- Closed home sales leapt in Might, showing April’s dipping mortgage rates and a strong labor market.

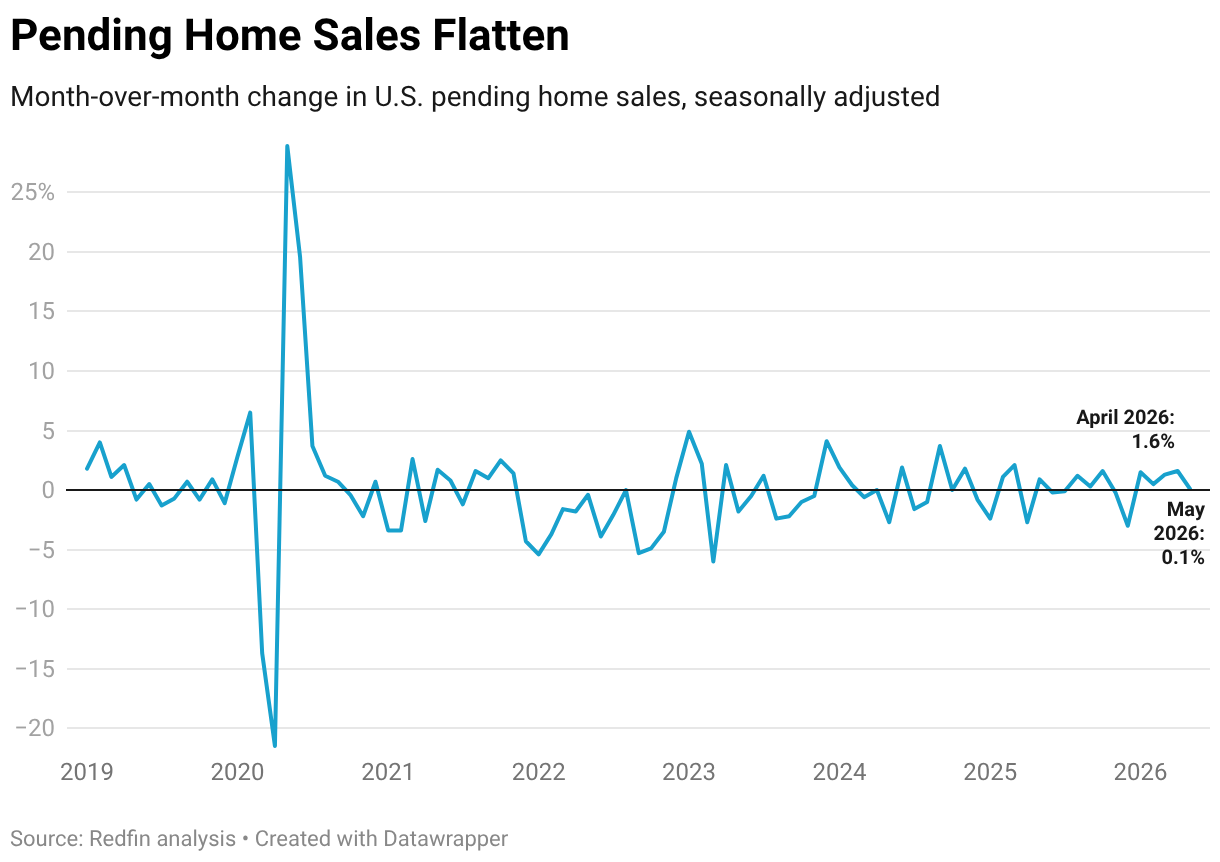

- However pending home sales were flat, a real-time reflection of Might’s increasing mortgage rates and financial uncertainty, which dampened buyers’ appetites.

- The Bay Location’s AI-fueled hot housing market added to the surge in closed sales, with double-digit sales upticks in San Jose and San Francisco. So did a rise in West Palm Beach, a market that’s typically driven by upscale purchasers.

- New listings rose to their highest level since 2022 as sellers tried to catch demand.

