< img src =" https://cdn9.areadevelopment.com/article_images/id71366_capitalizing-on-the-OBBBA1000.jpg" alt=" "> As the 2026 tax season techniques, designers and tax advisers are preparing for the first filing cycle that will completely show the One Big Beautiful Bill Act. Signed into law on July 4, 2025, the OBBBA changes the economics of commercial development in ways that are both generous and deadline-driven, broadening front-end reductions while speeding up the expiration of key building-efficiency rewards.

Associated Research study

For taxpayers in the understand, the 2025 tax year filed in 2026 marks the opening of a rare “golden window”: a brief duration in which restored capital expensing overlaps with the final months of certain energy-related advantages before a mid-2026 cliff. For the modular sector, the OBBBA is more than a tax cut. It is a policy environment that rewards speed, documents and disciplined classification, all areas where modular projects can hold a useful benefit when tax planning matches build technique.

Bonus Offer Depreciation and Expanded Section 179

The OBBBA’s most immediate impact is the repair of bonus devaluation. Under the phase-down schedule following the Tax Cuts and Jobs Act, benefit depreciation was diminishing, dropping to 60 percent in 2024 and 40 percent in 2025. The OBBBA halted the decline. For certified residential or commercial property acquired after Jan. 19, 2025, and put in service in the applicable taxable year, bonus offer devaluation is brought back to 100 percent, based on statutory timing rules, shift elections and special guidelines appropriate to self-constructed residential or commercial property.

The real benefit is not a label; it is the ability to develop a reputable record and place possessions in service on a foreseeable timeline.

The brand-new law also expands Section 179, increasing the expensing cap to $2.5 million and the phaseout threshold to $4 million. For middle-market operators deploying modular options, guardhouses, administrative space, medical clinics and other specialized centers, this can equate into meaningful Year 1 reductions for certifying property placed in service, presuming the taxpayer can use the deduction under applicable income and entity-level constraints.

Together, these provisions can materially enhance early-year cash flow. But the OBBBA’s most attractive outcomes are manual. They depend upon what qualifies, how expenses are classified and whether the taxpayer can support those positions if challenged.

Modular Edge

Modular construction is not immediately dealt with as concrete personal effects, and taxpayers need to be skeptical of any plan that assumes the structure itself becomes expensable just due to the fact that it was put together offsite. Nonresidential real property normally remains subject to a 39-year recovery duration, no matter delivery approach.

Where modular can exceed is in the useful conditions it develops, particularly compressed schedules, lowered onsite irregularity and clearer component-level procurement records. Those functions can support more defensible cost allocations into shorter-lived classifications, typically through a strenuous cost-segregation approach, specifically where tasks include systems and possessions that may qualify for much shorter healing periods and possibly for instant expensing under perk devaluation when properly validated.

100%

That’s the restored benefit devaluation readily available for qualifying residential or commercial property placed in service after Jan. 19, 2025.

In narrower scenarios, especially where units are really developed and utilized as relocatable, arguments for personal-property treatment might be supportable. However those outcomes are fact-specific and need to never ever be presumed. In the OBBBA period, the real advantage is not a label; it is the capability to develop a reputable record at the part level and location possessions in service on a predictable timeline.

Classification Discipline: What the Internal Revenue Service Will Anticipate to See

The IRS identifies real estate from tangible personal effects through a multifactor, fact-intensive analysis that frequently thinks about permanence, the manner of affixation, planned duration of use and the practical repercussions of elimination. In that framework, an all-or-nothing claim that a whole modular center is devices is normally the most susceptible posture.

Modular building and construction does not turn buildings into devices, but it can make category more defensible.

A more powerful technique is generally component-based: categorize assets by function and combination, supported by meaningful job documents and an engineering-driven approach. Authorities typically relied upon in this area, consisting of Medical facility Corporation of America v. Commissioner, 109 T.C. 21 (1997 ), enhance the proposition that category switches on practical use instead of form or marketing characterization.

If relocatability is meant to matter in the analysis, it must appear regularly in the project’s realities: style options such as demountable connections, structures engineered for removal where possible, operational plans and records that align with the declared use. These aspects can reinforce the case, but they do not eliminate the requirement for disciplined cost-segregation support and audit-ready documentation.

Certified Production Home: A Brand-new Tool for Industrial Growth

The OBBBA also presents Qualified Production Residential or commercial property, which in specified circumstances can extend 100 percent expense treatment to certain production-related real property where construction begins after Jan. 19, 2025, and before Jan. 1, 2029, and the property is positioned in service before Jan. 1, 2031, supplied the residential or commercial property is an important part of qualifying production activity. For makers broadening domestic operations or industrial customers constructing centers integral to qualifying production activity, QPP might materially enhance expense healing and narrow the historical gap in between walls and devices.

QPP is definition-driven, compliance-intensive and subject to regain if the property ceases to satisfy statutory usage requirements during the applicable compliance period. Effectively applied, it can be effective; applied casually, it can produce threat that remains well beyond the year of building.

