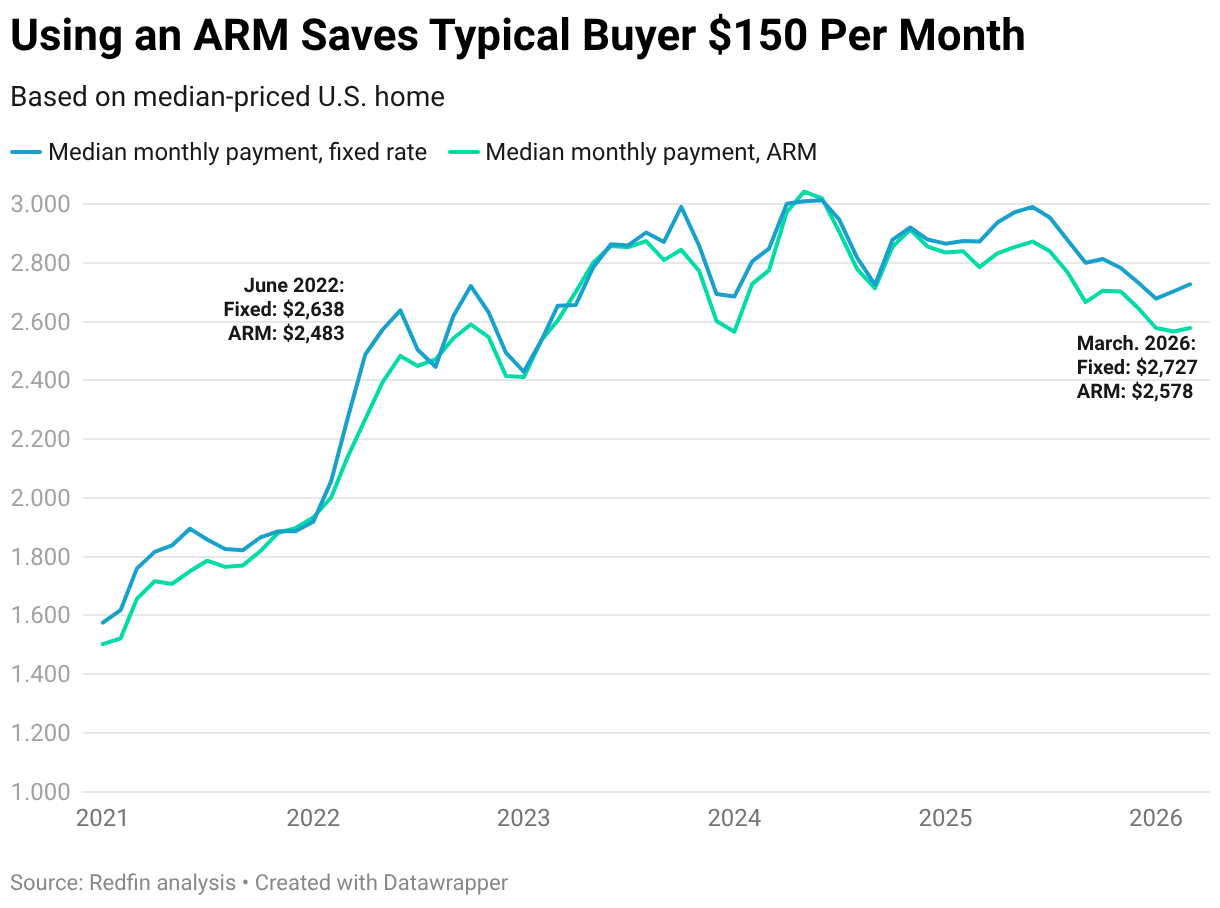

- The average rate for an ARM up until now this month is 5.51%, compared to a 6.19%average for a 30-year set rate home mortgage. The typical homebuyer utilizing an ARM takes on a monthly payment of $2,578, down 7% from last year.

- Today’s ARM discount rate is huge enough that purchasers ought to speak with their lending institution about whether it’s the right choice for them. ARMs aren’t nearly as risky as they once were; they feature interest-rate caps and defense for borrowers.