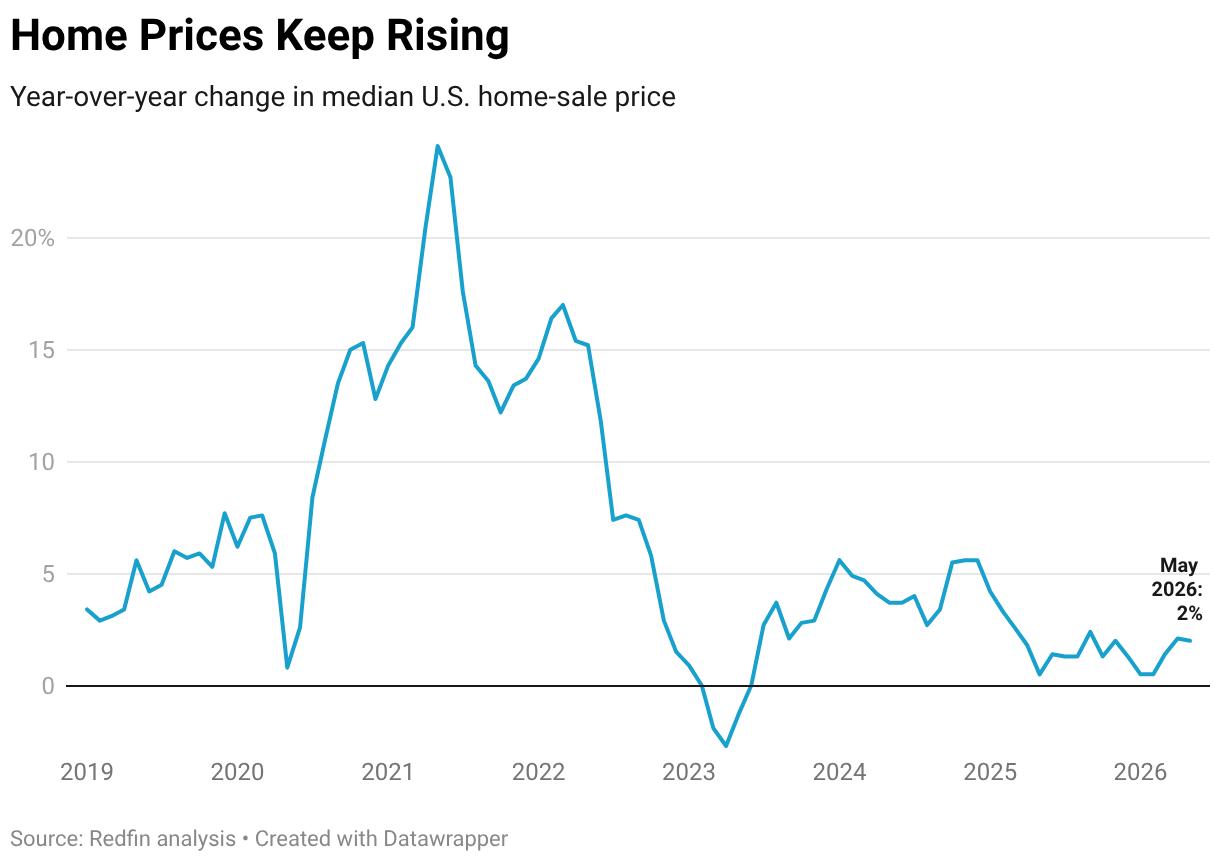

- Home rates increased 2% year over year.

