In This Article BiggerPockets members have actually spoken. Their verdict: mindful optimism.

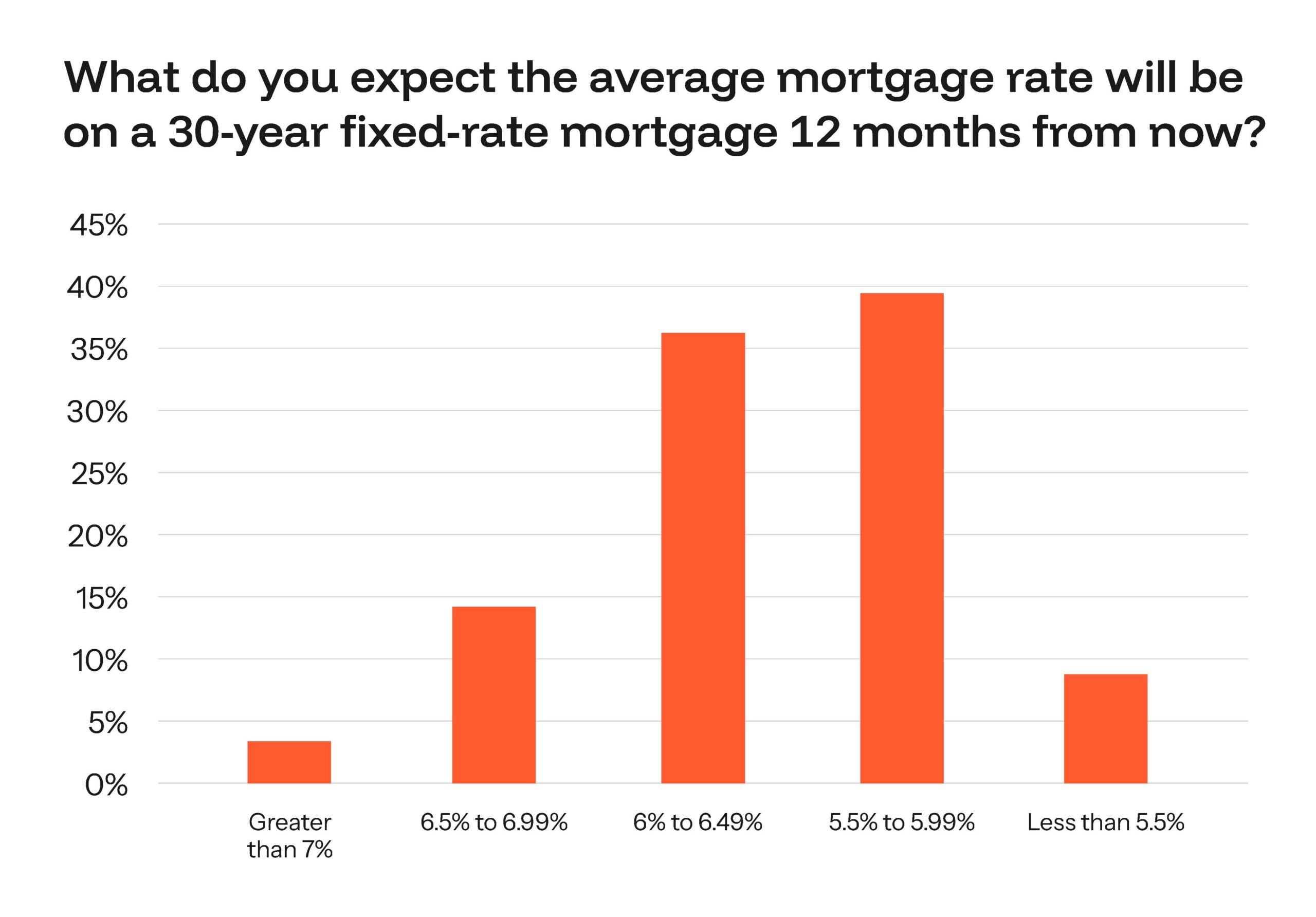

In the brand name brand-new BiggerPockets Pulse survey, BP members were asked to submit their expectations for 2026. In spite of a year of slow frustration in lots of markets, those surveyed feel usually good about doing deals in 2026, with expect lower interest rates and affordability in supporting markets, indicating a gentle changing of the winds in favor of financiers wanting to construct their portfolios.

