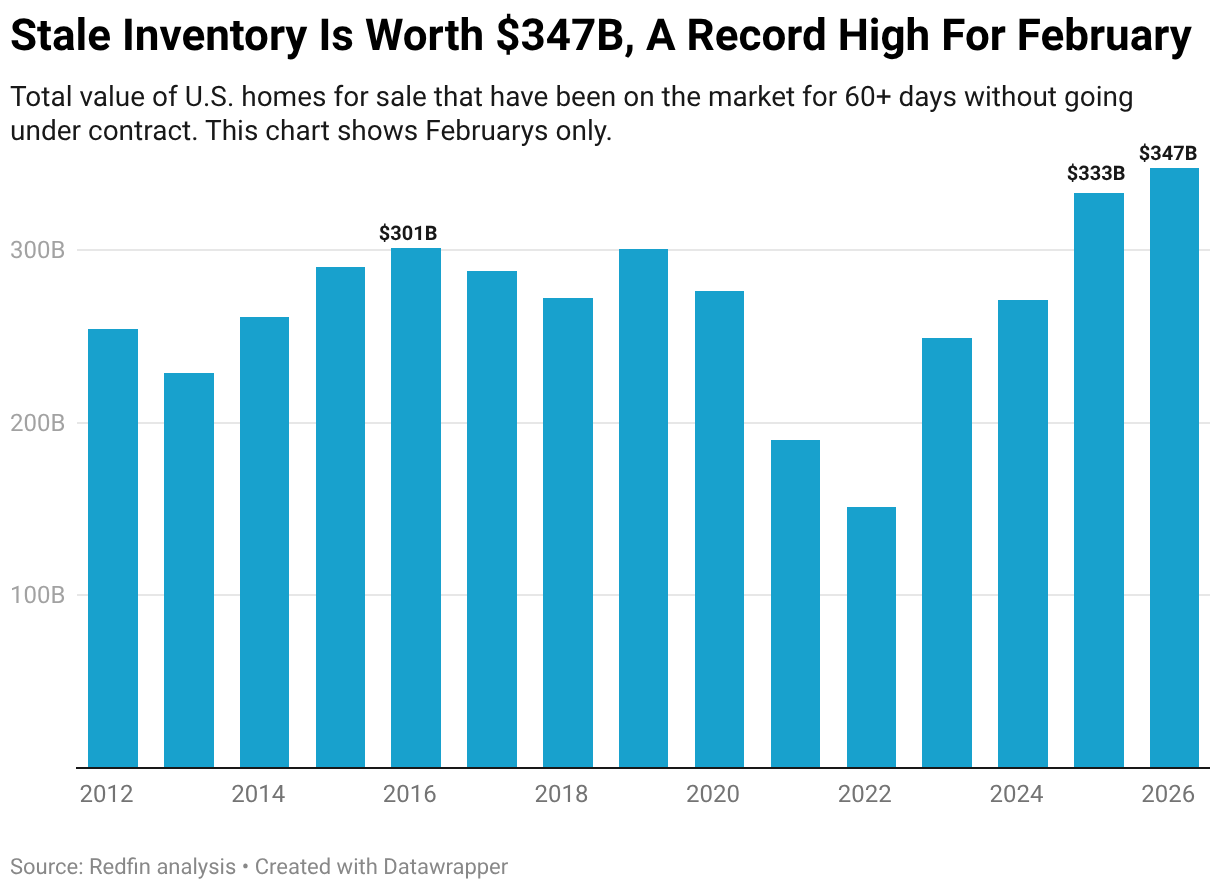

- In dollar terms, there’s$347 billion worth of stagnant listings in the U.S., more than ever before for this time of year. That’s since there are hundreds of thousands more home sellers than buyers, resulting in homes sitting on the marketplace.

- Stagnant inventory is most typical in Florida, and least common in the Bay Location.

- Through Redfin’s new collaboration with Compass, sellers can work to prevent stagnant listings by testing the marketplace, which might minimize the risk of homes remaining on the market.

