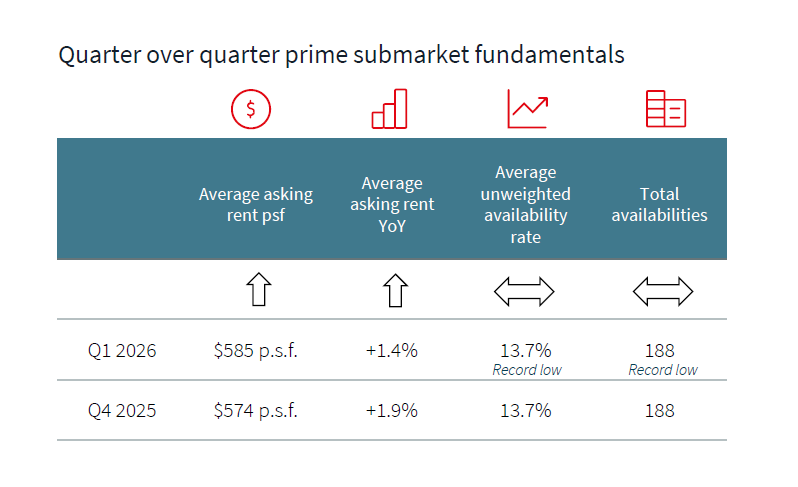

Average availability throughout crucial shopping districts– consisting of Fifth Opportunity, SoHo and Times Square– held at 13.7% in the very first three months of 2026, matching the previous quarter and marking the lowest level since tracking began in 2017.

The continued tightening highlights a multi-year recovery in New York retail, with job rates down dramatically from pandemic-era highs. Yearly average availability has actually fallen from more than 21% in 2019 to roughly 14% in 2025, reflecting consistent absorption of area throughout prime passages, according to JLL.

Leas, however, are showing a more fragmented image.

Average asking rents across prime submarkets edged as much as $585 per square foot in the first quarter, a modest increase from $574 in the previous period and broadly in line with 2025 levels. But performance differed widely by area, highlighting a market still adjusting to shifting foot traffic patterns and consumer behavior.

Downtown communities led the tightening up. SoHo accessibility dropped to a record low 9.1%, while the Meatpacking District and Herald Square likewise posted decreases in available area. At the very same time, rents in the Meatpacking District jumped 11% quarter-over-quarter and are up more than 20% from a year earlier.

By contrast, some of the city’s most popular retail passages showed softness. Asking leas fell on Madison Opportunity and in SoHo throughout the quarter, while Times Square– still contending with raised vacancy– saw year-over-year rents decline greatly regardless of a quarterly increase.

The divergence reflects both tenant demand and the progressing mix of merchants going into the marketplace.

Leasing activity in the quarter consisted of a mix of experiential tenants, discount rate retailers and food principles. Large deals included a 54,000-square-foot lease for the Balloon Museum at the Seaport and a 47,000-square-foot deal by Chelsea Piers in Hudson Square, signaling continued demand for destination-oriented uses.

Still, broader financial signals point to a more cautious consumer background.

Economic activity softened somewhat in early 2026, with flat work and modest wage development, while customer spending increased just partially. Homes remained price-sensitive, often going shopping across numerous outlets to discover value.

Weather condition likewise contributed, with a severe winter season dampening foot traffic and weighing on smaller sized retailers, even as food and beverage operators saw some strength.

The result is a retail market defined by constrained supply however selective need– where prime space is increasingly limited, yet pricing power remains uneven.

JLL states that dynamic is most likely to persist through 2026, as property owners balance restricted schedule with occupants navigating a still-fragile consumer environment.