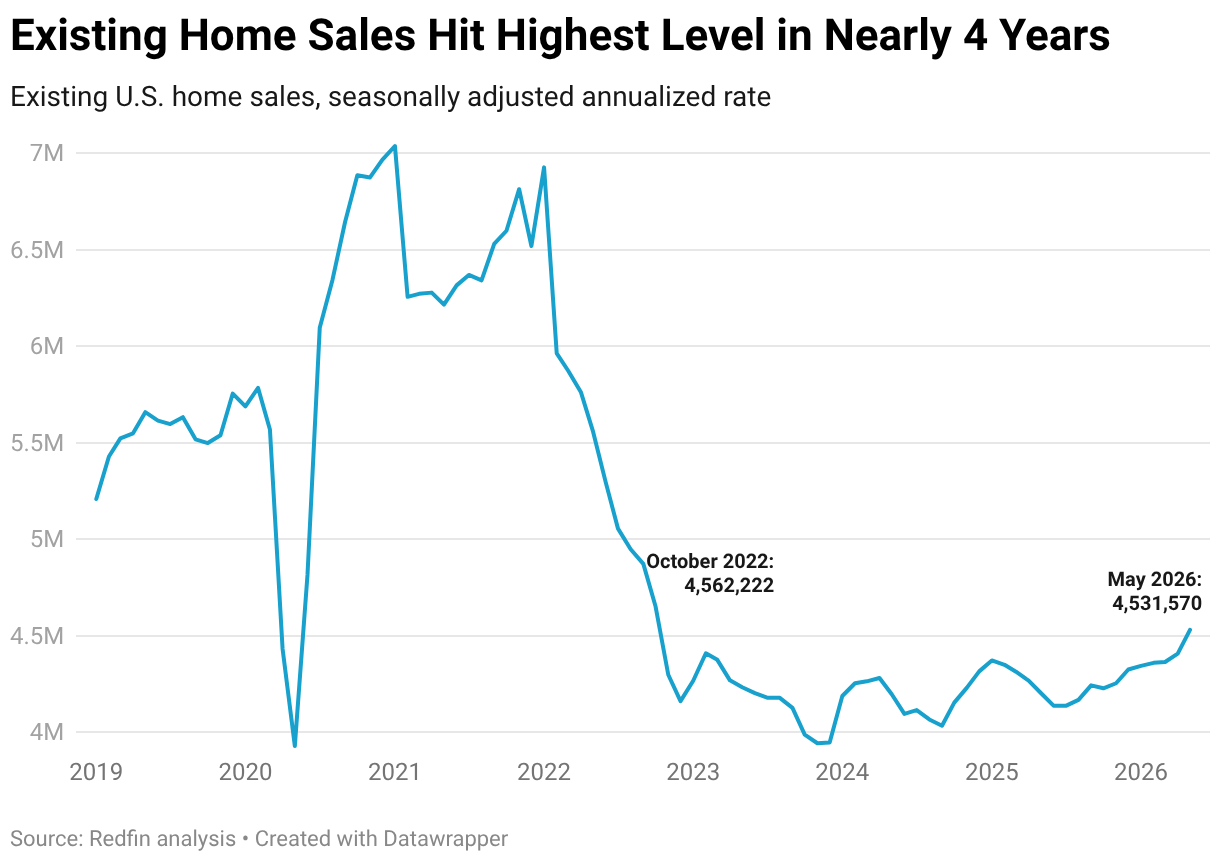

U.S. existing-home sales leapt 2.8% month over month in Might to their greatest level because October 2022. Overall home sales– including both existing and freshly developed homes– likewise increased to their greatest level given that October 2022, rising 3.8% month over month. While closed sales rose, pending sales– a more present market indicator– flattened as home loan rates increased.

All figures in this report are seasonally changed, with the exception of average list price information and home loan rate information. See a more comprehensive methodology here and view an interactive control panel here.

There are several reasons home sales struck their highest level in almost four years in May:

-

- Home loan rates dipped. They dropped down to the 6.3% variety for much of April after spiking in March. Sales that closed in May were made up of homebuying contracts that were signed– and rates that were secured– throughout April.

- It’s a purchaser’s market. There were numerous thousands more home sellers than purchasers out there, enabling purchasers to work out cost reductions and seller concessions, helping offers cross the finish line regardless of high costs. Furthermore, the labor market enhanced, making numerous Americans feel more confident about making a huge purchase.

