-

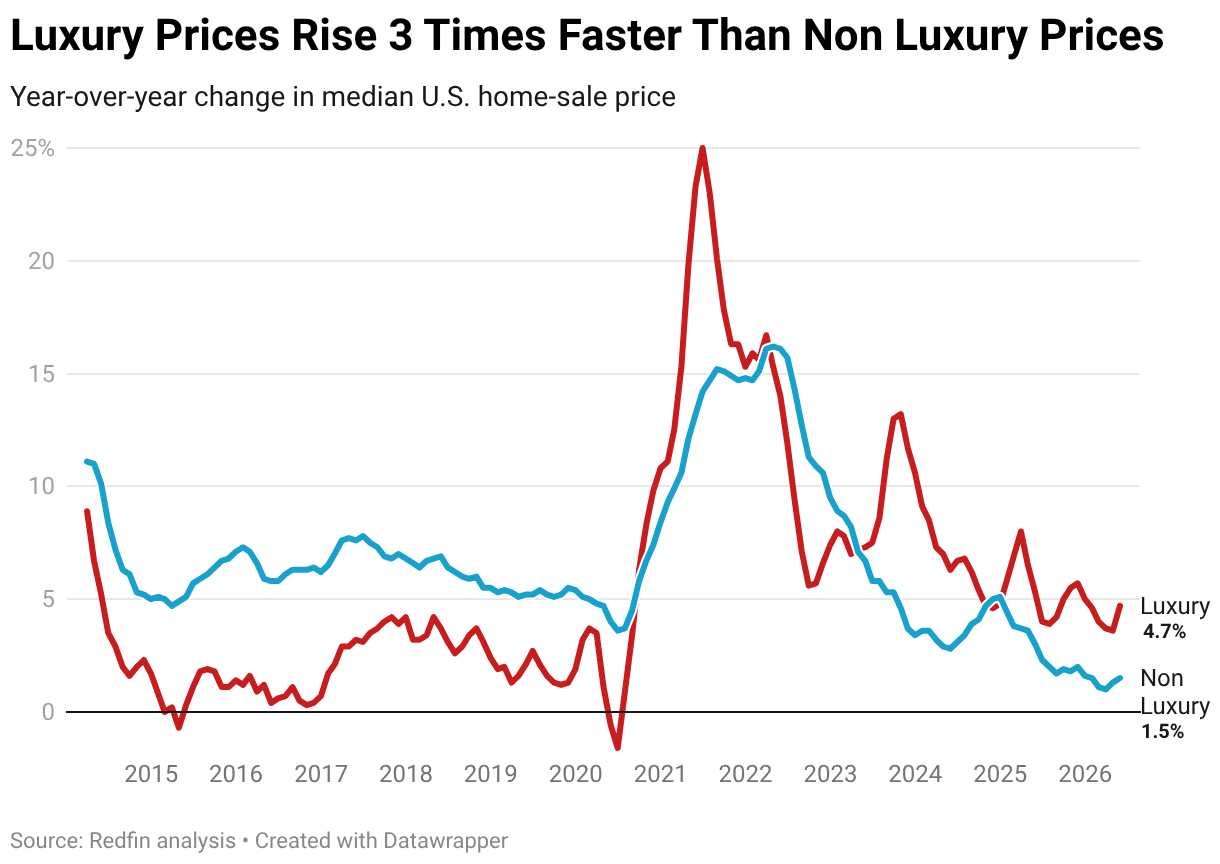

- High-end U.S. home prices are up 4.7 %year over year, compared to a 1.5 %boost in non high-end costs, as homebuying need from wealthy individuals continues to surpass need from average Americans.

- High-end purchasers are more active partly since they’re less sensitive to high mortgage rates and today’s financial uncertainty.

- Luxury rates are rising fastest in Tampa and Miami, partly due to an influx of ultra-wealthy people moving into Florida.

- Luxury sales are increasing fastest in San Francisco, mainly due to the AI boom, followed by Nashville, San Diego and a number of Florida city.

The median U.S. luxury home price increased 4.7% year over year to $1.37 million during the 3 months ending May 31– more than triple the 1.5% gain in non high-end sale prices.

