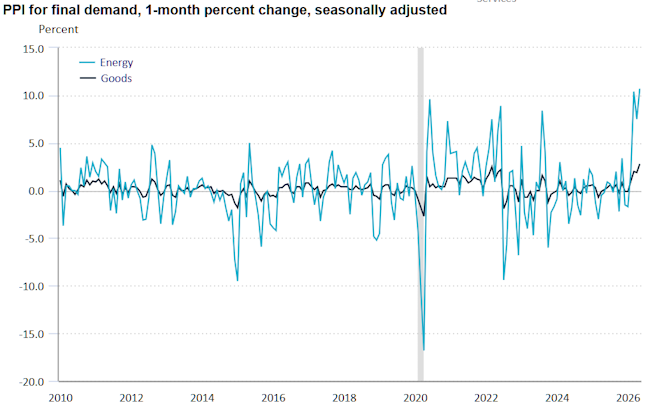

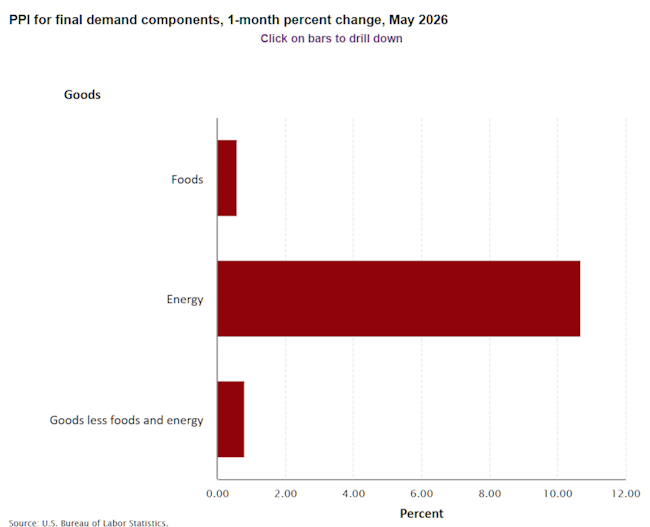

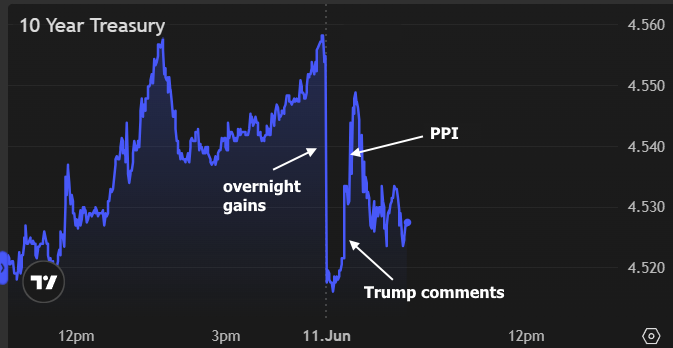

Bonds were fairly more powerful in the overnight session with 10yr yields down roughly 4bps from 4.56 to 4.52. About 8 minutes before the PPI information came out, a series of Trump discuss the Iran war sent oil prices and bond yields higher (new strikes and intent to take Kharg Island). PPI contributed to the pressure with the monthly heading striking 1.1% vs 0.7% forecast. The reality that core PPI can be found in at 0.4% vs 0.7% last month informs us that energy rates are the main driver (as does the text of the report itself, oddly enough). In fact, both energy and goods inflation are running greater than post-pandemic.

However the market assumes these can still be relatively short-term spikes if the war ends. Factor being, despite the fact that goods inflation is the greatest in years (month over month), that consists of energy-related products.

Bonds had already gone through this mental mathematics and discovered their footing about 6 minutes after the data. A couple of minutes later, Trump made additional remarks that helped press back in the other direction. With that, bonds have restored the majority of the ground lost previously today.

< img src="http://a.mbslive.net/assets/6a2abab4426428184492a0ac/6a2abab4426428184492a0ac.png" alt="20260611 open3.png"/ >