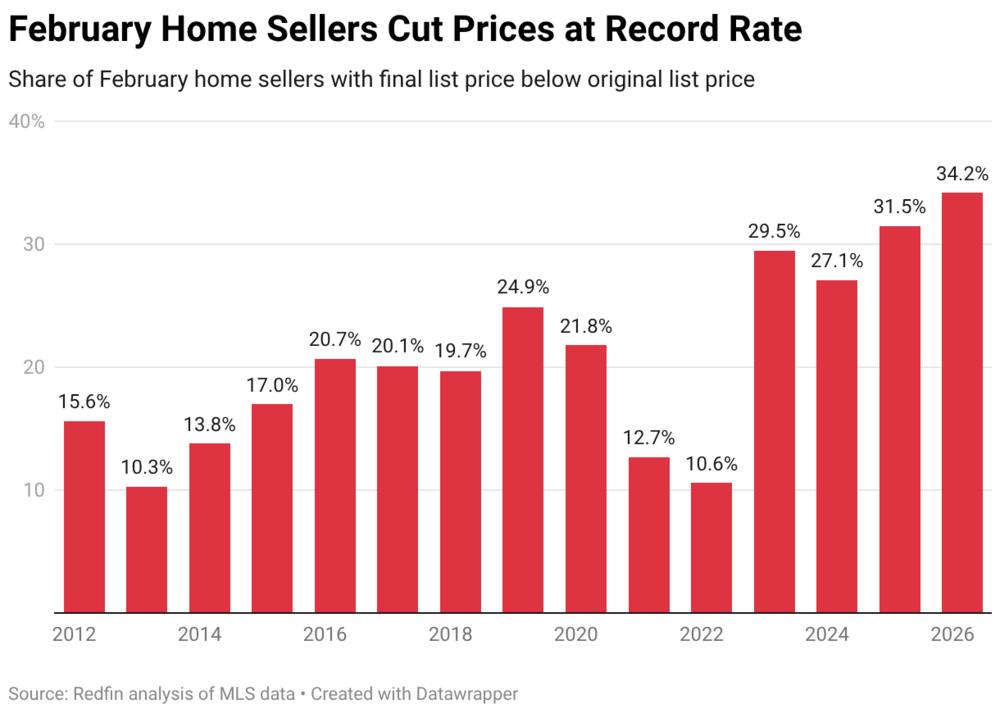

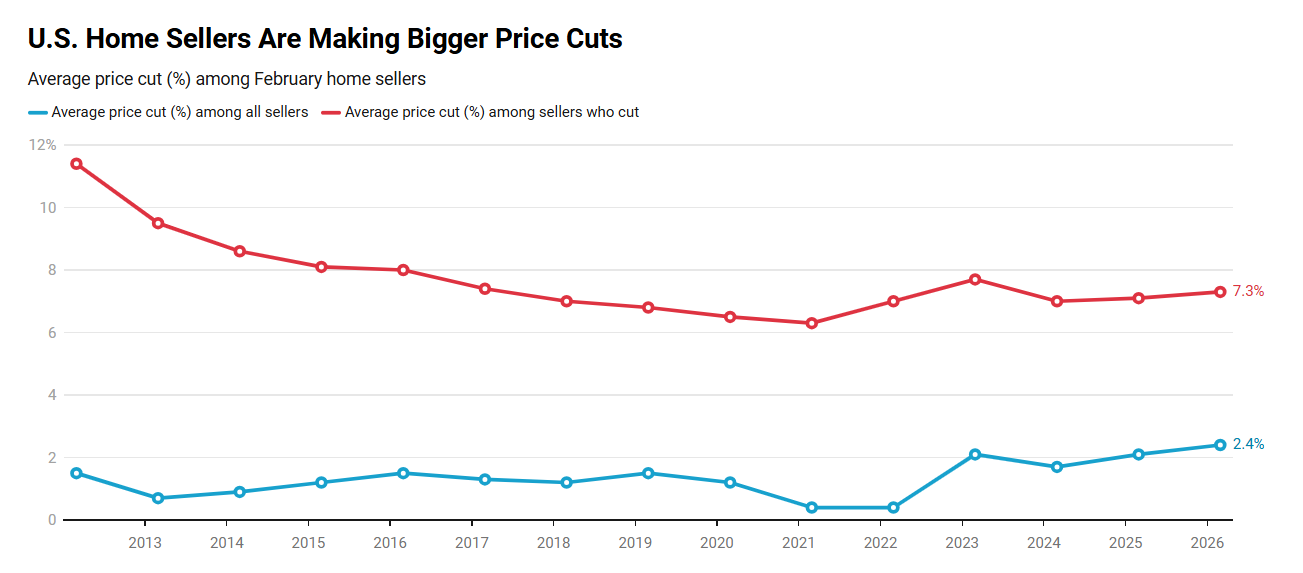

An overall of 34.2% of sellers decreased their list price during the month, up from 31.5% a year previously and the highest February share in records going back to 2012. The average decrease amongst sellers who cut costs was $40,915, or 7.3%, the largest portion decline for a February because 2023.

Across all home sales– not simply those with cost decreases– the typical seller cut related to $13,463, or 2.4% off the initial listing price, likewise a February record in percentage terms, according to the analysis of MLS information.

The findings point to a market in which raised home mortgage rates, high asking rates and broader economic unpredictability have actually compromised purchaser demand, leaving sellers with more stock competitors and less prices power.

“The market is really different in spring versus fall,” stated Aditi Jain. “Some homeowners need to move right away, but those who can manage to time the marketplace may get a much better cost.”