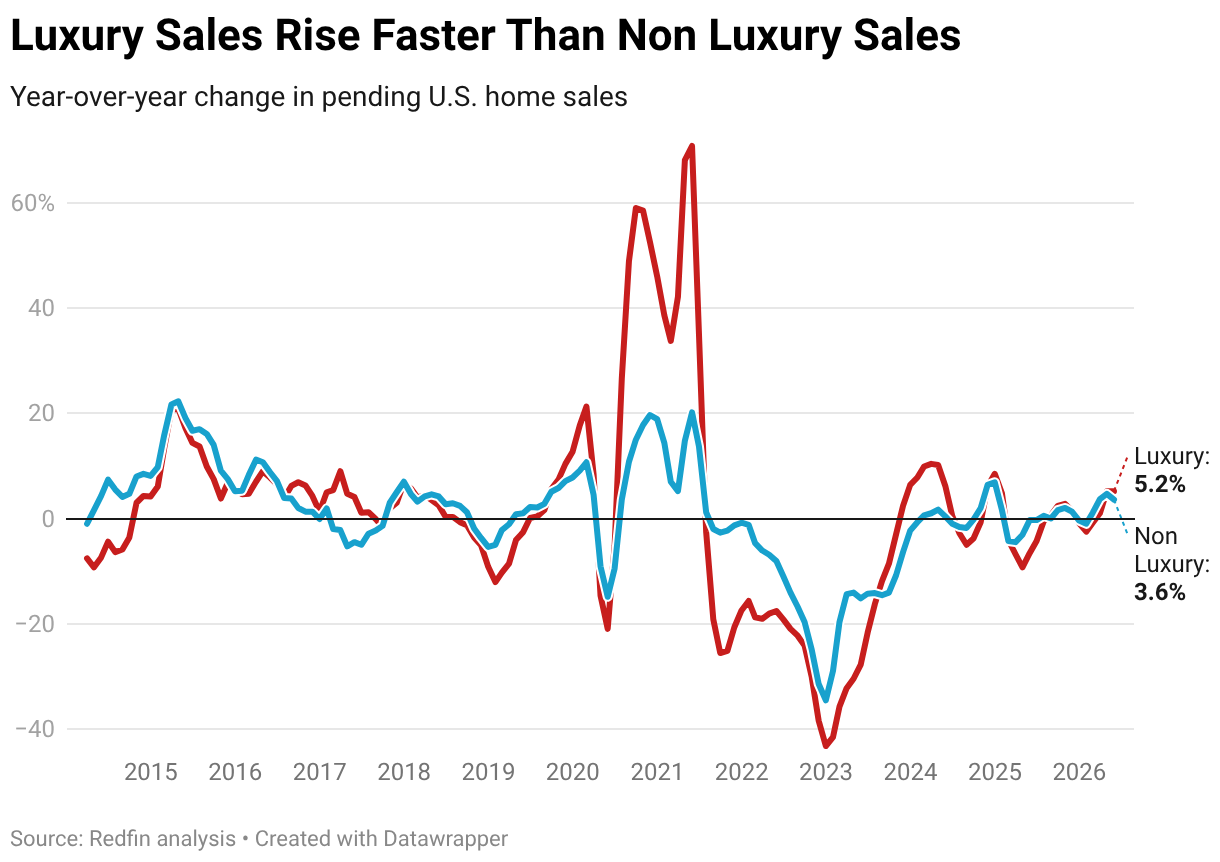

Luxury rates are increasing mainly due to the fact that demand for high-end homes is on the rise. Pending sales of luxury homes increased 5.2 %year over year– the biggest gain because December 2024. That’s compared to a 3.6% gain in non high-end pending sales, which is a deceleration from the month before.

This report is based on a Redfin analysis of MLS data that goes through revision. All figures cover rolling three-month durations. Redfin defines luxury homes as those approximated to be in the top 5% of their metro location’s price range, while non-luxury homes fall under the 35th– 65th percentile.

