Residential building and construction activity was mixed once again in April, as building permits rebounded while housing starts pulled back modestly from March’s more powerful rate. The current Census Bureau data continues to reflect a building and construction sector navigating uneven demand and cost pressures.

Independently owned housing starts fell 2.8% to a seasonally adjusted annual rate of 1.465 million, below March’s modified 1.507 million rate. Regardless of the regular monthly decline, starts were still 4.6% greater than April 2025 levels. Single-family starts dropped 9.0% to 930k, while multifamily starts (buildings with five systems or more) increased to 529k.

On the permitting side, activity recovered after March’s sharp decline. Total building authorizations rose 5.8% to a yearly rate of 1.442 million, though that was still 0.2% below year-ago levels. Single-family permits decreased 2.6% to 872k, while multifamily authorizations reached 514k.

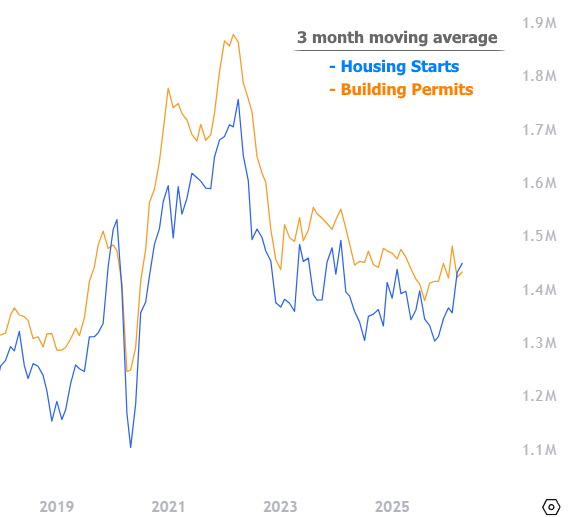

As is typically the case with this information series, month-to-month swings can overemphasize the hidden pattern. More broadly, domestic building activity has stayed relatively steady over the past year, with contractors continuing to stabilize raised funding expenses, cost challenges, and uneven purchaser demand. In fact, if we smooth the information with an easy 3-month moving average, it’s much easier to see a decent little rebound from the long term lows last Fall. In this light, housing starts are the greatest they have actually been since early 2024.

Housing completions increased 4.8% in April to a seasonally changed yearly rate of 1.449 million. Even with the month-to-month gain, completions were still 2.0% lower than the same time last year. Single-family conclusions slipped 1.0% to 903k, while multifamily completions was available in at 529k.

The April report recommends builders remain active, especially on the multifamily side, even as single-family building and construction showed some signs of cooling after March’s rebound.