- The Bay Area’s hot market added to the across the country uptick in sales. In San Jose, home sales soared 26% year over year in Might, and in San Francisco they leapt 19%. The AI boom is driving strong homebuying need in the Bay Area as workers of AI companies gather big wages and bonus offers.

- South Florida contributed, too. Closed home sales rose 18% year over year in West Palm Beach, FL, a market that’s generally driven by luxury purchasers who are less concerned about high expenses and economic jitters.

Pending Home Sales Flatten, Reflecting Real-Time Rising Rates

While closed home sales leapt in May, pending home sales were essentially flat (0.1%) month over month. Sales that closed in May are a backwards-looking indicator, showing the period when home mortgage rates fell temporarily in April.

Pending home sales are more reflective of the existing state of the market, representing homes that went under contract in Might– when home loan rates skyrocketed to an 11-month high. Economic and international uncertainty likewise frightened prospective purchasers: The continuous Iran war and closure of the Strait of Hormuz, AI-driven inflation and the possibility of interest-rate walkings all came together to paint a muddy financial picture.

New Listings Rise, Pressing Overall Stock to 6-Year High New listings of U.S. homes for sale increased 1.4 %month over month to their greatest level considering that 2022. The overall variety of homes for sale ticked up 0.4%from a month

previously, to their greatest level given that 2020. New listings increased partially since sellers noticed improving homebuying need in April, and intended to take advantage of it. Overall stock is at a six-year high since in addition to new sellers, there are a great deal of stagnant listings resting on the market after a slow start to the year.

Keep in mind that high inventory is another factor home sales struck their greatest level in nearly 4 years in Might. When there are more homes on the marketplace, there are more alternatives for homebuying deals.

Home Rates Continue Climbing Up

The average U.S. home list price increased 2% year over year in Might to $398,771. Prices kept increasing since there were more property buyers closing offers.