High-end property buyers are more active because they’re less sensitive to the cost pressures and monetary instability dealing with many Americans today. Overall homebuying demand has been relatively sluggish due to the fact that home mortgage rates and home rates remain stubbornly high, pricing numerous regular house hunters out of the marketplace. In addition, the economic unpredictability stemming from the back-and-forth on the Iran war, inflation, and the possibility of the Fed treking rates of interest is making some prospective purchasers think twice about making a huge purchase. Ultra-wealthy Americans, by contrast, have more money to pay high housing expenses, and they have the freedom to make huge purchases even in unsure times.

“The luxury market has been unsusceptible to the real estate downturn, particularly in the most preferable, beachfront areas,” said Mike DeMello, a Redfin Premier agent in Honolulu. “Affluent buyers who can manage luxurious homes are often insulated from things like high mortgage rates and financial uncertainty. On the other hand, a great deal of residents are choosing to rent since costs and rates are merely too expensive to buy.”

Tampa and Miami Lead Country in High-end Home-Price Growth

High-end home prices in Tampa, FL rose 15.6% year over year, the most significant boost of the 50 most populated U.S. metros, followed closely by Miami (14.2%). By contrast, non luxury rates fell 0.5% in Tampa, and they fell 0.7% in Miami.

Luxury prices are increasing in seaside Florida while non high-end prices are ticking down since upscale buyers are purchasing up homes in the Sunlight State. 3 of the 10 U.S. metros with the most significant increases in high-end pending sales remained in Florida: Tampa can be found in fourth, with a 20.8% boost in pending sales, West Palm Beach is fifth (18.5% boost), and Miami is seventh (14.6%).

Billionaires, tech business owners, executives and other wealthy Americans are drawn to Florida for its favorable tax environment, warm environment and waterfront way of life, driving strong need for high-end homes even as the wider real estate market softens in some parts of the state. Places like Miami and West Palm Beach have actually become magnets for ultra-rich Americans; for instance; Mark Zuckerberg recently paid $170 billion for an estate on an island called “Billionaire Bunker.” Florida normally controls Redfin’s list of the majority of pricey U.S. home sales every month; those ultra-expensive sales push up median luxury costs.

Luxury Pending Sales Increasing Fastest in San Francisco, Nashville and San Diego– Outpacing Florida Metros

San Francisco, Nashville, TN and San Diego are the only city where pending high-end sales are increasing faster than they are in Florida. Pending sales of San Francisco high-end homes increased 45.9% year over year, without a doubt the biggest increase of the metros in this analysis, followed by Nashville’s 24.5% boost and San Diego’s 22.5% increase.

The Bay Location’s luxury market is soaring mostly since of the AI boom, with lots of tech employees putting their wages and rewards into real estate. Nashville, as kept in mind above, is bring in a lot of rich citizens who move there for jobs and Tennessee’s favorable tax environment. San Diego is capturing some spillover from Los Angeles, with some upscale house hunters picking coastal San Diego instead of locations like Beverly Hills for personal privacy, a slower pace of life and oceanfront access.

