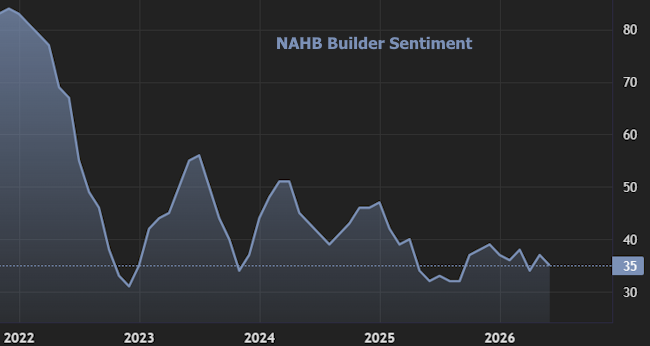

Contractor sentiment slipped once again in June as elevated home loan rates, greater material expenses and ongoing affordability pressures continued to weigh on the housing market. The National Association of Home Builders (NAHB)/ Wells Fargo Real Estate Market Index (HMI) fell 2 points to 35, marking the 14th straight month the index has stayed listed below 40.

The most recent reading underscores how far confidence remains from more long lasting levels. A streak that long below 40 has not been seen considering that 2011-2012, when the market was still handling the fallout from the foreclosure crisis.

All three significant elements of the index were either lower or unchanged. Current sales conditions slipped 2 points to 38, while sales expectations over the next 6 months held consistent at 45. Traffic of potential purchasers remained the same at 25, suggesting demand is still soft despite the start of the summertime selling season.

“With the nation short about 1.2 million homes, home builder belief will stay soft till barriers are reduced and conditions improve for home structure,” stated NAHB Chairman Bill Owens. He stated Congress could assist by advancing the significant housing package now before the Senate, in addition to legislation aimed at reducing labor shortages and securing access to natural gas in new homes.

NAHB Chief Economic expert Robert Dietz said regulative and policy costs continue to make it harder for home builders to include supply. He indicated a new NAHB research study revealing that federal government guideline, taxes, charges and other costs include more than 26% to the price of an average single-family home, arguing that reducing allowing hold-ups, density limits and zoning constraints would help reduce costs.

Prices pressure remained visible in the most recent survey. In June, 35% of contractors reported cutting costs, up from 32% in Might, while the typical price reduction held at 6%. The use of sales incentives likewise edged higher to 62%, the 15th consecutive month that share has actually reached at least 60%.

Regional three-month moving averages were mixed however mainly lower. The Northeast increased 2 indicate 44, the Midwest held at 43, the South slipped 2 points to 33 and the West fell one indicate 27. In general, the report suggests contractors are still awaiting a more significant improvement in cost and expense conditions before confidence can recover.