A new survey from CBRE Group reveals 57% of local investors plan to broaden their property holdings this year, reflecting a stable shift away from the protective strategies that dominated the past 2 years. Net purchasing intents– a closely watched gauge of sentiment– increased to 17%, continuing a multi-year climb from 13% in 2025 and just 5% in 2024.

The enhancing outlook is being underpinned by a combination of firmer occupier need, a thinning advancement pipeline and gradually loosening up financing conditions. Together, those elements are prompting investors to re-enter the market with a sharper concentrate on assets efficient in providing long lasting rental development.

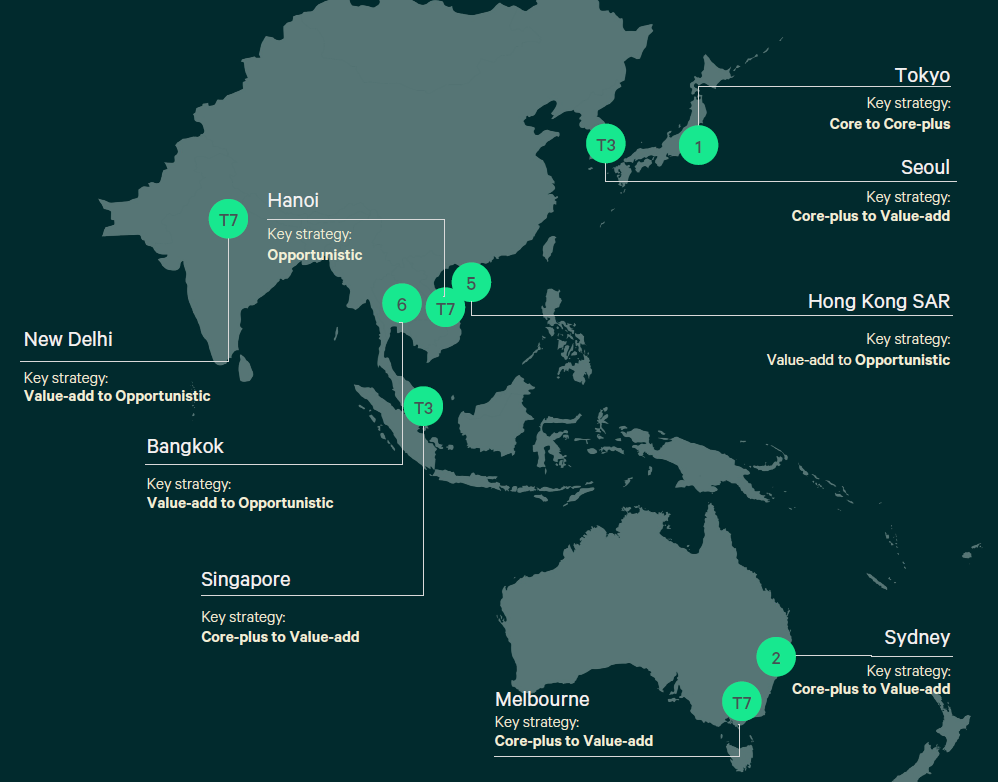

Workplace homes have emerged as the leading target for capital implementation for the very first time in six years, overtaking commercial and logistics properties that had actually controlled allowances throughout the pandemic-era e-commerce boom. The renewal is most pronounced in gateway markets such as Tokyo, Sydney and Singapore, where high occupancy levels and limited brand-new supply are supporting rent development and stabilizing assessments.

Cross-border capital continues to gravitate toward Tokyo, which maintains its position as the area’s most preferred investment destination for a seventh successive year. Financiers are drawn by relatively low borrowing expenses and consistent income streams. Sydney ranks next, followed by Singapore and Seoul, while Hong Kong has re-entered the top tier amid a pickup in activity connected to property conversions and hotel repositioning.

While workplaces lead, commercial and logistics possessions remain securely in focus, with roughly one-fifth of financiers prioritizing the sector amidst expectations that brand-new supply will lessen after 2027. Structural need linked to e-commerce continues to provide long-term support. Meanwhile, rental real estate– especially build-to-rent– has actually gotten traction, alongside rising institutional interest in information centers as digital facilities ends up being increasingly ingrained in portfolio methods.

Investment techniques are also developing. Core-plus and value-add strategies now control, accounting for more than 60% of financier preferences, as buyers position for rental-driven benefit rather than counting on distressed prices. Opportunistic plays have lost favor, showing a decrease in forced sales and persistently high building and construction and labor expenses.

Property financial investment trusts throughout Asia-Pacific are expected to be among the most active buyers this year, while personal financiers might start cutting holdings acquired during earlier market dislocations.

Despite the enhancing tone, risks stay. Financiers cite increasing building and labor expenditures as the most considerable headwind, overtaking rates of interest for the very first time. Geopolitical uncertainty continues to weigh on sentiment in key markets such as China and India, while shifting central bank signals in Japan and Australia have actually reestablished concerns about the path of borrowing costs.

However, the wider trajectory points toward a determined healing– one defined less by enthusiasm and more by disciplined capital deployment into top quality properties with clear, income-generating potential.