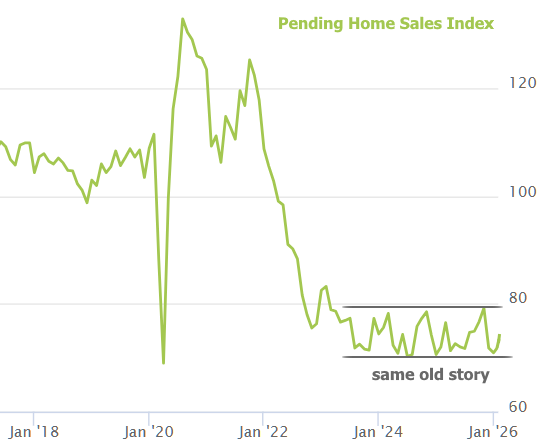

Brief variation: The Pending Home Sales Index stays in the same low, narrow, sideways range that’s been undamaged for 3 years. The bright side is that there’s been a trustworthy flooring. The bad news is that the top of the range lines up with the historical lows seen in 2010 (April 2020 regardless of).

Longer version: Pending home sales moved decently higher in March, breaking from current softness however staying within a fairly controlled range. The National Association of Realtors’ Pending Home Sales Index (PHSI) increased 1.5% month over month while decreasing 1.1% compared with the exact same time in 2015.

The monthly gain recommends some underlying demand durability, even as home mortgage rates remained raised. Nevertheless, on a yearly basis, contract activity continues to show a market still working through price restraints and uneven purchaser participation.

NAR Chief Economist Lawrence Yun kept in mind that, “Agreement signings increased in March despite higher mortgage rates, pointing to pent-up real estate need … A greater supply of stock will assist translate that demand into more home sales.” He included that demand remains particularly rate-sensitive amongst novice and more youthful purchasers, highlighting the requirement for additional supply in smaller sized, more budget-friendly homes.

Regional efficiency stayed blended. The Northeast and South posted month-to-month gains, while the Midwest and West saw declines. On a year-over-year basis, only the South tape-recorded an increase, with the remaining areas continuing to trend lower– highlighting continuous local divergence in housing activity.

Regional Breakdown (Month-Over-Month)

- Northeast: +4.4%

- Midwest: − 1.3%

- South: +3.9%

- West: − 2.6%

Regional YoY Modification

- Northeast: − 6.5%

- Midwest: − 3.1%

- South: +2.3%

- West: − 1.7%