Luxury Homeowners Are Listing at a Slightly Higher Rate Than Everybody Else

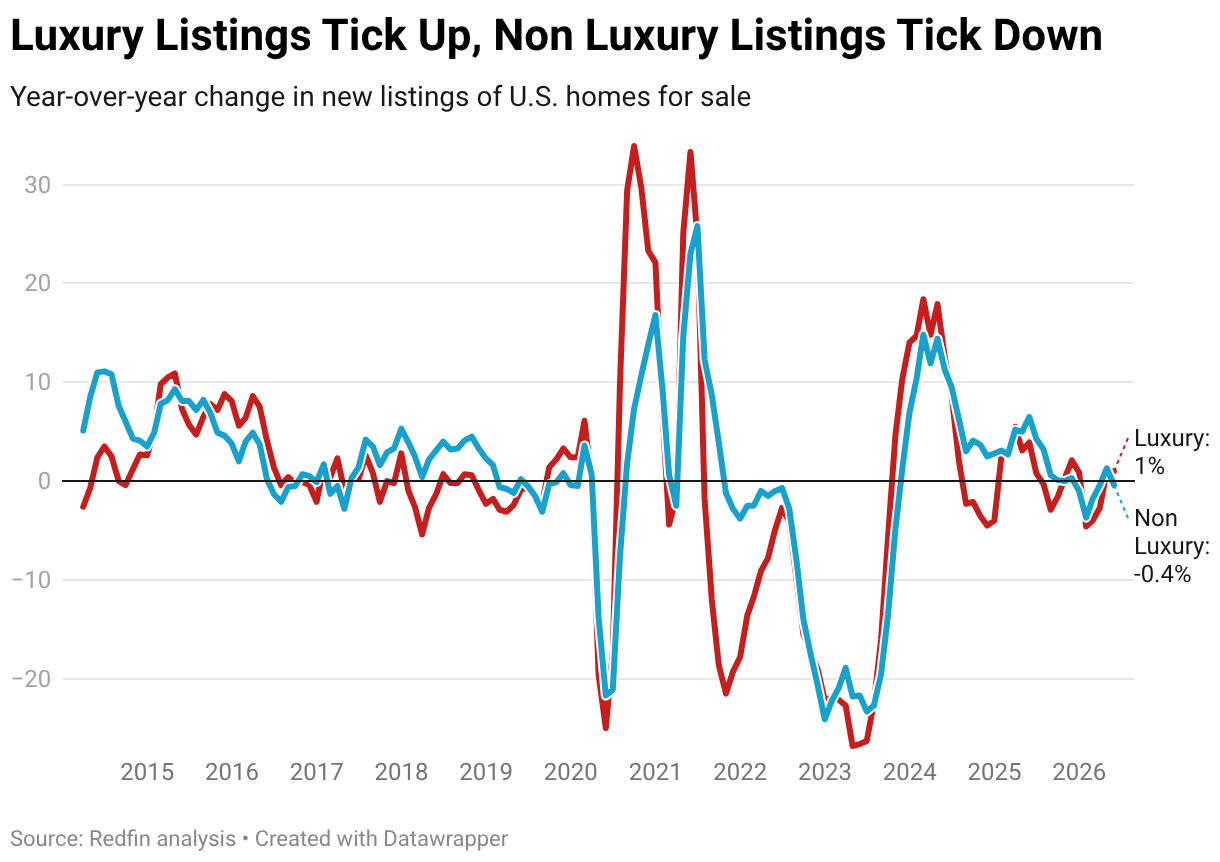

On the selling side, new listings of U.S. luxury homes increased 1% year over year throughout the 3 months ending Might 31. That’s compared to a 0.4% decline in non luxury new listings.

Owners of high-end homes are somewhat more going to list than owners of regular homes, likely due to the fact that high rates and strong need have made this a favorable moment to squander. But wealthy property owners don’t have a lot of incentive to sell: A lot of them are locked into low home mortgage rates, there are tax deterrents to offering pricey houses, and lots of rich Americans don’t need to sell their home when they move; they may have the ability to move into a different home and hang onto their old one.

Luxury Market Summary: 3 Months Ending May 2026 High-end

| Non High-end Average | list price$ | |||

|---|---|---|---|---|

| 1,374,470$377,477 | Average sale | cost, YoY modification 4.7% | ||

| 1.5%Pending home sales, YoY change 5.2% | 3.6% | |||

| Residences sold, YoY modification | 2% | 2% | ||

| New listings, YoY modification | 1% | -0.4%Active listings | , YoY change | 0.4% |

| 1.2%Median days on market 49 44 | Average days | on market, | ||

YoY modification 5 3 Metro-Level High-end Emphasizes: 3 Months Ending May

| 2026 Redfin’s metro-level luxury data |

is based |

on an analysis |

|

of the 50 most populous U.S. metropolitan areas; the 49 with adequate

information are

included in this report. All changes below are year over year. Costs: High-end costs increased most in Tampa, FL(15.6% ), Miami (14.2% )and Las Vegas(13.7%). They fell in just 4 metros: New Brunswick, NJ( -4.3 %), Oakland, CA(

- -1.8%),Detroit(-1 %)and Dallas (-0.3 %). Pending sales: Luxury pending sales rose most in San Francisco(45.9 %), Nashville, TN (24.5%)and San Diego(22.5 %). They

