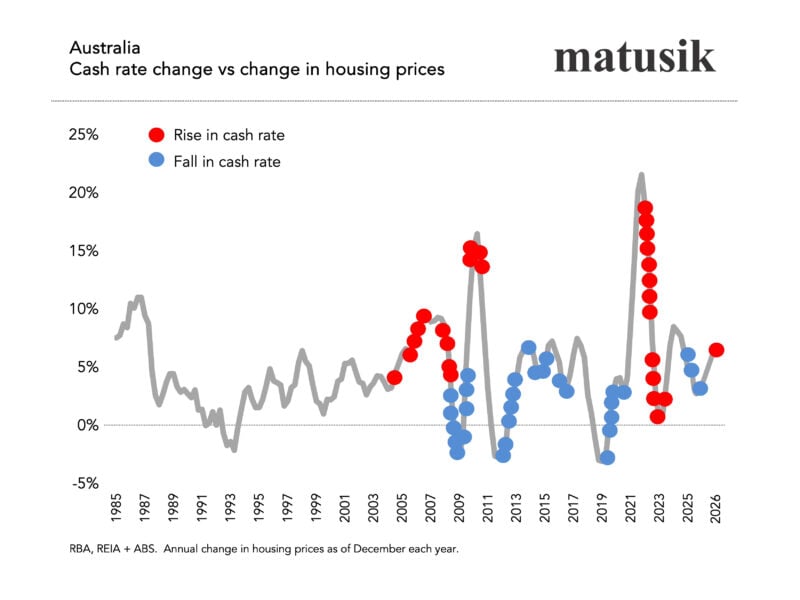

< img src =" https://cdn.propertyupdate.com.au/wp-content/uploads/2022/07/interest-rates.jpg" alt= "" > Among the more relentless concerns I get asked at recent speaking gigs during the Q+A that follows by babble, is” When the RBA lifted rates 13 times across 2022 and 2023, why didn’t real estate crash?.”

The chart recommends it ought to have has more effect.

Historically, rising cash rates sluggish dwelling rates. Sometimes greatly. Yet post-Covid, after a preliminary wobble, housing values pushed higher again.

< img src=" https://cdn.propertyupdate.com.au/wp-content/uploads/2026/03/Australia-cash-rate-change-vs-change-in-housing-prices-800x600.jpg" alt=" Australia Money Rate Change Vs Modification In Housing Costs "width=" 800

” height =” 600 “/ > The response isn’t a secret. It’s money. Between 2020 and 2022, Australia experienced the largest monetary expansion in its contemporary history.

Quantitative relieving, massive federal government bond purchases, financial transfers, organization grants, wage subsidies and state stimulus integrated to provide near $1.2 trillion in policy assistance across the economy.

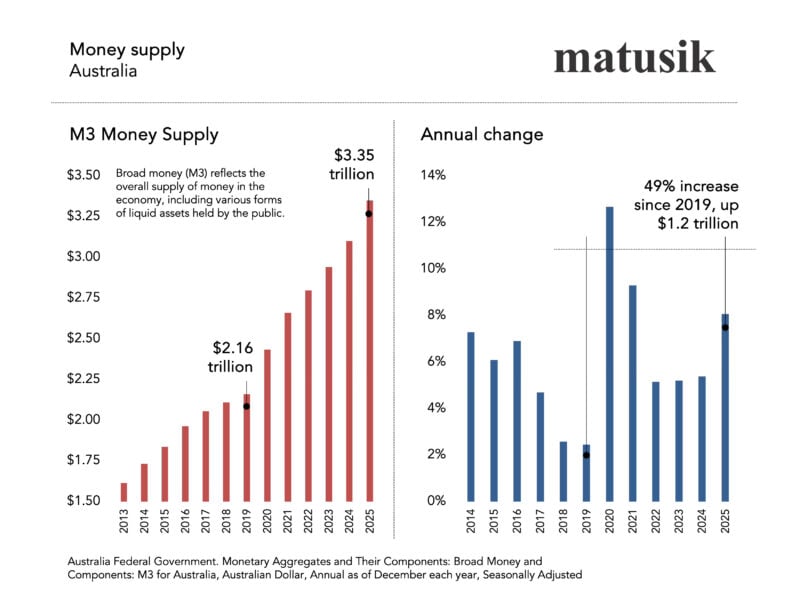

Over the very same duration, Australia’s broad money supply (M3) increased from around $2.16 trillion in 2019 to roughly $3.35 trillion today – an increase of roughly $1.2 trillion, or about 55%.