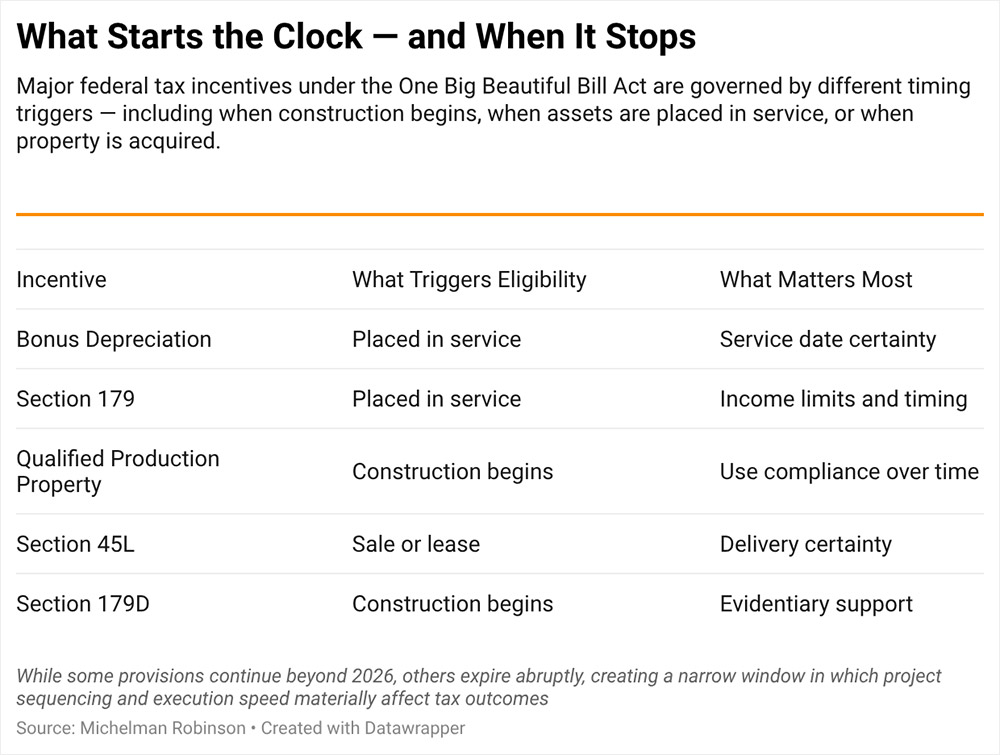

The June 30, 2026, Cliff: Two Rewards, Two Different Timing Standards

The OBBBA likewise accelerates the expiration of two significant building-efficiency provisions: Section 45L, the New Energy Efficient Home Credit, and Area 179D, the Energy Effective Business Structures Reduction. Both sunset June 30, 2026, however the timing rules vary, and that distinction will form job sequencing.

June 30, 2026

That’s the deadline for Sections 45L and 179D before major energy rewards end.

For Area 45L, eligibility generally switches on whether a certified home is obtained through sale or lease, consistent with program requirements, by the deadline. The credit is typically discussed as up to $2,500 to $5,000 per system, depending upon the credentials path and appropriate requirements, but the useful problem is schedule certainty. Conventional multifamily jobs may deal with material danger of missing the acquisition due date. Modular tasks, due to the fact that they compress schedules and lower variance, are typically much better positioned to provide and document certifying acquisition events within the window.

For Section 179D, the sundown is keyed to whether construction starts by the due date. Jobs that please the standard might be grandfathered into the deduction regime, subject to statutory requirements and future assistance. Taxpayers might want to “begin building” ideas used in other federal incentive routines as reference points, but prudent counsel needs to treat this as an evidentiary requirement instead of a presumption, particularly till Treasury and internal revenue service assistance clarifies how the guideline will be applied here.

Supply Chain Compliance: A Smaller Area With Bigger Effects

The OBBBA likewise highlights an industrial-policy reality: rewards significantly include supply chain and counterparty scrutiny. Domestic-content rules are credit-specific, but where they use, taxpayers may require substantiation that structural steel and iron production procedures take place in the U.S. and that produced items fulfill developing domestic-sourcing thresholds frequently determined through cost-based tests.

Incentives reward speed and documents, not assumptions.

Layered on top are restrictions connected to forbidden foreign entities and associated foreign-influence concepts that use on a credit-specific basis, with reliable dates and thresholds that vary by regime. Sometimes, the danger consists of regain, not simply disallowance.

For modular companies incorporating advanced systems such as storage, controls and high-efficiency a/c, the takeaway is direct: traceability is now a tax problem. Contracts ought to assign compliance obligation plainly through representations, covenants, audit-cooperation obligations and indemnities aligned with the parties best placed to manage sourcing danger. Developers need to likewise remain conscious that jobs utilizing HUD Community Preparation and Development financing might implicate Build America, Buy America Act requirements, based on implementation guidelines and offered waivers.

Broaden  Close < img alt =" What Begins the Clock" src =" https://www.areadevelopment.com/taxesIncentives/q1-2026/"/ > What Starts the Clock

Close < img alt =" What Begins the Clock" src =" https://www.areadevelopment.com/taxesIncentives/q1-2026/"/ > What Starts the Clock