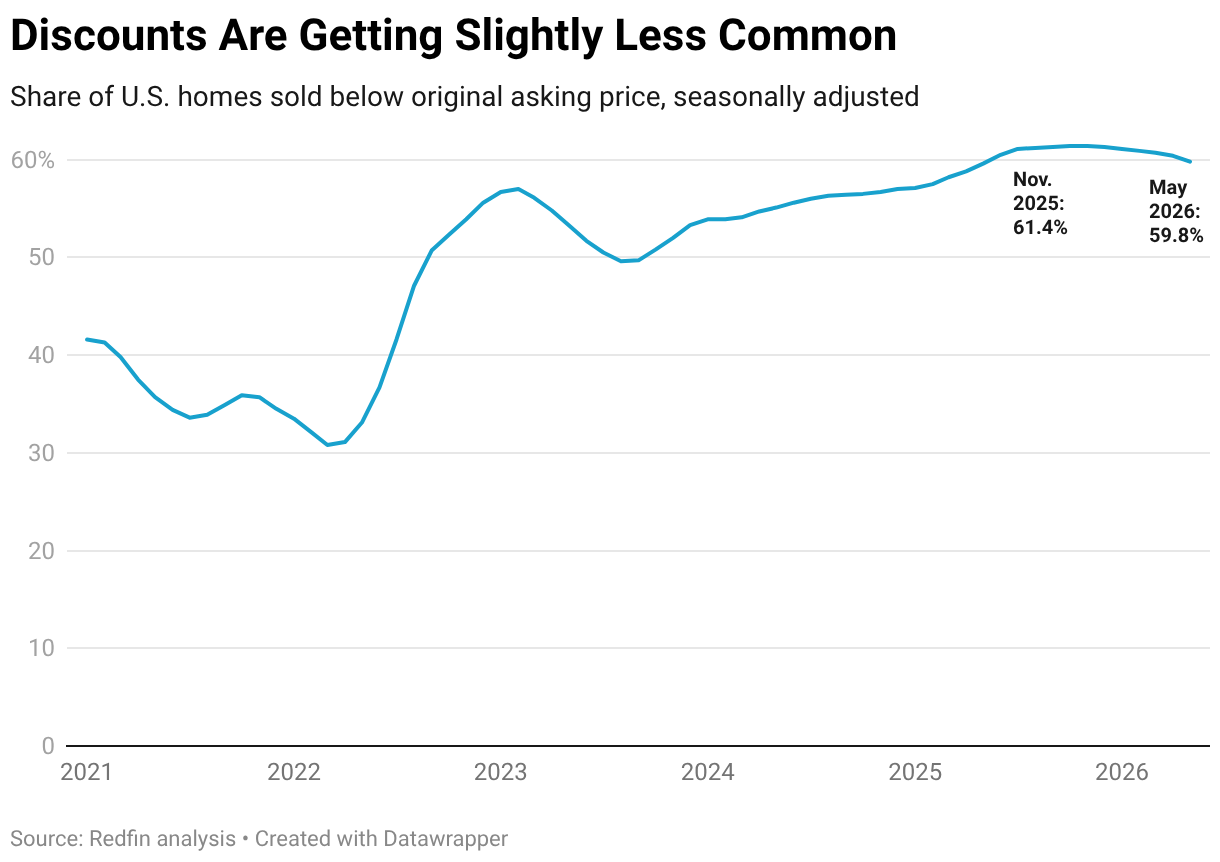

Less Buyers Are Getting Discounts Just under 3 in 5(59.8%)homes that offered in May opted for less than their initial sale price. That’s a somewhat smaller share than the month before, and marks the sixth straight month in which this share has decreased. That means that while a lot of homebuyers are still scoring discount rates, it is ending up being a little less typical.

Discount rates are ending up being a bit less typical since while it’s still a big-time buyer’s market, the benefit purchasers have more than sellers has actually begun shrinking. Another reason is that sellers are pricing their homes more realistically from the start. The median rate for new listings in May was essentially flat (-0.1%) month over month, compared to the 2% boost in sale rates.

|

May 2026 Housing Market Highlights: United States |

|||

|---|---|---|---|

|

May 2026 |

Month-over-month change |

Year-over-year change |

|

|

Median list price |

$398,771 | n/a | 2% |

| Existing-home sales, seasonally changed annual rate | 4,531,570 | 2.8% |

7.8% |

| Pending home sales | 350,173 | 0.1% |

4.5% |

| Houses sold | 308,446 | 3.8% |

5.2% |

|

New listings |

396,181 | 1.4% | 1.2% |

| Overall homes for sale (active listings) | 1,483,839 | 0.4% |

0.7% |

| Months of supply | 3.7 |

-0.1 |

-0.2 |

|

Average days on market |

49 |

the same |

3 |

| Share of homes that offered listed below initial list price | 59.8% |

-0.6 ppts |

0.2 ppts |

| Typical sale-to-original-list-price ratio | 96.3% | 0.1 ppts |

unchanged |

| Pending sales that fell out of agreement, as % of total pending sales | 13.6% | 0.1 ppts | 0.1 ppts |

| Regular monthly average 30-year set home mortgage rate | 6.44% | 0.11 ppts | -0.38 ppts |

May 2026 Metro-Level Emphasizes

The figures listed below are based upon a list of the 50 most populated U.S. metropolitan areas. Some metros may be gotten rid of from time to time to make sure data accuracy. Describe our metrics meaning page for explanations of metrics utilized in this report. All modifications listed below represent year-over-year changes.

- Rates: Average sale prices rose most from a year earlier in San Francisco (10.9%), St. Louis (6.7%) and Pittsburgh (6.7%). They fell most in San Jose, CA (-5.6%), Orlando, FL (-2.2%), Seattle (-0.9%) and San Antonio (-0.9%).

- Pending home sales: Pending sales increased most in West Palm Beach, FL (34.5%), San Francisco (21.4%) and Miami (16.2%). They fell most in Houston (-12.5%), Seattle (-7%) and Tampa, FL (-3.4%).

- Closed home sales: Home sales rose most in San Jose (25.7%), San Francisco (19.3%) and West Palm Beach (18.3%). They fell most in Detroit (-14%), New York City (-9.1%) and Providence, RI (-8.4%).

