A slight cooling in U.S. home costs did little to ease pressure on house owners in 2025, as property taxes climbed to nearly $400 billion and effective tax rates reached their greatest level in 5 years, highlighting the growing detach in between market values and local tax problems.

New figures from ATTOM show that city governments levied $396.8 billion in property taxes on approximately 89.6 million single-family homes, a 3.7% increase from the prior year. The average tax bill increased to $4,427, up 3% from 2024, even as home worths declined modestly.

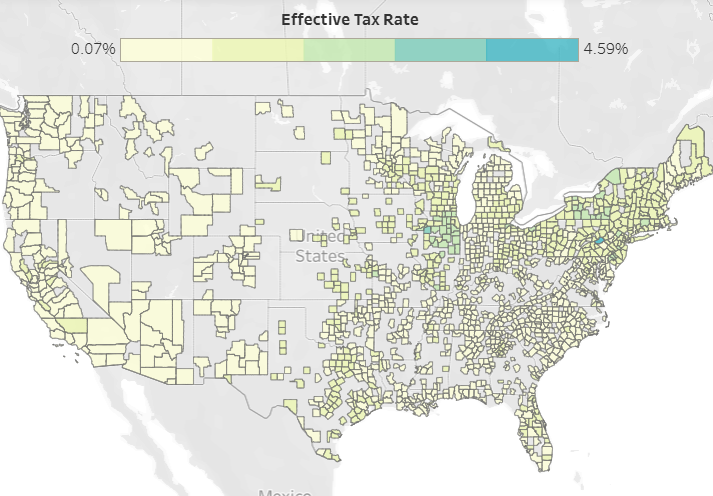

The nationwide reliable real estate tax rate increased to 0.9%, compared to 0.86% a year previously, marking the highest level given that 2020. The rise reflects a shift in the underlying characteristics of the real estate market, where tax problems are increasing in spite of softening home worths. The typical estimated worth of a single-family home fell 1.7% year over year to $494,231, though it stays near traditionally raised levels following sharp gains in prior years.

“Real estate tax are no longer relocating tandem with home rates,” stated ATTOM Chief Executive Officer Rob Barber, noting that greater tax bills integrated with declining values are pushing effective rates up and highlighting the growing influence of local government costs and policy choices.

The heaviest tax problems stay focused in the Northeast and Midwest, where older infrastructure and higher community costs continue to drive raised rates. Illinois led the nation with an efficient rate of 1.84%, followed by New Jersey at 1.58% and Vermont at 1.4%. Connecticut and Ohio were close behind, while several other states across those areas also published rates above 1.2%.

These greater rates equate into considerably larger tax expenses. Property Owners in New Jersey paid an average of $10,499 in 2025, almost 10 times the $1,081 average in West Virginia, which had the most affordable tax concern in the country. Connecticut, New Hampshire, Massachusetts, and New york city likewise ranked among the states with the highest typical expenses, each well above the national average.

By contrast, the lowest effective tax rates were mainly focused in the West and South. Hawaii published the lowest rate at 0.33%, followed by Idaho, Wyoming, Arizona, and Alabama. Numerous other states, including Utah, Delaware, Tennessee, and Nevada, also maintained reasonably low tax burdens, although sometimes those savings are balanced out by rising home rates and population growth.

At the city level, disparities are even more pronounced. Smaller sized metro areas in the Northeast and Midwest taped the highest efficient tax rates, led by Binghamton, New York City, at 2.27%, in addition to Champaign, Illinois, and Trenton, New Jersey. On the other hand, a few of the lowest rates were discovered in markets such as Knoxville, Tennessee, Salisbury, Maryland, and Honolulu, Hawaii.

Among the largest metropolitan areas, those with populations exceeding one million, Rochester, New York City, Chicago, and Buffalo posted the greatest efficient tax rates. In contrast, significant Sun Belt markets consisting of Phoenix, Nashville, Salt Lake City, and Las Vegas ranked among the lowest.

Over half of the 221 metro locations analyzed skilled real estate tax increases that surpassed the nationwide average. A few of the most significant dives occurred in Memphis, where typical tax costs rose 34%, followed by Baltimore at 27% and more moderate boosts in St. Louis, Houston, and Kansas City. The trend recommends that city governments are increasingly counting on real estate tax to balance out fiscal pressures, even as housing markets start to cool.

At the county level, the highest property tax expenses stay focused in wealthy seaside regions. Of the 26 counties where typical taxes go beyond $10,000, a disproportionate share lie in New Jersey, California, and New York. Westchester County, New York, taped the greatest average expense at $18,386, followed by Marin County, California, and a number of counties in northern New Jersey, consisting of Bergen and Essex, in addition to San Mateo County in California.

The information point to a more comprehensive structural shift in the U.S. housing landscape. Property taxes are becoming less tied to variations in home prices and more reflective of local fiscal needs. For property owners, that suggests bring expenses continue to increase even when property worths stagnate or decline– a dynamic that could have lasting implications for price, migration patterns, and housing market stability.