The data likewise reveal a rising share of sellers choosing to delist and relist homes instead of cut prices instantly. Approximately 45,000 homes formerly removed the market were relisted in January, the highest January total on record considering that 2016, according to Redfin. Experts state this technique can obscure the real occurrence of rate reductions, given that cuts made before delisting are not always caught when homes re-enter the market.

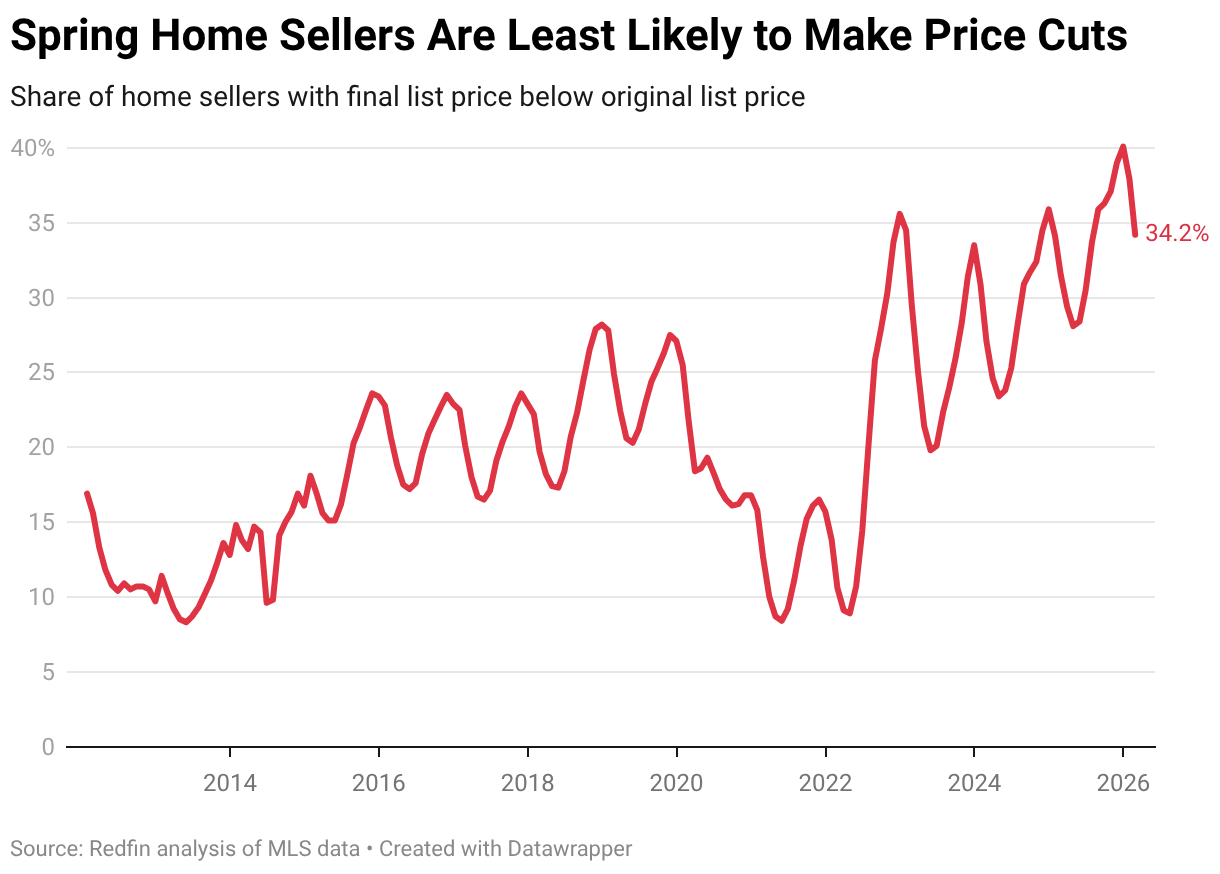

Seasonality remains a crucial consider prices behavior. Spring usually provides sellers the strongest environment to avoid reductions, with April or May producing the lowest share of price cuts in newest years, while winter– particularly December– tends to see the weakest results.

Sellers who have owned their homes for less than two years were most likely to cut costs, with 37.4% doing so in February. That compares to 34.9% among owners of two to 7 years and 31.8% for those holding homes longer than seven years.

The pattern reflects sticking around impacts of pandemic-era home purchases, when rates surged quickly in many markets. In numerous regions, subsequent rate stagnation or declines have left some recent purchasers better to breakeven or underwater, increasing pressure to adjust expectations to present market conditions.

Regional disparities were noticable. In San Antonio, 57.9% of sellers decreased asking rates, the highest share amongst major U.S. metros. It was followed by Austin, Dallas, Tampa and Fort Lauderdale– markets that have actually seen substantial brand-new construction and increasing stock levels.

Texas and Florida, in particular, have emerged as buyer-leaning markets due to elevated supply, with Florida also dealing with extra pressure from increasing insurance costs, natural catastrophe threat and higher condominium association charges.

At the other end of the spectrum, West Coast tech centers revealed far less rate reductions. In San Francisco, just 7.4% of sellers cut prices, the most affordable among major cities, followed by San Jose, Newark, Oakland and Seattle. In numerous Bay Area submarkets, pricing strategies often start below perceived market value to promote bidding wars, lowering the requirement for subsequent decreases.

The information suggest a real estate market significantly defined by divergence: softening pricing power in high-supply Sun Belt markets, and relative durability in constrained coastal cities– even as national averages point toward growing purchaser utilize.