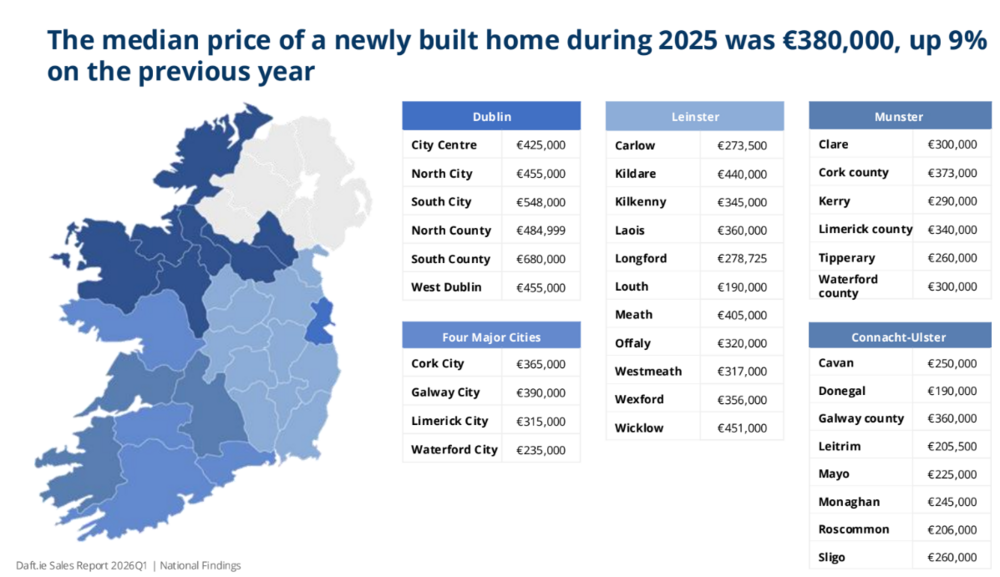

New data from Daft.ie shows nationwide asking costs rose 3.7% in the year to March, marking the weakest yearly increase since late 2023. The typical listed price for a three-bedroom semi-detached home stood at EUR435,000 in the first quarter, leaving values about 42% above pre-pandemic levels and still decently listed below their mid-2000s peak.

The small amounts is also apparent in closed sales. Deal rates increased 5.6% year-on-year through March– also the slowest development rate in over two years– while quarterly gains stalled, signifying a market losing momentum after a prolonged run-up. The gap between asking and final list price, a crucial procedure of competition, narrowed to 5.8%, showing less aggressive bidding conditions.

The shift, however, is far from uniform. A pronounced urban-rural divide is emerging, with stabilization taking hold first in cities where supply has begun to recuperate.

In Dublin, asking costs increased simply 2.5% from a year earlier, and deal rates edged lower in the first quarter. Other major metropolitan centers saw a lot more controlled development, with sticker price up just 0.7%. Increased schedule– particularly in the second-hand market– is alleviating pressure on purchasers and tempering cost gains.

Outside the cities, the picture remains markedly various. Costs continue to climb up at a much faster clip, rising roughly 5% in Leinster and more than 8% in Connacht-Ulster, where restricted real estate stock continues to fuel competitors.

Supply stays the main fault line. Simply over 10,100 second-hand homes were on the market nationwide at the start of March, up 6% from a year earlier but still less than half the common pre-pandemic level. While inventory in Dublin has rebounded closer to historical standards, lacks stay acute throughout much of the nation.

The result is what financial experts significantly refer to as a “two-speed” housing market: cooling conditions in metropolitan hubs contrasted with relentless inflation in supply-constrained regions.

“Price development is plainly slowing, however the change is uneven,” said Ronan Lyons, a financial expert at Trinity College Dublin and author of the report. “Improving schedule in cities is alleviating competition, particularly in Dublin, but outside those areas supply stays far below regular levels, sustaining upward pressure on rates.”

That imbalance underscores a much deeper structural problem. In spite of modest gains in listings, Ireland continues to deal with a substantial real estate deficiency. Analysts estimate that building levels would require to approximately double across private, rental and social real estate sectors to bring back long-term stability.

For now, the data suggest the marketplace is transitioning instead of turning– moving from broad-based cost velocity to a more selective, supply-driven landscape where location progressively determines results.