< img

src=” https://cdn.propertyupdate.com.au/wp-content/uploads/2022/11/renting-property.jpg” alt=” “>< img src =" https://propertyupdate.com.au/wp-content/themes/oldpaper/img/keys.svg" alt=" crucial takeaways"/ > Secret takeaways Australia’s nationwide domestic job rate was up to 1.1% in February 2026, down from 1.2% in

January and notably below February 2025( 1.3 %). The overall number of property vacancies decreased to 34,572 residences, suggesting continued tightening in rental market conditions

throughout many capital cities. The February outcome recommends that the seasonal tightening up usually observed at the start of the year has actually continued and broadened, with strong tenant need absorbing available rental listings to levels listed below what was taped this time in 2015

SQM Research study launched its most current data on property rental property job rates.

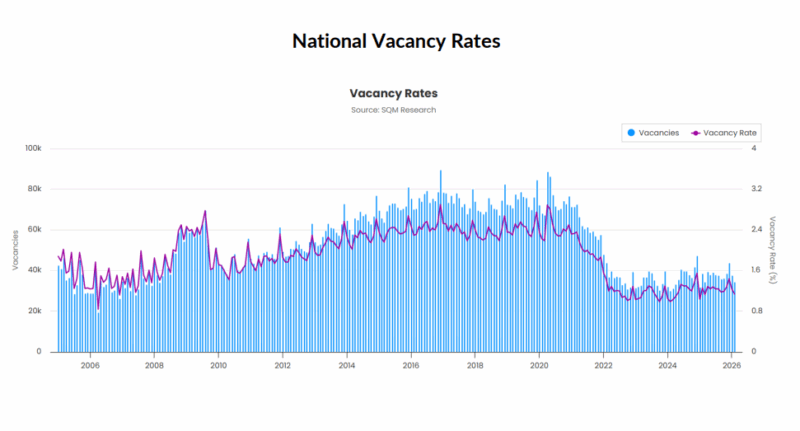

Australia’s national domestic job rate was up to 1.1% in February 2026, down from 1.2% in January and significantly below February 2025 (1.3%).

The total variety of domestic jobs declined to 34,572 residences, suggesting continued tightening up in rental market conditions across the majority of capital cities.

< img src=" https://cdn.propertyupdate.com.au/wp-content/uploads/2026/03/National-Vacancy-rate-February-2026-800x431.png" alt =" National Vacancy Rate February 2026 "width=" 800 "height=" 431 "/ > The February result suggests that the seasonal tightening typically observed at the start of the year has continued and expanded, with strong renter need soaking up available rental listings to levels below what was taped this time in 2015.

Vacancy Rates – February 2026

| City | Feb 2025 Jobs | Feb 2025 Vacancy Rate | Jan 2026 Vacancies | Jan 2026 Vacancy Rate | Feb 2026 Jobs | Feb 2026 Vacancy Rate |

|---|---|---|---|---|---|---|

| Sydney | 11,155 | 1.5% | 10,987 | 1.5% | 9,491 | 1.3% |

| Melbourne | 9,326 | 1.8% | 9,197 | 1.7% | 8,294 | 1.6% |

| Brisbane | 3,445 | 1.0% | 3,339 | 0.9% | 3,002 | 0.8% |

| Perth | 1,201 | 0.6% | 1,153 | 0.6% | 1,130 | 0.6% |

| Adelaide | 1,070 | 0.7% | 1,216 | 0.8% | 1,203 | 0.8% |

| Canberra | 961 | 1.6% | 870 | 1.4% | 688 | 1.1% |

| Darwin | 277 | 1.1% | 195 | 0.8% | 144 | 0.6% |

| Hobart | 174 | 0.6% | 112 | 0.4% | 132 | 0.5% |

| National | 38,427 | 1.3% | 37,630 | 1.2% | 34,572 | 1.1% |

Source: SQM Research

Capital city highlights

Sydney:

Vacancy rates declined to 1.3%, down from 1.5% in January, with 9,491 dwellings available.

The city continues to see strong tenant demand following the summer leasing period.

Melbourne:

Vacancy rates tightened to 1.6%, from 1.7%, with 8,294 jobs recorded.

Rental conditions remain reasonably well balanced compared to other major capitals.

