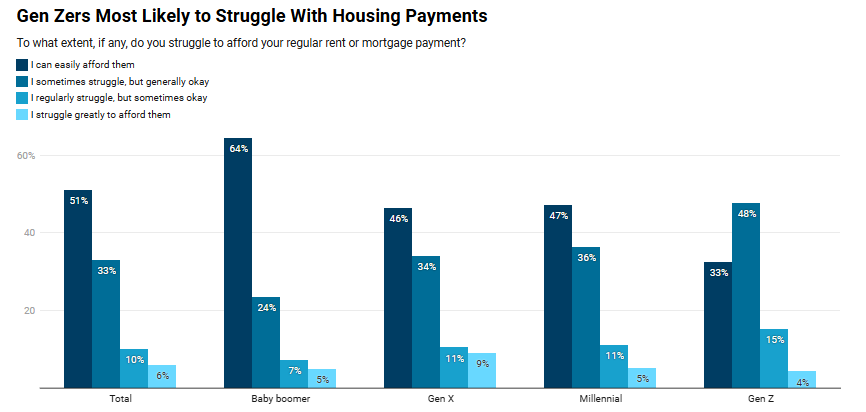

The survey exposes that 49% of U.S. citizens report difficulties in staying up to date with their real estate expenses, up from 44% in a similar study last spring. The strain is disproportionately felt by younger generations, with two-thirds of Gen Z adults– those born in between 1997 and 2012– confessing to significant difficulties, compared to just over half of millennials and Gen Xers, and only about a 3rd of infant boomers.

Carried out by Ipsos on behalf of Redfin in November 2025, the study polled 4,000 grownups across the country. Respondents were classified as having a hard time if they described their scenario as either a “fantastic battle” to pay for real estate or one where they “routinely battle but are often fine.”

This escalation comes amidst raised home costs and loaning costs that continue to outpace income development. The average U.S. home-sale cost in November hovered at levels needing an annual family earnings of around $111,000 to easily manage a normal residential or commercial property– well above the nationwide average earnings of about $86,000. Home mortgage rates, while off their peaks, remained stubbornly high, contributing to the barriers for prospective purchasers.

“Young buyers are resting on the sidelines due to the fact that of sky-high housing expenses paired with more comprehensive financial jitters,” said Desiree Bourgeois, a premier representative with Redfin in Detroit. “Worries over task stability, possible tariffs, and the danger of declining property values are keeping them out. Newbie homeownership seems like an insurmountable obstacle right now.”

The fallout extends far beyond month-to-month expenses, forcing lots of to make tough trade-offs in their lives and long-lasting plans. Among those facing affordability problems, 39% have cut back on dining out, while 34% are giving up vacations. More than one in six are getting additional work hours or offering individual products to make ends satisfy.

The sacrifices can be a lot more extensive: 15% report skipping meals, 14% are delaying needed healthcare, and smaller shares– around 4% each– are delaying starting households or relinquishing pets to alleviate financial pressure.

Gen Z bears the brunt of these adjustments. In this group, 35% are eating out less regularly, 18% are skipping meals completely, one in 5 have offered possessions, 18% have taken on side gigs, and 15% have returned to live with parents to cope.

These pressures are likewise wearing down paths to homeownership, a foundation of the American dream. Just 27% of Gen Z adults own homes, far listed below the rates for older friends: over half of millennials, and more than 70% for both Gen X and child boomers.

Yet, there are tentative signs of reducing ahead. Homeownership among more youthful Americans edged up slightly in 2025, buoyed by modest improvements in affordability. Economists anticipate further relief in 2026, with home mortgage rates expected to settle around 6%, home-price gratitude slowing down, and wages possibly rising faster than real estate costs.

Nevertheless, the study highlights a widening gorge between skyrocketing real-estate expenses and stagnant earnings, specifically for those at the entry level of the market. For numerous young Americans, incremental way of life tweaks are proving inadequate to close the divide, raising wider concerns about economic movement in a post-pandemic era.