The Only Way Is Up

Make no error, this is not the crazy bliss of 2020-2022, however more of a “the only method is up” sentiment following current rate drops and news of increased stock in the light of the affordability crisis.

BiggerPockets members’ beliefs align with nationwide projections of a total steadier market. Realtor.com expects interest rates to typical around 6.3% in 2026, down somewhat from 2025, while home cost development is anticipated to be modest. Practically speaking, that could result in increased purchasing opportunities for judicious buyers, but not a remarkable correction.

BiggerPockets members have checked out the market properly, which is why most plan to construct their portfolios rather than sit on the sidelines. The

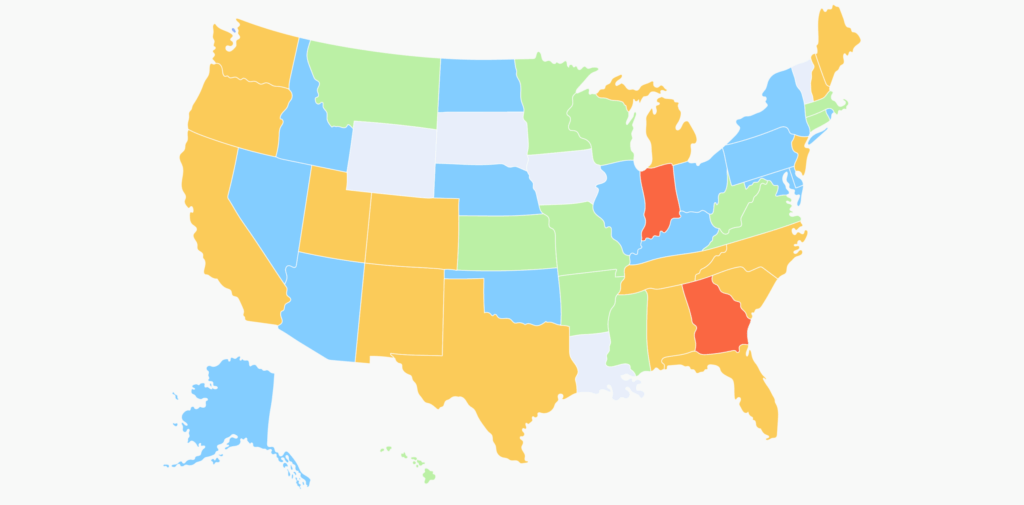

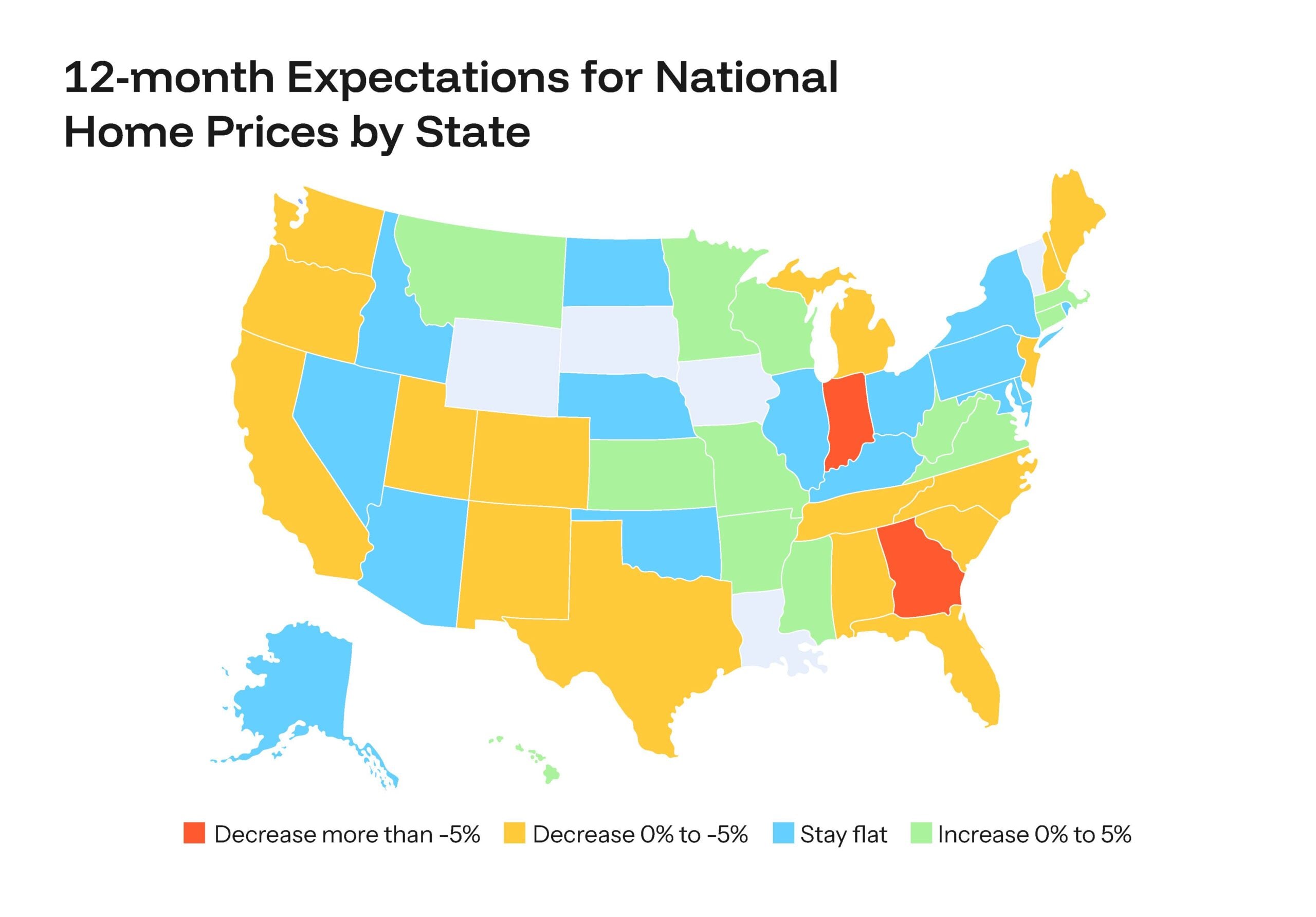

Home Price Growth Map: What’s Up With Atlanta and Indianapolis?

The BiggerPockets home price growth map for 2026 shows an obvious divergence in between markets anticipated to grow and those where momentum has actually stalled or reversed. Georgia and Indianapolis, property stars in previous years, have fallen under the latter category, dropping over 5%. It has had a marked effect on how both residents and buyers feel about their local markets.

“Hotlanta” is no longer hot Atlanta was once a financial investment rock star with an exuberant post-pandemic market. The projection drop in sales is because of softening rents, greater insurance and real estate tax expenses, and a smaller sized pool of buyers able to manage peak-era costs. Financiers in the Atlanta area might do well to await the market to bottom out before making a relocation, and cash flow at current prices might be tough to come by.

Indianapolis: A confounding photo

BiggerPockets information price quotes over a 5% drop in house prices in Indiana. Nevertheless, certain markets will experience higher declines than others. HousingWire reported at the end of 2025 that Indianapolis saw sellers cut costs on 56% of homes amid rising stock and low absorption rates.

Regardless of the relatively worrying numbers for both Atlanta and Indianapolis, the metros are a long way from crash territory. Rather, they are transitioning far from the frenzied cost boosts of 2020 to 2022 towards a more mundane market with slower appreciation.

In both cases, waiting for the marketplace cycle to run its course before leaping in seems sensible for financiers.

