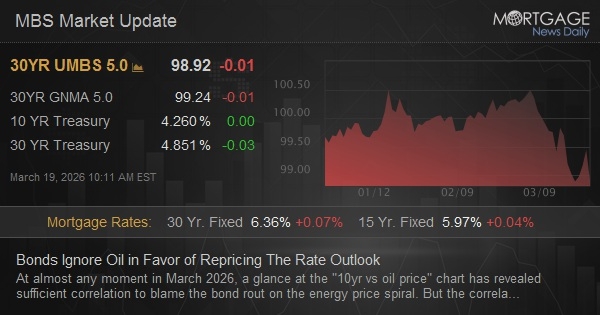

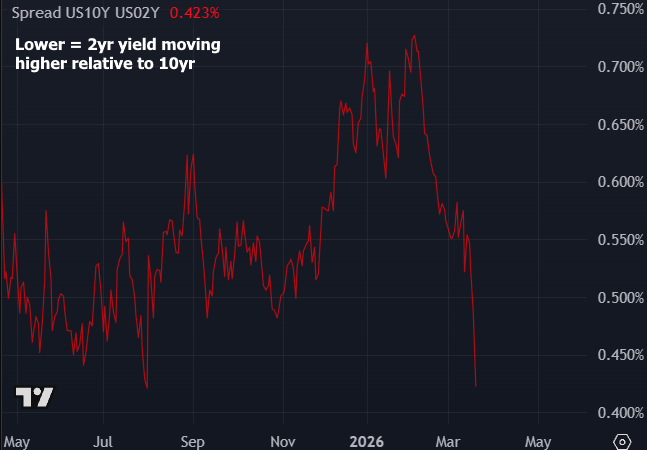

At nearly any minute in March 2026, a look at the “10yr vs oil cost” chart has revealed sufficient connection to blame the bond rout on the energy cost spiral. However the connection is spotty sometimes and today is among the starkest examples. Oil is essentially flat while bonds surged to greater yields overnight. We do not generally focus much on 2yr Treasuries, however the selling there is much even worse than in the 10yr, reflecting a quickly altering outlook for the Fed Funds Rate. Undoubtedly the odds of a rate walking (not cut) in April rose from just over 4% to just over 10% this morning. The big shifts in the 2s vs 10s yield curve speak to the same phenomenon. Oil prices and econ information are easily being hushed by this large scale repositioning for “greater for longer” short-term rates.

< img src="http://a.mbslive.net/assets/69bbf2197e6b4ed5bff13bc7/69bbf2197e6b4ed5bff13bc7.png" alt="20260319 open2.png"/ > < img src="http://a.mbslive.net/assets/69bbf2137e6b4ed5bff13bc6/69bbf2137e6b4ed5bff13bc6.png" alt="20260319 open.png"/ > < img src="http://a.mbslive.net/assets/69bbf21f7e6b4ed5bff13bc8/69bbf21f7e6b4ed5bff13bc8.png" alt="20260319 open3.png"/ >