- New listings: New listings increased most in Philadelphia (11.5%), Minneapolis (9.5%) and Boston (8.6%). They fell most in St. Louis (-17.9%), Denver (-10%) and San Antonio (-9.2%).

- Active listings: Active listings rose most in Cincinnati (15.1%), Boston (15%) and Montgomery County, PA (12.6%). They fell most in Jacksonville, FL (-17.4%), Miami (-13.9%) and Tampa, FL (-12.8%).

- Days on market: In Jacksonville, FL the normal home that went under agreement did so in 69 days, which was 6 days quicker than a year earlier– the most significant decline amongst the metros analyzed. Next came Orlando, FL (-6 days) and West Palm Beach, FL (-4 days). Days on market increased the most in San Antonio (+14 days), Houston (+11 days) and Nashville, TN (+8 days).

| May 2026 Complete Metro-Level Data | ||||||||

| U.S. city location | Typical list price | Mean list price, Y/Y change | Pending sales, Y/Y change | Homes sold, Y/Y modification | New listings, Y/Y modification | Active listings, Y/Y modification | Mean days on market | Typical days on market, Y/Y modification |

| Anaheim, CA | $1,255,878 | 4.7% | 5.6% | 7.7% | -4.1% | -7.2% | ||

| Atlanta, GA | $403,755 | 0.9% | -2.1% | 3.0% | -5.8% | -2.3% | 59 | 4 |

| Austin, TX | $443,632 | -0.3% | 9.5% | 8.7% | 3.1% | -3.3% | 87 | 6 |

| Baltimore, MD | $431,669 | 5.3% | 2.9% | -0.6% | 4.9% | 9.9% | 39 | 7 |

| Boston, MA | $777,603 | 0.3% | 9.1% | 0.0% | 8.6% | 15.0% | 25 | 2 |

| Charlotte, NC | $419,198 | 0.2% | 2.6% | 7.3% | 0.9% | 8.0% | 64 | 4 |

| Chicago, IL | $395,780 | 5.3% | 5.8% | 4.5% | 3.0% | 0.3% | 51 | -2 |

| Cincinnati, OH | $324,001 | 4.5% | 7.1% | 5.1% | 15.1% | 43 | 1 | |

| Cleveland, OH | $250,229 | 4.3% | 5.4% | 8.2% | 0.4% | 5.1% | 29 | 0 |

| Columbus, OH | $363,878 | 3.4% | 7.0% | 13.8% | 7.5% | 9.1% | 48 | 4 |

| Dallas, TX | $423,694 | 2.1% | 3.0% | 1.0% | -5.2% | -5.1% | 59 | 1 |

| Denver, CO | $608,125 | 1.4% | -2.3% | 6.1% | -10.0% | -6.5% | 34 | 3 |

| Detroit, MI | $224,308 | 4.3% | -0.8% | -14.0% | 1.2% | 10.9% | 29 | 3 |

| Fort Worth, TX | $362,881 | 0.0% | 6.4% | 5.2% | -7.7% | -6.9% | 59 | 1 |

| Houston, TX | $341,996 | 1.5% | -12.5% | -1.7% | -2.1% | -0.6% | 66 | 11 |

| Indianapolis, IN | $324,001 | 2.5% | 4.0% | 14.0% | -1.5% | 6.5% | 32 | 5 |

| Jacksonville, FL | $388,801 | 6.2% | 2.9% | 1.7% | -3.0% | -17.4% | 69 | -6 |

| Kansas City, MO | $363,878 | 4.0% | 0.7% | 2.0% | -6.4% | -3.7% | 24 | 2 |

| Las Vegas, NV | $453,602 | 1.0% | 4.6% | 6.1% | -6.3% | 0.1% | 64 | 8 |

| Los Angeles, CA | $937,111 | 0.8% | 2.6% | 10.9% | -5.7% | -4.3% | 49 | 1 |

| Miami, FL | $568,248 | 0.0% | 16.2% | 4.9% | -7.4% | -13.9% | 88 | 2 |

| Milwaukee, WI | $363,878 | 4.0% | 12.4% | 9.8% | 3.4% | 10.4% | 44 | 1 |

| Minneapolis, MN | $398,671 | -0.2% | 13.7% | 6.1% | 9.5% | 10.3% | 32 | 2 |

| Montgomery County, PA | $517,405 | 1.6% | 11.3% | -0.4% | 6.1% | 12.6% | 33 | 6 |