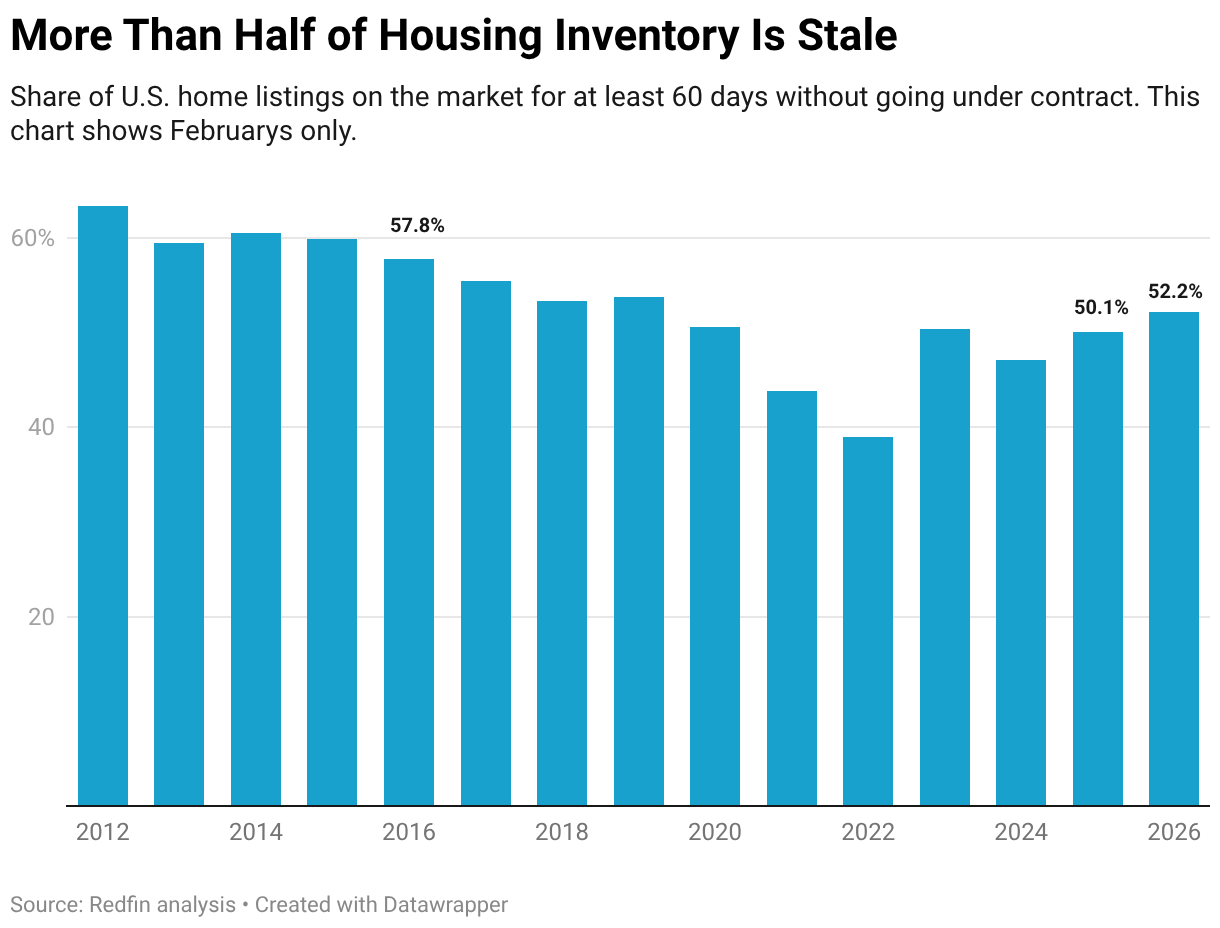

Majority (52.2%) of February’s home listings were on the market for a minimum of 60 days without going under contract (i.e. they were stale) nationwide, up from 50.1% a year earlier and the greatest share because 2019.