Growth Markets: Slow, Steady, and Still Cost effective

If you’re attempting to create an investment method, the Northeast, Midwest, and pockets of the interior South could show a pleased searching ground, according to the BiggerPockets home price?growth map. States expected to appreciate by more than 5% are:

- Arkansas

- Connecticut

- Kansas

- Massachusetts

- Minnesota

- Mississippi

- Missouri

- Montana

- Virginia

- West Virginia

- Wisconsin

Chilly Northeast Markets Present Long-Term Opportunities

Realtor.com shares a similar opinion with New york city markets such as Rochester and Syracuse, which are close to Rhode Island and Connecticut, where Hartford, Connecticut, another fast-appreciating city, lies, where appreciation is expected to be in the double digits. These markets are highlighted by their relatively low housing prices, population development, and restricted housing supply.

A lot of these cities are gaining from huge financial investments from the tech sector. For cautious purchasers, these markets can offer the holy trinity of price, stable growth, and capital– so long as you purchase right.

You may likewise like

Definitely, compared to lots of metros, these cities offer a safer alternative. However, many sections of these cities have not yet “turned the corner,” with high criminal offense still a problem, such as in Syracuse, which suggests buyers need to be careful of entering a tenant landmine.

Why Ownership Rates Affect Rental Inventory

National data shows that since Q2 2025, 65% of U.S. house owners own their homes, while 35% rent, with variations by state. States in the Midwest and South often have higher homeownership rates, and thus tighter sales inventories– factors that support rate stability and moderate gratitude.

Lower rates here equate to higher cost for both house owners and occupants. This contrasts with some of the South and West markets, where rapid building and price escalation have actually resulted in flat or decreasing leas, stagnant or unfavorable price development, and price issues for lots of would-be buyers.

In short, it’s tough to invest in many Sunbelt markets compared to more steady markets in other places, where the numbers still work, demand is diversified, and forecasts indicate slower, long lasting gratitude.

Occupants, Owners, and the Costs

Deciding where to invest needs to be balanced with stats concerning rental demand. Even if a city is budget friendly and appreciating does not suggest there will be a high need for rental real estate.

While the average homeownership numbers around the nation is 65%, in states such as West Virginia, Maine, and Minnesota, ownership spikes to over 70%, according to DoorLoop, while expensive states such as California, New York City, and Nevada see real portions approaching 40%, far above the national average of 35%. In the more pricey states, it’s much more difficult to make cash flow numbers make good sense.

Steady Single-Family Rental Markets

High ownership, lower-cost states and metros such as West Virginia, Delaware, Michigan, Maine, and Vermont tend to support stable single-family rentals since homeowners reward homeownership, according to visualcapitalist.com, however not everyone can buy at first.

These renters have a greater probability of ultimately becoming buyers, but begin by renting a single-family home– the next best thing. As prices rise in single-family markets, the likelihood of renting for longer boosts, but the threats of investing also increase due to greater utilize.

Last Ideas

Putting BiggerPockets Pulse actions together with nationwide forecasts, a coherent investment strategy emerges for 2026. In the face of an amazingly unspectacular housing market, BiggerPockets members are concentrating on long-term leasings and portfolio building, rather than speculative gratitude or short-term leasings.

For depreciating markets such as Atlanta and Indianapolis, adjust underwriting appropriately and purchase right, listed below current comps, preparing for the markets to bottom out or await them to do so. In falling home cost markets, sellers are desperate, creating chances for smart purchasers.

In home-price development markets, investors can not pay for to let the exact same disciplined procedures slip. Recognizing strong, gradually increasing– mid?single digits– instead of exuberantly increasing markets is the crucial to long-term growth. Coupled with this is the requirement for healthy sales activity, price, and income and work ratios listed below 30% for both occupants and house owners.

Layering savvy investment strategies, such as forcing equity through rehabilitation and holding long enough to benefit from progressive gratitude, on top of other metrics, will guarantee the something BiggerPockets investors covet most: a dependable, long-lasting cash-flowing leasing.