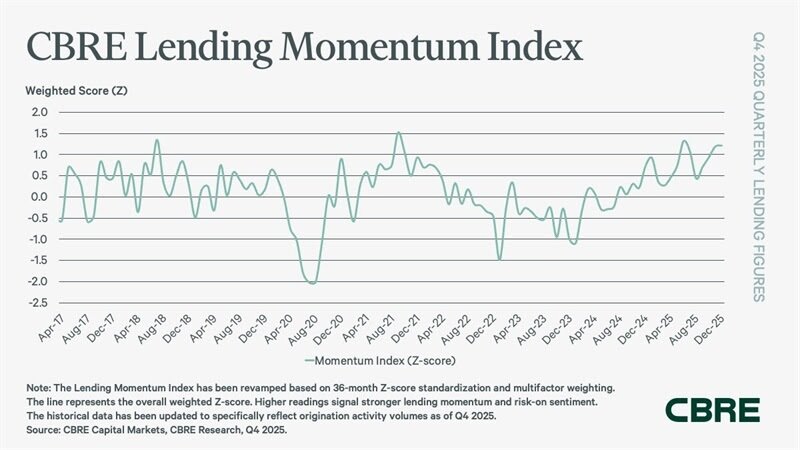

Loan originations accelerated dramatically in the 4th quarter, with CBRE’s Lending Momentum Index climbing 67% from a year earlier to 1.2– roughly in line with pre-pandemic activity levels seen in 2018. The rebound was fueled in part by a 26% increase in long-term funding, with December publishing the greatest regular monthly volume since 2021.

Loaning expenses and credit conditions remained broadly steady. Commercial home mortgage spreads held at 197 basis points during the quarter, while multifamily spreads edged up a little to 142 basis points. At the same time, modest enhancements in underwriting metrics signified a very carefully improving danger environment: financial obligation service protection ratios ticked greater, and both loan constants and home loan rates decreased from the previous quarter.

Still, the healing stays unequal underneath the surface area. “The marketplace is bifurcated however progressively healthy,” stated James Millon, CBRE’s U.S. and Canada capital markets co-head, keeping in mind that increasing delinquencies and legacy loan sales are being soaked up by deep swimming pools of liquidity. Tightening up credit spreads and near-full participation throughout lender types highlight the sector’s improving footing.

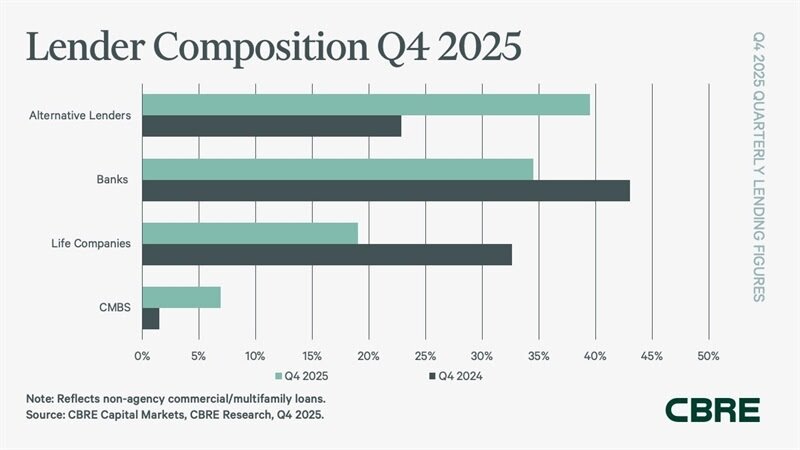

Alternative lending institutions continued to broaden their footprint, accounting for 40% of non-agency loan closings– up sharply from a year previously. Debt funds drove much of that growth, with volumes more than doubling year-over-year. Banks, while still active, delivered share to these personal credit gamers even as their own origination volumes rebounded on a quarterly basis.

On the other hand, securitized loaning staged a significant comeback. CMBS issuance rose in 2025, with annual volumes reaching $158 billion– the highest given that 2007– lifting CMBS lenders’ share of non-agency originations to 7%, up from just 1% a year earlier.

Leverage levels likewise crept higher, showing a modest shift towards less conservative lending. Typical loan-to-value ratios increased to 60.9% for business assets and 66.2% for multifamily homes, suggesting loan providers are gradually loosening constraints as confidence improves.

Government-backed multifamily lending remained a pillar of the market. Company volumes increased to $55 billion in the fourth quarter, pressing full-year originations to $150 billion– up 25% from 2024. At the exact same time, agency mortgage rates declined to approximately 5.3%, even more supporting borrowing activity.

The data point to an industrial property credit market regaining traction after a duration of tension, with liquidity deepening even as legacy threats continue to work their way through the system.