This is based on an analysis of listings on Redfin.com returning through 2012. For the overall dollar worth of all stock on the market, we summarize the sale price of all active U.S. listings since the last day of every month; February 2026 is the most current month for which data is offered. We specify “stagnant inventory” as home listings that invest a minimum of 60 days on the market and are actively noted for sale on the last day of the relevant month. This data is seasonal, which is why we compare February to previous Februarys. Please see completion of this report for more on methodology.

Home Sellers Are Sitting on $347 Billion Worth of Stale Listings, a Record High For This Time of Year

In dollar terms, there’s a total of $347 billion worth of stale inventory on the marketplace nationwide. That’s up 4.3% yearly and the greatest dollar amount on record for this time of year.

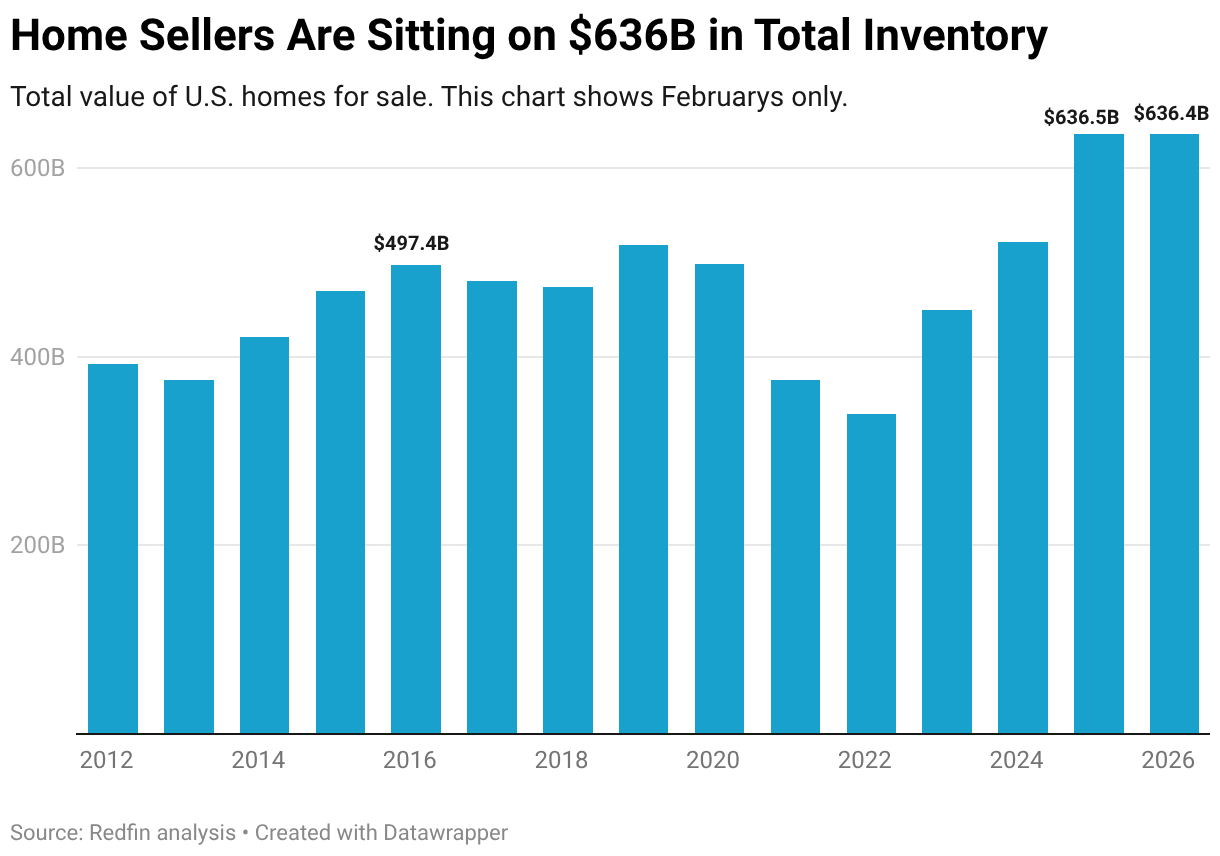

There’s a Total of$636 Billion Worth of Homes For Sale in the U.S. Zooming out to all inventory, there’s a total of$636 billion worth of homes for sale, essentially unchanged from a year earlier. Like stagnant inventory, that’s the greatest dollar amount on record for this time of year (other than 2025, when it was 0.01% higher).