The normal homebuyer would save $150 monthly taking out a variable-rate mortgage rather of a 30-year fixed rate home loan. That’s a 5.8% discount rate, the greatest ARM users have had because June 2022 in both dollar and percentage terms.

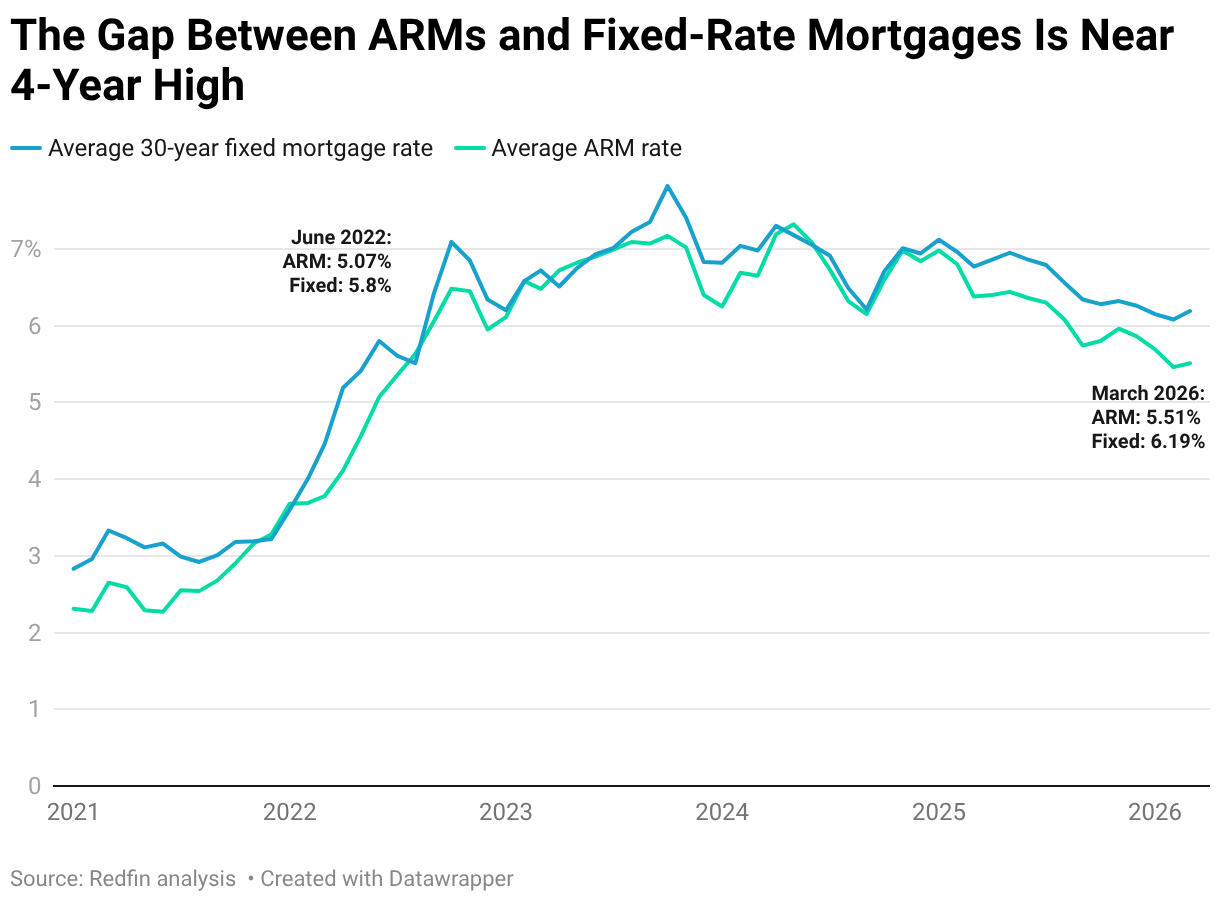

That’s due to the fact that the typical homebuyer utilizing an ARM so far in March handled a 5.51% rate, while the average buyer securing a fixed home loan had a 6.19% rate. The ARM is 0.68 basis points lower– the biggest space given that June 2022.