- fell most in Seattle( -14.8% ), Nassau County, NY( -14.3 %) and Baltimore (-10.4%). Closed home sales: High-end home sales rose most in San Francisco (46.3 %), Tampa (27.4%)and Portland, OR (13.1%). They fell most in Anaheim

- (-16.9 %), Orlando( -13.2% )and Seattle(-13 %). New listings: High-end brand-new listings increased most in Warren, MI (28.2%), Columbus, OH (12.4%)and Nashville, TN (11.4%)

- . They fell most in Las Vegas (-16.5% ), Anaheim, CA (-15.7% )and Denver (-15.7%). Active listings: Luxury active listings increased most in Warren, MI (20.5%),

- Seattle (13.9%)and Detroit(12.8%). They fell most in Anaheim (-23.2%), New York City (-18.6% )and Miami (-17.2%). Typical days on market: In Pittsburgh, the normal luxury home that went under agreement did so in 54 days, down 9 days from a year earlier– the greatest decrease amongst the metros Redfin examined. Next came St. Louis (-7) and Austin, TX (-6). The greatest increases remained in Miami(+24 days), Las Vegas(+23 )and Nassau County, NY (+19). Complete Metro-Level Luxury Data: 3 Months Ending May 2026 Redfin evaluated the 50 most populated U.S. city areas and consisted of the 49 with

| sufficient information. Fort Lauderdale , FL is excluded. U.S. city area

Median sale price Average list price, YoY modification Pending sales, YoY modification Homes sold, YoY change New listings, YoY change Active |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| listings, YoY change Typical days on market Mean days on market, YoY modification Anaheim, | CA$5,276,971 2.2 %-1.1%-16.9%-15.7%-23.2%47 1 Atlanta, GA$ 1,440,533 6.4%2.4 | %-4.3%6.6%12.2 %32 -1 Austin, TX$1,811,150 9.0%9.3% 5.5%-13.4 %-10.1%51 -6 Baltimore | , MD$1,276,125 4.0%-10.4%-12.6%-2.3%-5.7%31 9 Boston, MA$ 2,826,655 7.4%-8.6%-6.0

