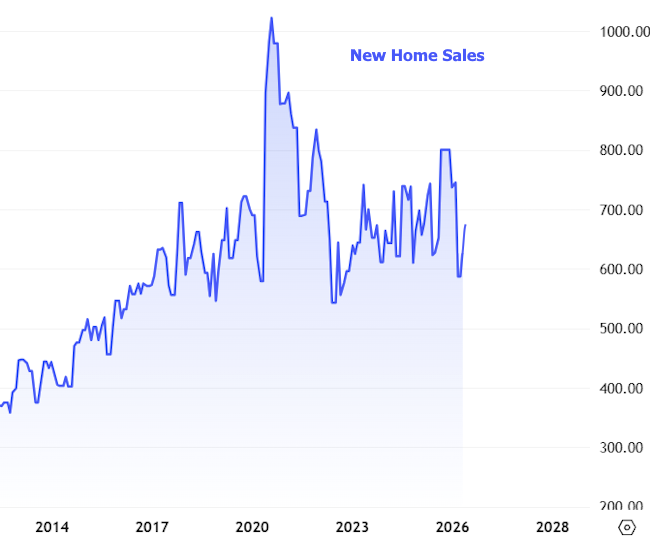

New home sales moved higher in March and February. Both months were reported on a single day today as the Census Bureau continues catching up from the government shutdown.

After dropping to 587k in January, sales increased to 635k in February and 682k in March. This represents a strong recover into the center of the broadly sideways variety that’s been undamaged for the previous 2 years.

For-sale inventory edged somewhat lower to 481,000, down 0.4% from February and 4.6% below year-ago levels. At the existing sales pace, months’ supply fell to 8.5 months, down from 9.1 months in February and 9.2 months one year earlier. The decrease reflects a mix of stronger sales and decently tighter inventory.

Prices moved lower on both a month-to-month and annual basis. The mean prices decreased to $387,400 (-5.3% MAMA; -6.2% YoY), while the average rate slipped to $503,100 (-3.4% MAMA; -1.2% YoY). The continued softness in rates suggests a shift in the mix of homes offered and continuous pressure on affordability.

- Sales (MoM): +7.4%

- Sales (YoY): +3.3%

- Stock (YoY): -4.6%

- Months’ Supply: 8.5 (below 9.1 prior month; 9.2 YoY)