The reliable tariff rate as of the first half of 2025 is currently around 4 times higher compared to the historical quarterly average throughout the 30-year period from 1995– 2024. Countries throughout APEC, an area that contributes over two-thirds of U.S. imports annually, deal with high tariff rates regardless of worked out trade deals that are currently in location. For instance, countries like Brunei and Singapore, with no trade handle location, deal with a 25 percent rate (mutual for the former and secondary for the latter). South Korea, in spite of having a trade offer, still deals with a 15 percent tariff rate.Related Research The effects of such trade policy on last products in retail are quite direct: greater costs cause customers to pull back costs, moistening perhaps not simply short-term demand however likewise long-term need depending on the period of present trade policy. This dynamic might cause brick-and-mortar sellers to reassess their space requires if they believe depressed demand will last for a prolonged period of time. The effects on industrial commercial property, nevertheless, are maybe less obvious. Nonetheless, the passthrough system between items need and space demand for these 2 property types is now increasingly comparable. Even with trade offers and exemptions, commercial properties in the U.S. have felt the effects. Some coastal markets are seeing performance degeneration far above nationwide averages. Normally speaking, broad

macroeconomic headwinds have resulted in sharp boosts in storage facility and circulation vacancies, plateauing lease development

, and net negative absorption in many markets. Tariffs have actually only contributed to the pressure, as storage facility and circulation area demand depends on storage and shipment need for both intermediate items and final items. While causation associated to tariffs is too strong of a conclusion, there is clear correlation. Some West Coast markets have actually experienced efficiency wear and tear that substantially surpasses that of the national average. For instance, while the U.S. has only seen a 50-basis-point increase in the storage facility and distribution vacancy rate year-over-year(see Figure 1), Los Angeles and Oakland– East Bay both exceeded 100-basis-point boosts in the same metric even though inventory growth for both metros was below that of the national figure. However, other markets (e.g., San Diego and San Francisco)are on par or even show lower year-over-year vacancy rates, showing a tightening market with adequately robust demand even with inventory development that surpasses the nationwide number, as is the case for San Diego. This pattern extends beyond the West Coast. Port cities along the East Coast whose daily tonnage is typically skewed towards global freight, like Philadelphia, are also feeling the impact. Expand Close Job and Inventory Still, tariffs are only one factor behind damaging storage facility and circulation efficiency. Oftentimes, greater job

rates, and the accompanying

weak point in lease growth, are more directly attributable to the amount of speculative square footage that has actually come online, despite a general downturn in the new-supply pipeline nationally. Norfolk/Hampton Roads and Savannah are 2 prime examples as both markets have experienced outsized stock growth year-over-year. Flex and R&D area remain more insulated even as other industrial subtypes soften. Two significant headwinds for warehouse and distribution demand development persist, both tied to final durable goods spending

: weak consumer belief over raised inflation expectations, and the interaction in between rates of interest and

loaning costs, which has added to the plateauing of e-commerce growth. The University of Michigan Index of Customer Sentiment shows quickly declining self-confidence. The November 2025 reading stands at 50.3– just shy of the record low of 50.0 in July 2022– as customers worry about food and items rates this holiday. Much of that concern relates

to inflation that has yet to meaningfully reach the policy target. Meanwhile, over the previous four quarters of information, from the 3rd quarter of 2024 to the 2nd quarter of 2025, e-commerce’s share of retail sales has actually held steady, just above 16 percent, oscillating in between 16.1 percent and 16.3 percent. The record high of 16.3 percent, very first reached in the 2nd quarter of 2020, was only matched again in the second quarter of 2025. 4 That’s the variety of times present tariff rates exceed the 30-year historical average. Flex and research study and advancement( R&D)homes have actually been a significant exception to such weakening efficiency. As their name suggests, they offer more versatility. From retail to workplace to warehousing for smaller sized enterprises, flex area provides

a more dynamic environment and a smaller footprint for businesses to scale up or down

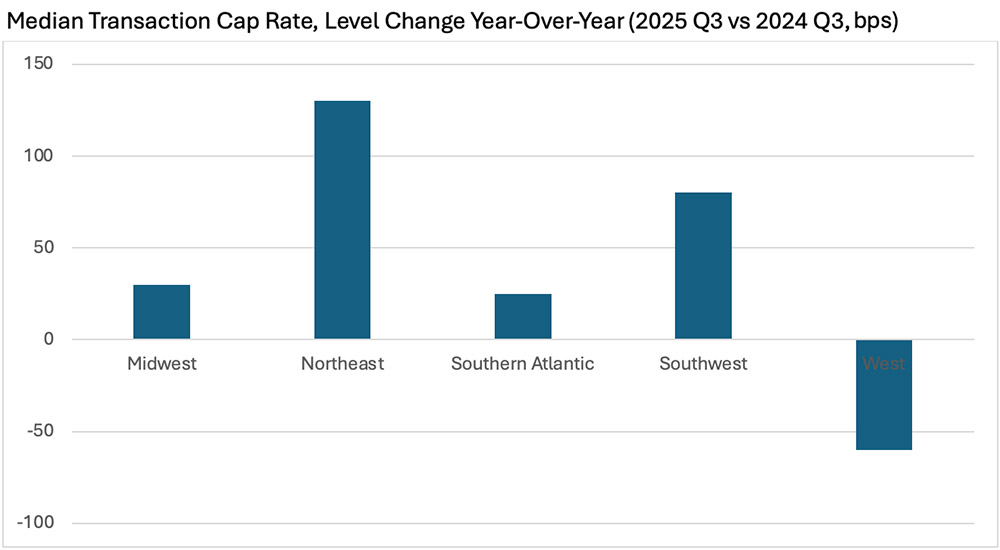

with ease. Thus, although this commercial subtype has actually been even more insulated, data from the 2nd half of 2025 is starting to suggest a softening due to this intermingling of uses and blurring of lines, offered the pile of the abovementioned macroeconomic aspects. Tariffs have actually included pressure to storage facility need even as wider economic forces drive vacancies greater. Turning to activity in the capital markets for the storage facility and distribution subsector, deal volume has actually picked up year-over-year in the West, both by nominal dollar amount and residential or commercial property count. While activity stays more muted than years past, deal volume is up 17 percent from

the third quarter of 2024 to the third quarter of 2025 and the mean transaction cap rate is down 60 basis points

over the exact same period although the 10-year Treasury yield increased by 30 basis points. The other areas of the nation have not been as lucky, with either decreasing transaction volumes or increasing cap rates, or both. However, the South Atlantic, the just other region to experience a boost in transaction volume over the previously mentioned duration, saw average transaction cap rates increase simply 25 basis points, on par with the 10-year Treasury yield, implying that the danger premium over the risk-free rate stayed the same. Expand Close Median Transaction Cap Rate Although demand softening has caused a sharp deceleration in the

quantity

of square

year, in addition to square footage under building and construction, investor hunger for existing residential or commercial properties stays strong. Considerable commercial portfolios are trading across the country, with specific financier interest in newer construction that offers functions like greater ceiling clearance and advanced automation abilities. Regardless of continuous issues regarding evaluations due to the present interest-rate and Treasury-yield environment, in the wake of slowing, and in some pockets, stagnant, net operating income development, industrial portfolios are finding access to capital with loans issued for brand-new purchases and refinancing. This durability is largely due to very little debtor distress throughout the commercial sector. Delinquency rates remain low(the lowest across all of the core home types)– just 1.5 percent as of September 2025– indicating momentary headwinds instead of a long-term downward trend.

of square

of square