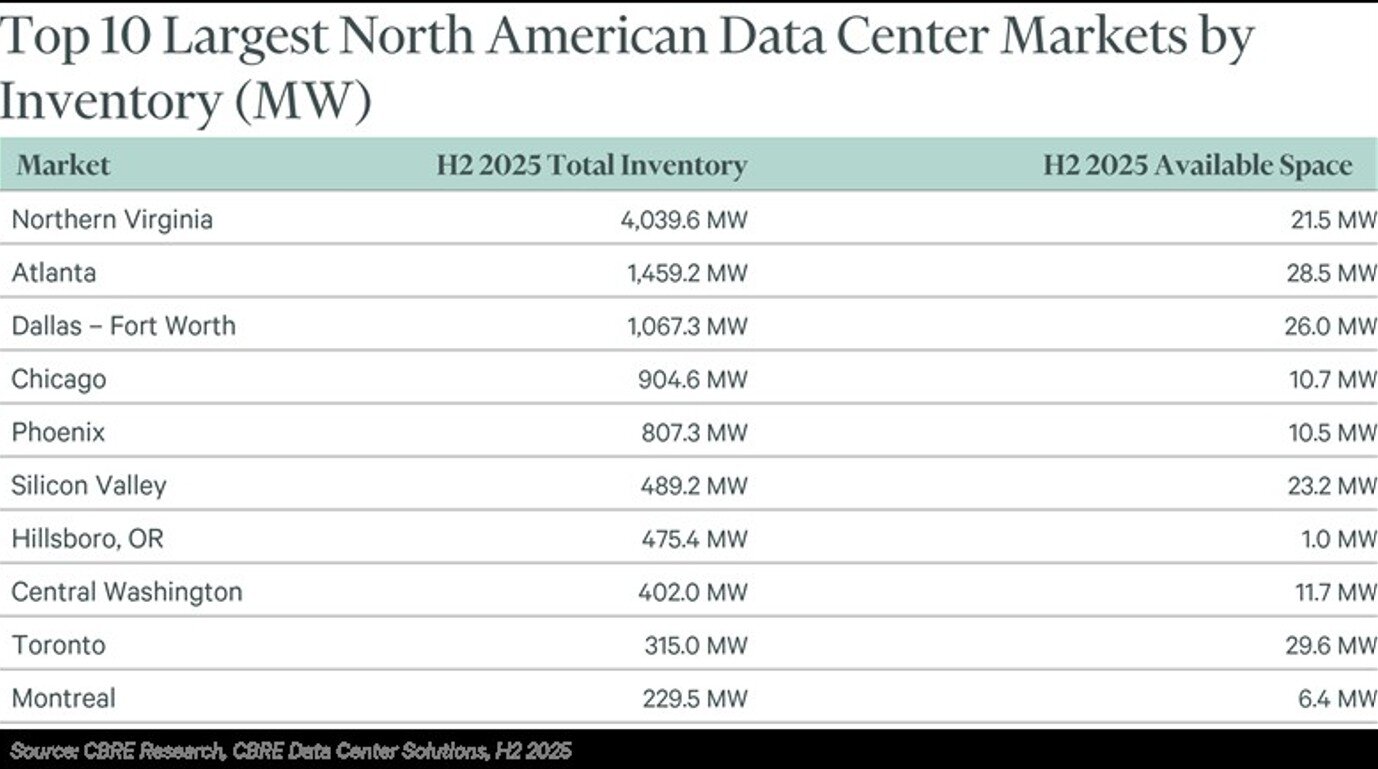

Throughout the eight primary markets, tenants took nearly 2,500 megawatts (MW) of space in 2015– a 38% increase from 2024– highlighting the quick adoption of AI-powered tools and digital services. Northern Virginia recovered its leadership position after Atlanta led in 2024, taping 1,102 MW of net absorption, more than double the previous year. Its total stock now exceeds 4,000 MW, approximately three-and-a-half times the combined capacity of all secondary U.S. markets.

“The rise in leasing throughout North America shows how rapidly company and customers are embracing AI-powered tools and digital services,” stated Pat Lynch, Executive Handling Director of CBRE Data Center Solutions. “Need is outpacing supply, while power and supply chain lacks are reinforcing a power-first approach that focuses on sites with the fastest course to power. Eventually, unlocking extra supply will depend on power availability timelines, approvals for on-site generation, and greater financial investment in transmission infrastructure.”

National job fell to 1.4% even as total capacity climbed up 36% to 9,432 MW, highlighting the speed at which recently built area is being soaked up. Lease rates rose 6.5% year-over-year to $194.95 per kilowatt per month, marking the fourth consecutive annual boost.

Building and construction activity, nevertheless, slowed for the very first time because 2020. Capacity under development fell to 5,994 MW at year-end, below 6,350 MW in 2024, as allowing delays, zoning approvals, and power restraints extended project timelines.

Emerging markets are gaining attention as operators search for land, permitting flexibility, and accessible power. “The everyday use of AI, from information analysis to personalized suggestions, needs quick reaction times and servers situated near population centers,” said Gordon Dolven, Data Center Research Study Director at CBRE. “Combined with growing interest in markets that offer available land and power, this is spurring financial investment beyond standard centers and improving the North American data center market.”

Atlanta continues to expand rapidly, with more than 2,000 MW under building and construction, while Dallas-Fort Worth ended up being the 3rd North American market to exceed 1 gigawatt of total inventory, signing up with Northern Virginia and Atlanta.

Experts say the combination of soaring AI demand, limited readily available land, and power facilities constraints is reshaping the continent’s information center landscape. Future development will hinge less on traditional real estate aspects and more on the speed at which utilities can deliver trusted electrical energy, a shift that is most likely to specify the next generation of North American information centers.