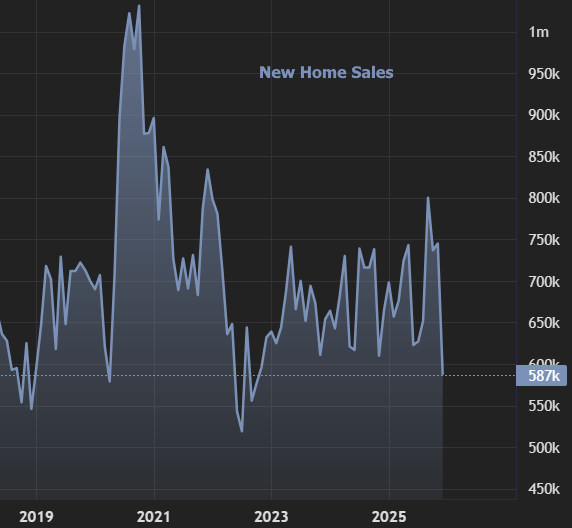

New home sales took a significant action back in January, reversing much of the previous month’s strength and highlighting the volatility that frequently specifies this data series. The Census Bureau reported a seasonally adjusted annual rate of 587,000, down sharply from December’s 712,000 and 11.3% lower than January 2025.

For-sale inventory moved somewhat greater to 476,000, up 0.4% from December however still 4.0% below year-ago levels. At the present sales rate, months’ supply leapt to 9.7 months, up from 8.0 months in December and 9.0 months one year ago. The increase reflects the mix of softer demand and relatively steady stock levels.

Costs decreased on both a month-to-month and yearly basis. The median list prices fell to $400,500 (-4.5% MoM; -6.8% YoY), while the average rate dropped to $499,500 (-5.9% MOTHER; -3.6% YoY). The pullback suggests a shift in the mix of homes offered, with less upward pressure from higher-priced transactions.

- Sales (MOMMY): -17.6%

- Sales (YoY): -11.3%

- Inventory (YoY): -4.0%

- Months’ Supply: 9.7 (up from 8.0 previous month; 9.0 YoY)