Brisbane:

Vacancy rates tightened a little to 0.8%, below 0.9%, with 3,002 dwellings readily available, maintaining among the tighter markets nationally.

Perth:

Vacancy rates held consistent at 0.6%, with 1,130 residences available.

The city continues to experience strong rental need amid extremely limited new supply.

Adelaide:

Vacancy rates remained unchanged at 0.8%, with 1,203 vacancies recorded.

Supply restrictions continue to keep rental conditions tight.

Canberra:

Vacancy rates decreased to 1.1%, from 1.4%, with 688 homes readily available.

The drop reflects stronger leasing activity in early 2026.

Darwin:

Job rates fell to 0.6%, below 0.8%, with 144 houses vacant, marking among the lowest vacancy levels among the capital cities.

Hobart:

Vacancy rates increased a little to 0.5%, from 0.4%, with 132 homes offered.

Despite the boost, Hobart stays one of the tightest rental markets nationally.

Promoted leas analysis

National promoted rents continued to increase through early March, with combined leas increasing 1.0% over the past 1 month and 6.6% higher year-on-year, reflecting ongoing supply scarcities across a lot of capital cities.

This represents an acceleration in leas compared to the very same period in 2025.

The nationwide combined rent average now stands at $688.76 per week, while the capital city average has actually increased to $782.57, supported by gains in both house and unit leas.

Nationally, house rents rose 1.6% for the month and 7.8% over the year, while unit leas increased 0.1% regular monthly and 4.6% annually, showing stable need for medium-density lodging.

Sydney:

Combined leas rose 0.5% for the month and 7.3% year-on-year, driven by strong home rent development with houses averaging $1,145.45 weekly.

Melbourne:

Integrated leas increased 0.8% regular monthly and 5.0% yearly, supported by continued leasing activity throughout both houses and units.

Brisbane:

Combined leas rose 0.6% for the month and 8.0% over the year, showing sustained population inflows.

Perth:

Integrated rents raised 1.3% month-on-month and 5.5% year-on-year, highlighting the city’s continuous rental supply lacks.

Adelaide:

Combined leas increased 0.3% for the month and 2.8% each year, with house rents balancing $690.13 weekly.

Canberra:

Integrated rents decreased 1.1% over the month and 2.5% over the year, suggesting some short-term reducing in the ACT market.

Darwin:

Integrated leas rose 1.9% for the month and 12.7% annually, representing one of the greatest rental development rates nationally.

Hobart:

Combined rents increased 2.9% for the month and 12.2% year-on-year, reflecting continuous supply restrictions.

Weekly rents index

Sydney

| Property Type | Rent ($) | Weekly change | Regular monthly change | 12 Months change |

|---|---|---|---|---|

| All Homes | $ 1,145.45 | 5.55 | 0.7% | 9.2% |

| All Units | $ 743.84 | 0.17 | 0.2% | 5.4% |

| Combined | $ 906.69 | 2.39 | 0.5% | 7.3% |

Source: SQM Research

Melbourne

| Home Type | Rent ($) | Weekly change | Regular monthly change | 12 Months change |

|---|---|---|---|---|

| All Houses | $ 800.82 | 4.18 | 1.0% | 5.2% |

| All Units | $ 589.73 | 0.28 | 0.7% | 4.5% |

| Combined | $ 678.21 | 1.98 | 0.8% | 5.0% |

Source: SQM Research study

Brisbane

| Property Type | Rent ($) | Weekly modification | Month-to-month change | 12 Months alter |

|---|---|---|---|---|

| All Houses | $ 812.46 | 2.54 | 0.9% | 8.9% |

| All Systems | $ 630.90 | -0.89 | 0.1% | 6.8% |

| Combined | $ 730.67 | 0.99 | 0.6% | 8.0% |

Source: SQM Research study

Perth

| Home Type | Rent ($) | Weekly change | Regular monthly change | 12 Months change |

|---|---|---|---|---|

| All Houses | $ 886.48 | 6.52 | 1.5% | 5.7% |

| All Systems | $ 670.32 | -0.31 | 0.9% | 4.8% |

| Combined | $ 797.27 | 3.75 | 1.3% | 5.5% |

Source: SQM Research

Adelaide

| Home Type | Rent $) | Weekly modification | Regular monthly modification | 12 Months change |

