are constrained,” said Thom Malone, principal economic expert at Cotality. “Unlike prior recessions connected to broader financial tension, real estate today leads the cycle. The marketplace is waiting for earnings and financing conditions to capture up.”

Regional Divergence Deepens

Large urbane markets continue to exceed the national average, though momentum is fading. The 10-city and 20-city composites published annual gains of 1.7% and 1.2%, respectively, however underneath the surface area, regional variations are widening.

In the Northeast and Midwest, New York City and Chicago led annual rate development, rising 4.9% and 4.6%. By contrast, previously high-flying Sunbelt markets are losing steam as inventory constructs. Tampa and Denver published the steepest decreases, each falling more than 2% from a year previously.

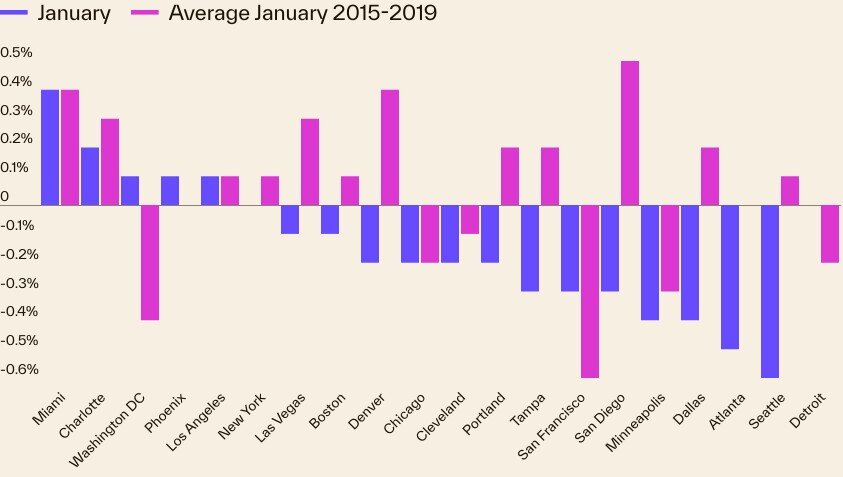

Monthly figures tell a similarly irregular story. Miami taped a modest 0.4% boost, while Charlotte and Washington, D.C. also eked out gains. On the other hand, Seattle and Atlanta saw rates fall by a minimum of 0.5%, reflecting weaker near-term need.

High-end Sector Shows Cracks

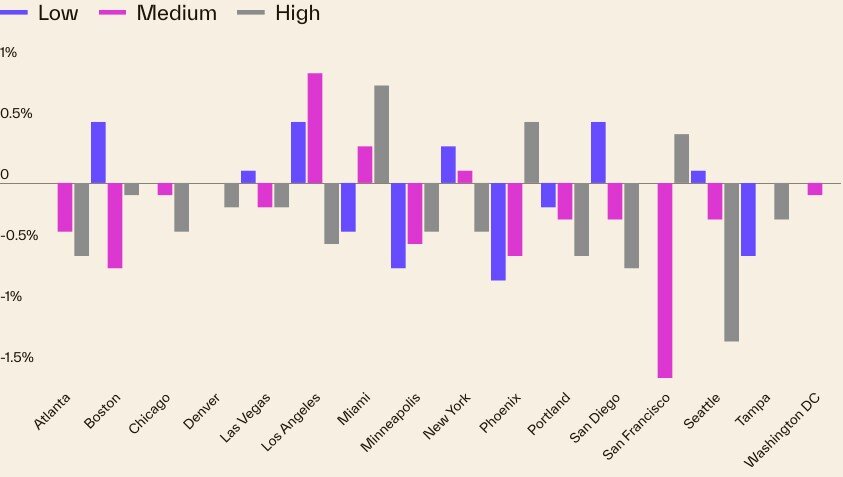

Cost pressures are increasingly focused at the top end of the market. High-tier homes decreased 0.25% in January throughout major cities, compared to a more modest 0.05% dip for lower-priced homes. The divergence suggests that upscale buyers– more sensitive to financing costs and market volatility– are pulling back faster than entry-level buyers.

Standoff Continues Into Spring

The housing market stays specified by a stalemate in between buyers and sellers that took hold through 2025. Homeowners, reluctant to give up low mortgage rates and collected equity, have resisted price cuts. At the exact same time, prospective buyers continue to face extended affordability, limiting transaction volumes and dampening cost momentum.

That dynamic has resulted in rising stock, suppressed sales, and broadly flat rates trends– conditions most likely to continue into the early months of the spring selling season.

The next stage depends upon which side yields initially. A wave of cost reductions from sellers could press valuations, while enhanced funding conditions or more powerful earnings growth might draw purchasers back into the market.

For now, the most likely result depends on between: a steady thaw marked by modest rate gratitude and continued friction, instead of a definitive rebound or slump.

< img src="https://www.worldpropertyjournal.com/assets_c/2026/04/2026%20national%20home%20price%20data%2C%20S%26P%20Cotality%20-%20Chart%203-thumb-855x477-36610.jpg" alt="2026 national home rate information, S&P Cotality - Chart 3. jpg"/ >

Sign Up Free|The WPJ Weekly Newsletter Pertinent realty news.Actionable market intelligence.Right to your inbox every week.

Property Listings Showcase

Property Listings Showcase