The total worth of stagnant stock– and all inventory– is greater than ever for this time of year since there are a record 630,000 more home sellers than purchasers in the market, extending the amount of time it takes to offer a home. Here are more information:

- Homebuying need is slow. U.S. home sales fell 3.1% year over year in February. House hunters watch out for high home loan rates and high prices, and they’re jittery due to the fact that of financial uncertainty, consisting of worries about layoffs, inflation and the Iran war.

- Home selling is downing along. The overall number of homes for sale is up 1.5% year over year. While some sellers have actually withdrawed, lots of are still in the market, wishing to cash in on still-high home values.

- Days on market are at a record high. The common home that went under contract in February invested 66 days on the marketplace– the slowest speed in a years for this time of year.

- Home costs are increasing. The mean home-sale cost is up roughly 1% year over year. When home costs increase, so does the overall dollar worth of homes for sale, and the overall dollar value of stale stock.

“Sellers understand it’s a purchaser’s market, however they still want to get as much money as they can for their home. So they note on the luxury, anticipating purchasers to work out down, which’s causing listings remaining on the market for a very long time,” stated Jason Wind, a Redfin Premier agent in New Orleans. “There are still deals to be made, but 9 times out of 10, homes are costing under their asking price. But in some cases, the price is just too expensive, and sellers need to pull their home off the marketplace after six months or two.”

Stale Listings Are The Majority Of Common in Miami

In Miami, almost two-thirds (62.6%) of home listings are stale, the biggest share of all the significant U.S. metros. Next come San Antonio (58.3%), Pittsburgh (58.1%) and West Palm Beach (55.9%).

Listings are stagnating in those locations since they are major purchaser’s markets; in Miami, San Antonio and West Palm Beach, there are more than two times as lots of home sellers as buyers.

Stale listings are least typical in the Bay Location. In San Jose, 19.8% of listings are stale, the smallest share among the major metros, followed by San Francisco (24%) and Oakland (31.1%). Next come Anaheim, CA (34%) and Seattle (34.1%). The majority of those are buyer’s markets, however to a much smaller degree than the Florida city listed above; for example, in San Jose, there are just 10% more sellers than buyers. San Francisco is a balanced market, with an approximately equal variety of sellers and buyers.

Letting Home Sellers Evaluate the Waters Before Listing Could Enable Them To Offer Faster

Residences sticking around on the market can have unfavorable effects for sellers; in some cases, buyers are wary of homes that have been on the market for a very long time.

That’s one factor Redfin partnered with Compass on phased marketing, which gives sellers more flexibility in how they present their homes to potential buyers. Sellers can pick to show their homes on Redfin.com with no days on market, no price history and no home assessment price quotes.

That permits sellers to gauge early interest in their property and price properly from the beginning, which we discovered might help sellers in a few methods:

- Lower the risk of listings going stale. Sellers who evaluate rates strategies with phased marketing might be less most likely to see their homes rest on the marketplace. Overpricing your home by 10% or more can increase time on market by more than a month.