| %-4.3%-4.1% |

28 1 |

Charlotte |

, NC$1,660,462 4.7% |

-1.1% |

-7.6% |

3.8%8.7 |

% |

43 7 Chicago, IL$1,545,360 |

6.2% |

11.3 |

% |

5.1% |

0.6% |

-12.2%44 |

-5 |

Cincinnati |

, OH$952,523 0.3 |

% |

4.3% |

-2.6 |

% |

5.7% |

2.5%44 1 |

Cleveland, OH$

| 833,228 11.0 %9.4%3.0 |

%3.1%-2.2% |

24 -2 Columbus |

, OH$1,017,342 2.9% |

13.0% |

5.9%12.4 |

% |

6.8%37 -1 Dallas, TX$1,603,312 |

-0.3 |

% |

7.1% |

1.7% |

2.4% |

6.2%38 4 |

Denver |

, CO |

$1,971,456 |

4.3% |

-5.1% |

0.0% |

-15.7% |

-4.9%20 |

7 |

Detroit, MI |

$719,252 -1.0% |

-6.9% |

6.5% |

-2.1 |

% |

12.8%15 |

5 |

Fort Worth, TX |

$1,309,293 9.4 |

% |

2.1% |

12.2% |

-9.8 |

% |

-8.8%34 |

3 |

Houston, TX |

$1,361,843 4.9 |

% |

-4.5 |

% |

-5.8 |

% |

-7.5%-2.2%28 9 Indianapolis

| , IN |

$1,009,314 |

9.0% |

-4.1% |

2.7% |

-4.6% |

-6.8 |

%18 4 Jacksonville, FL |

$1,589,567 |

6.9%4.5%-2.6% |

-5.0 |

% |

-11.5% |

54 |

-1 Kansas City

| , MO |

$1,137,946 |

10.9 |

% |

-6.4 |

% |

4.8% |

-1.6%-6.2%30 -5 Las Vegas, NV

| $1,694,567 13.7%-1.0%-11.6%-16.5% |

-4.5% |

79 23 |

Los Angeles |

, CA$4,512,482 4.9% |

0.4%0.0 |

%-7.2 %-10.8 %49 4 Miami, FL$4,855,331 |

14.2 |

% |

14.6% |

5.2% |

-13.0 |

%-17.2% |

150 24 Milwaukee, WI |

$1,098,057 |

8.9% |

9.8% |

0.0% |

0.3% |

-6.5% |

51 |

0 |

Minneapolis, MN |

$1,284,400 |

8.1% |

-5.2% |

-12.6% |

5.4% |

4.8%31 3 |

Montgomery County, |

PA$1,544,219 8.5% |

0.0%-2.4% |

7.3% |

10.7% |

32 7 Nashville, TN$2,190,591 7.1%24.5 |

%10.0%11.4%8.4

| %96 11 Nassau County, NY$2,862,605 |

13.3% |

-14.3 |

% |

-7.0% |

-7.0% |

-8.3%100 |

19 |

New Brunswick |

, NJ$1,947,027 |

-4.3% |

6.5% |

-5.3% |

9.6% |

4.6% |

34 |

1 New York |

, NY |

$4,380,249 |

5.0% |

-2.5 |

% |

-9.5% |

-12.3% |

-18.6%83 |

16 Newark, NJ$

| 2,126,234 |

7.9%-3.1%-8.6% |

5.2% |

-7.6% |

15 -3 Oakland |

, CA |

$2,999,012 -1.8

| %1.1%1.9%-6.9 |

%-14.9%12 0 |

Orlando, FL |

$1,437,130 |

4.5% |

-6.7 |

% |

-13.2%-6.8%-9.9%41 |

11 Philadelphia, PA$1,342,284 |

11.1 |

% |

-0.3% |

-1.8 |

% |

-6.0%-3.6%43 13 Phoenix, AZ

| $2,225,630 12.6%14.2% |

2.0%-5.7% |

-0.1 |

% |

70 5 Pittsburgh, PA$904,202 |

6.1%0.0 |

% |

-12.0%2.6% 1.1%54 -9 |

Portland, OR$1,459,821 2.0 |

% |

2.3% |

13.1% |

3.6% |

-2.4%24 |

-2 |

Providence, RI |

$1,714,243 |

6.3% |

-9.9% |

-11.6 |

% |

-8.6% |

-4.1%38 5 |

Riverside, CA$

| 1,723,962 0.5%-3.1 |

%-6.4%-11.0% |

-12.3% |

58 -1 |

Sacramento |

, CA$1,721,234 |

2.8 %11.3 %12.3%-3.6%3.0%32 8 San Antonio |

, TX$ |

968,344 5.1 |

% |

5.5% |

-8.6% |

0.4%0.5 |

%74 6 San |

Diego, CA |

$3,771,304 |

2.7% |

22.5% |

9.6% |

-3.5 |

% |

-7.7%31 |

2 San Francisco

| , CA |

$6,648,922 |

6.0% |

45.9 |

% |

46.3% |

5.5% |

-11.5%13 |

-2 San Jose, CA

| $5,654,565 4.4%2.7 |

%-2.4%7.6% |

-5.5% |

9 0 Seattle, WA |

$2,992,812 |

3.1% |

-14.8%-13.0%0.6%13.9 |

%10 5 St. Louis, MO |

$1,028,596 |

10.9% |

6.4% |

-1.7% |

1.7% |

4.7% |

11 |

-7 |

Tampa, FL |

$1,650,875 |

15.6% |

20.8% |

27.4 |

% |

-2.9% |

-0.5%33 |

0 |

Virginia Beach, VA$ |

1,105,952 |

9.5% |

-5.9% |

-7.3 |

% |

-1.8%-0.4%39 7 Warren |

, MI |

$1,052,067 |

4.5% |

17.7 |

% |

5.6% |

28.2% |

20.5%22 |

1 Washington, DC

| $2,040,078 3.0% |

5.2%6.9%0.7% |

0.7% |

24 -4 West Palm |

Beach |

, FL$4,510,196 1.3% |

18.5%9.5%-0.6

| %-5.2%94 2 United States of America$1,374,470 4.7% |

5.2% |

2.0% |

1.0% |

0.4% |

49 |

5 |

|