|---|---|---|---|---|

| All Homes | $ 690.13 | 0.87 | 0.0% | 2.3% |

| All Systems | $ 535.37 | -7.38 | 0.8% | 3.9% |

| Combined | $ 637.96 | -1.87 | 0.3% | 2.8% |

Source: SQM Research study

Canberra

| Residential or commercial property Type | Lease ($) | Weekly modification | Month-to-month modification | 12 Months change |

|---|---|---|---|---|

| All Homes | $ 774.51 | -7.51 | -2.0% | -5.5% |

| All Units | $ 583.89 | -0.90 | -0.1% | 1.2% |

| Combined | $ 669.72 | -3.93 | -1.1% | -2.5% |

Source: SQM Research

Darwin

| Home Type | Lease ($) | Weekly change | Month-to-month modification | 12 Months alter |

|---|---|---|---|---|

| All Houses | $ 805.17 | 21.84 | 2.7% | 10.3% |

| All Systems | $ 582.95 | -0.95 | 1.2% | 14.8% |

| Integrated | $ 673.92 | 8.41 | 1.9% | 12.7% |

Source: SQM Research

Hobart

| Property Type | Lease 9$) | Weekly modification | Regular monthly modification | 12 Months change |

|---|---|---|---|---|

| All Homes | $ 610.16 | -0.16 | 2.3% | 9.0% |

| All Units | $ 563.08 | 7.92 | 4.0% | 17.6% |

| Integrated | $ 591.39 | 3.06 | 2.9% | 12.2% |

Source: SQM Research study

National

| Residential or commercial property Type | Lease ($) | Weekly modification | Monthly modification | 12 Months change |

|---|---|---|---|---|

| All Homes | $ 774.36 | 3.63 | 1.6% | 7.8% |

| All Systems | $ 589.50 | 0.50 | 0.1% | 4.6% |

| Integrated | $ 688.76 | 2.20 | 1.0% | 6.6% |

Source: SQM Research study

Cap City Average

| Residential or commercial property Type | Rent ($) | Weekly change | Monthly modification | 12 Months alter |

|---|---|---|---|---|

| All Houses | $ 912.86 | 4.13 | 0.8% | 6.9% |

| All Systems | $ 667.56 | -0.56 | 0.4% | 5.2% |

| Integrated | $ 782.57 | 1.67 | 0.6% | 6.1% |

Source: SQM Research study

The national vacancy rate falling to 1.1% reveals the rental market stays really tight throughout most of the nation.

While some seasonal tightening up is anticipated at this time of year, need for rental housing is plainly continuing to overtake offered supply therefore this relocation exceeds normal seasonality.

Job rates listed below one percent in cities such as Brisbane, Perth and Darwin emphasize just how constrained rental supply remains in parts of Australia.

With marketed leas continuing to speed up greater, the information recommends tenants are still facing strong competitors for available properties.

Without a significant lift in new housing supply and an easing in need, rental pressures are likely to stay a feature of the marketplace through much of 2026, which might feed into the CPI.

< img alt="  Ahmad Imam Square Wide Lo Rez 400. jpglouis Christopher” src=”https://propertyupdate.com.au/wp-content/uploads/2018/02/cropped-Ahmad-Imam-square-wide-lo-rez-400.jpgLOUIS-CHRISTOPHER-148×148.jpg” height=”148″ width=”148″/ > About Louis Christopher Louis is acknowledged as one of Australia’s most respected and impartial research study residential or commercial property analyst. He has extensive understanding and experience of property and is regularly estimated in the media on his insights and is director of SQM Research.Visit www.SQMResearch.com.au

Ahmad Imam Square Wide Lo Rez 400. jpglouis Christopher” src=”https://propertyupdate.com.au/wp-content/uploads/2018/02/cropped-Ahmad-Imam-square-wide-lo-rez-400.jpgLOUIS-CHRISTOPHER-148×148.jpg” height=”148″ width=”148″/ > About Louis Christopher Louis is acknowledged as one of Australia’s most respected and impartial research study residential or commercial property analyst. He has extensive understanding and experience of property and is regularly estimated in the media on his insights and is director of SQM Research.Visit www.SQMResearch.com.au