This is according to a Redfin analysis of 30-year set home mortgage rates compared with 7/6 ARMs since March 16, 2026. Please see the end of this report for more

on method. The typical month-to-month payment for a homebuyer using an ARM is $2,578, versus$2,727 for somebody utilizing a fixed rate.

The Typical ARM Buyer’s Housing Payment Is 7% Lower Than a Year Ago

Today’s payment for purchasers utilizing an ARM, $2,578, is down 7.4% from a year back. That’s compared to a 5% decline for fixed-rate borrowers, to $2,727.

In general, home mortgage rates are lower than they were a year earlier, bringing property buyers a little bit of relief. However rates for ARMS have declined more: Today’s typical rate for an ARM, 5.51%, is down from 6.38% a year ago; the typical 30-year fixed rate of 6.19% is down from 6.77%.

“Variable-rate mortgages are using meaningful cost savings in 2026’s expensive housing market,” stated Costs Banfield, chief organization officer at Rocket. “Despite the fact that housing costs have just recently come down a bit, it remains hard for novice purchasers to break in– and for existing property owners to walk away from their ultra-low rates. With ARMs providing borrowers with the most significant discount in nearly 4 years, picking an ARM might be a gamechanger, saving buyers hundreds of dollars monthly and thousands over a few years. ARMs generally make sense when rates are high enough that purchasers do not desire to lock them in– like now. When rates are low, like they were during the pandemic, it’s worth locking them in for as long as possible.”

The advantage of a 30-year fixed rate home loan, even when rates are relatively high, is that borrowers know exactly what their payment will be for the entire length of the loan. In today’s market, ARMs are using lower payments throughout the initial duration, however they include some unpredictability. After the initial fixed-rate duration, rates may be higher, rising month-to-month payments. Naturally, rates might likewise be lower when the seven-year period ends.

ARMs Aren’t As Risky As They Used to Be

The ARM discount rate is huge enough that buyers getting a home mortgage should talk with their lender about whether it’s an excellent choice. ARMs can be a smart strategy for debtors who plan to remain in a home only for the short term, have the financial means to manage a higher payment and/or plan to re-finance their loan later. There’s a pretty good opportunity rates will fall enough throughout the fixed-rate period that it makes sense to re-finance.

It’s also crucial for property buyers to know that ARMs are not almost as dangerous as they when were; new guidelines entered into impact after the financial crisis to secure debtors. One, ARMs include interest-rate caps, which limit just how much the rate can increase each term and over the life of the loan. 2, customers frequently need to get approved for an ARM based on a greater rate, so they usually have leftover space in their budget if the rate does increase. Also note that the common home mortgage lasts between 4 and seven years before the borrower refinances or offers, according to the National Home loan Database; frequently, a homebuyer who handles an ARM with a 7- or 10-year set rate period never even gets to the adjustable-rate duration.

Here’s more info on ARMs and 30-year fixed rate home mortgages from Rocket Home mortgage.

Methodology

This is according to a Redfin analysis of Home loan News Daily’s rates aggregated to a regular monthly average: 30-year fixed mortgage rates compared to 7/6 ARMs as of March 16, 2026.

With a 7/6 ARM, the customer pays a fixed rate of interest for the very first 7 years of the loan. In the period that follows, the borrower’s rate of interest changes every 6 months; For this report, month-to-month payments show the preliminary fixed-rate period (7 years), calculated utilizing a 30-year amortization at the initial ARM rate. After the initial period, the rate adjusts based on an index rate (a market-based recommendation rate of interest) and a margin (a number set by your lender when you get the loan); it does not change directly to a present prevailing mortgage rate. The index (frequently SOFR) moves with the marketplace, and the lender adds a fixed margin embeded in the loan terms. ARMs typically have periodic and lifetime caps that limit how much they can increase, both per term and over the life of a loan.

Total monthly housing payments are computed using mean U.S. home price, and assume a 20% down payment, 1.25% property taxes and 0.5% house owners insurance.