| Nashville, TN | $484,252 | 0.9% | 5.2% | 10.4% | 0.6% | 10.6% | 75 | 8 |

| Nassau County, NY | $749,689 | 5.4% | 9.8% | -2.7% | -7.4% | 1.8% | 33 | 1 |

| New Brunswick, NJ | $583,202 | 0.6% | 5.4% | -3.8% | 6.8% | 9.9% | 40 | 2 |

| New York, NY | $812,495 | 2.2% | 8.6% | -9.1% | -2.8% | 0.4% | 56 | 2 |

| Newark, NJ | $662,956 | 6.2% | 3.8% | 0.5% | 6.6% | 7.1% | 27 | -4 |

| Oakland, CA | $996,927 | 1.7% | 1.0% | 13.2% | -5.9% | -9.6% | 22 | -2 |

| Orlando, FL | $410,734 | -2.2% | 4.1% | 2.7% | 1.7% | -7.1% | 48 | -6 |

| Philadelphia, PA | $314,032 | 1.3% | 2.1% | -1.5% | 11.5% | 7.3% | 47 | 4 |

| Phoenix, AZ | $467,559 | -0.1% | 7.1% | 11.3% | -3.3% | -3.6% | 66 | 4 |

| Pittsburgh, PA | $272,161 | 6.7% | 5.6% | 1.1% | 3.7% | 7.8% | 60 | 0 |

| Portland, OR | $568,248 | -0.3% | 8.0% | 7.7% | -4.7% | -0.7% | 33 | 0 |

| Providence, RI | $521,393 | 2.2% | 8.3% | -8.4% | 2.4% | 5.2% | 29 | 2 |

| Riverside, CA | $590,928 | 0.3% | 2.4% | 2.1% | -7.9% | -11.4% | 55 | 1 |

| Sacramento, CA | $603,141 | 1.4% | 6.9% | 11.7% | -7.5% | -4.2% | 34 | 0 |

| San Antonio, TX | $309,047 | -0.9% | 8.2% | -5.9% | -9.2% | 0.9% | 86 | 14 |

| San Diego, CA | $922,157 | 0.4% | 8.8% | 7.2% | 1.1% | -4.9% | 34 | 1 |

| San Francisco, CA | $1,774,529 | 10.9% | 21.4% | 19.3% | 0.7% | -12.3% | 19 | -2 |

| San Jose, CA | $1,605,052 | -5.6% | 0.0% | 25.7% | 7.0% | 10.1% | 19 | 1 |

| Seattle, WA | $842,403 | -0.9% | -7.0% | 1.8% | -4.7% | 12.2% | 21 | 7 |

| St. Louis, MO | $304,063 | 6.7% | 7.6% | -3.0% | -17.9% | 1.4% | 27 | -1 |

| Tampa, FL | $385,561 | 1.7% | -3.4% | 3.2% | -5.5% | -12.8% | 49 | 5 |

| Virginia Beach, VA | $382,441 | 2.9% | 7.2% | 6.4% | 2.3% | 0.9% | 36 | 3 |

| Warren, MI | $338,955 | 2.7% | 8.4% | 3.9% | 8.2% | 11.7% | 26 | 2 |

| Washington, DC | $626,568 | 3.0% | 5.4% | 10.3% | 3.5% | 8.7% | 45 | 3 |

| West Palm Beach, FL | $538,340 | 1.6% | 34.5% | 18.3% | 5.2% | -5.1% | 82 | -4 |