- Lower the danger of losing cash from a price drop. Sellers who check prices using phased marketing might be less likely to lose cash via a price cut. Redfin economic experts approximate that homes cost less when they have a price cut due to the preconception.

| Metro-Level Summary: Stale Home Listings, Feb. 2026

Home listings are “stale” if they have been on the market for a minimum of 60 days without going under agreement |

||

| U.S. city area | Total dollar value of stagnant stock | Share of home listings that are stagnant |

| Anaheim, CA | $3,804,979,477 | 34.0% |

| Atlanta, GA | $6,967,001,572 | 51.2% |

| Austin, TX | $4,235,317,502 | 53.4% |

| Baltimore, MD | $1,263,200,842 | 47.7% |

| Boston, MA | $2,754,374,299 | 38.7% |

| Chicago, IL | $3,158,224,864 | 40.9% |

| Cincinnati, OH | $1,048,562,696 | 45.6% |

| Cleveland, OH | $610,000,680 | 49.5% |

| Columbus, OH | $993,323,978 | 44.8% |

| Dallas, TX | $5,947,277,162 | 49.3% |

| Denver, CO | $2,733,851,592 | 40.3% |

| Detroit, MI | $463,118,430 | 54.0% |

| Fort Worth, TX | $2,310,252,422 | 50.6% |

| Houston, TX | $7,687,421,473 | 54.5% |

| Indianapolis, IN | $1,104,438,728 | 53.5% |

| Jacksonville, FL | $2,546,738,082 | 51.3% |

| Las Vegas, NV | $3,906,105,308 | 51.3% |

| Los Angeles, CA | $13,531,277,797 | 44.1% |

| Miami, FL | $15,894,396,237 | 62.6% |

| Milwaukee, WI | $508,495,433 | 36.3% |

| Minneapolis, MN | $1,963,662,229 | 43.7% |

| Montgomery County, PA | $857,609,898 | 43.3% |

| Nashville, TN | $5,190,002,567 | 54.8% |

| Nassau County, NY | $3,522,293,691 | 49.2% |

| Brand-new Brunswick, NJ | $2,152,388,676 | 47.1% |

| New York City, NY | $16,939,740,119 | 55.1% |

| Newark, NJ | $1,006,363,900 | 46.1% |

| Oakland, CA | $903,312,534 | 31.1% |

| Orlando, FL | $4,222,334,231 | 55.7% |

| Philadelphia, PA | $1,179,569,999 | 52.6% |

| Phoenix, AZ | $10,150,809,424 | 46.1% |

| Pittsburgh, PA | $1,158,245,883 | 58.1% |

| Portland, OR | $2,100,910,565 | 48.3% |

| Providence, RI | $796,842,587 | 43.4% |

| Riverside, CA | $5,505,718,830 | 48.8% |

| Sacramento, CA | $1,665,099,987 | 41.8% |

| San Antonio, TX | $3,365,734,572 | 58.3% |

| San Diego, CA | $2,960,305,403 | 37.7% |

| San Francisco, CA | $687,464,464 | 24.0% |

| San Jose, CA | $524,074,518 | 19.8% |

| Seattle, WA | $2,237,074,918 | 34.1% |

| Tampa, FL | $5,980,820,981 | 53.4% |

| Virginia Beach, VA | $977,175,816 | 43.6% |

| Warren, MI | $1,093,257,329 | 46.2% |

| Washington, DC | $3,748,942,561 | 43.9% |

| West Palm Beach, FL | $11,599,537,794 | 55.9% |

| United States of America | $347,358,012,659 | 52.2% |

Methodology

This report is based upon an analysis of listings on Redfin.com going back through 2012. For the overall dollar value of all inventory on the market, we sum up the sale price of all active U.S. listings as of the last day of monthly; February 2026 is the most current month for which data is available. Listings are included in the total if they were included on or before the last day of the month, and are still active (not sold or delisted) as of the last day of the month. Listings were omitted if the list price was greater than $300 million.

For the purposes of this report, the term “value” is interchangeable with “asking cost”; i.e., when we refer to “total home worth,” we imply the amount of all list prices.

For the stagnant inventory area of this report, we define “stagnant inventory” as home listings that invest a minimum of 60 days on the marketplace and are actively noted for sale on the last day of the relevant month. Listings that have actually been on the market for more than one year are left out from the analysis.

The data in both the dollar value and stale stock areas of this report tend to be seasonal; they are usually higher during the spring and summer, and lower in the winter.