That is an amazing lift in liquidity in an extremely short time period.

For context, Australia’s yearly GDP is approximately $2.64 trillion, currently growing at around 2.1% per year.

Put more merely: Australia’s cash supply is now majority again as large as it was pre-Covid, and more than one-third of all Australian dollars around today were created in the previous 5 years.

Stop and read that last sentence once again.

< img src =" https://cdn.propertyupdate.com.au/wp-content/uploads/2026/03/Money-supply-Australia-800x600.jpg" alt =" Cash Supply Australia" width=" 800" height=" 600"/ > And you can not pour that much liquidity into our housing system and anticipate

no distortion. Yes, the preliminary Covid action was warranted. Pandemic panic demanded circuit breakers.

However emergency settings didn’t simply relax, they changed, and big time.

Government spending rose structurally. Every social problem now has an automatic funding option, even if truly simply requires some difficult love. Every constituency has actually ended up being a spending plan line item.

Naturally we aren’t alone.

Throughout innovative economies, financial settings stay elevated compared to the pre-pandemic standard.

Public balance sheets are larger, structural deficits wider and political appetite for restraint extremely restricted, more like non-existent, if you ask me.

Rates of interest increases have tightened the margin, however they haven’t completely balanced out the magnitude of the earlier and continuing liquidity surge.

And real estate sits downstream of this.

The excess liquidity did 3 things.

Initially, it permanently lifted family balance sheets. Savings buffers surged. Deposits swelled. Even as rates rose, lots of debtors had cushions.

Second, it embedded greater small earnings. Wage development accelerated method above performance gains. Asset inflation enhanced viewed wealth.

Third, policy actively supported real estate need. Since 2020, simply over 265,000 * Australians have entered home ownership by means of federal deposit guarantee schemes. That has demand advanced. It narrowed the deposit difficulty and pulled purchasers into the marketplace earlier than would otherwise happen. This activity misshapes the real estate cycle.

Layer that atop record migration and weak new housing supply (specifically in 2023 and 2024), and you get resilience not collapse.

However here’s the uncomfortable bit.

This current development rhythm is unlikely to repeat.

Inflation is showing sticky. And for mine will remain so in a more fractured international order – regional trade blocs, supply chain duplication, defence spending and now spreading out abroad conflicts – adds to structural costs.

Deglobalisation is inflationary. Energy transition expenses are inflationary. Ageing demographics are inflationary when you do not have the right policy settings.

That most likely ways rates of interest stay higher for longer than history taught us to anticipate.

Meanwhile, debt levels across families, developers and federal governments are materially greater. When leverage increases, margin for error falls.

Recent real estate rate development appears less like the start of a new cycle and more like the lagged result of unmatched stimulus still working its way through the economy.

Monetary growths seldom raise efficiency; they mostly inflate possession worths and bring forward demand.

The risk

The threat for real estate investors – and especially new housing designers – is presuming the anomaly is the standard.

Greater building costs. Thinner feasibility. Tighter credit evaluation. Greater sales danger.

We are not returning to the ultra-cheap money era at any time quickly. And without that tailwind, real estate returns revert toward earnings growth, not liquidity development.

That’s an extremely various formula than where things have actually been at over the previous five or two years.

The post-Covid housing upswing wasn’t magic. Pump adequate money into an economy and asset prices will respond.

The question now isn’t why prices didn’t fall. It’s what happens when the sugar hit finally wears off.

< img alt="Michael Matusik Bright" src="https://propertyupdate.com.au/wp-content/uploads/2019/03/cropped-Michael-Matusik-bright-148x148.jpg" height="148" width="148"/ > About Michael Matusik Michael is director of independent property advisory Matusik Property Insights. He is independent, perceptive and to the point; has actually helped over 550 brand-new residential developments concern fruition and composes his informative Matusik Missive

< img alt="Michael Matusik Bright" src="https://propertyupdate.com.au/wp-content/uploads/2019/03/cropped-Michael-Matusik-bright-148x148.jpg" height="148" width="148"/ > About Michael Matusik Michael is director of independent property advisory Matusik Property Insights. He is independent, perceptive and to the point; has actually helped over 550 brand-new residential developments concern fruition and composes his informative Matusik Missive