In This Post As if house rates and insurance coverage weren’t costly enough, throw soaring real estate tax in the mix, and you have the holy trinity of unaffordability, eating into cash flow like termites into unattended damp wood.

According to a current analysis by the Urban-Brookings Tax Policy Center, pointed out by CBS News, the average property tax costs in the U.S. rose 30% between 2019 and 2024. Nevertheless, there is a large disparity between states. WalletHub reports that the typical American household now pays approximately $3,119 a year in real estate tax, according to the U.S. Census Bureau, with effective rates over 8 times higher in the costlier states than in the cheapest.

Nearly 50% of the Median Income Goes to Principal, Interest, Taxes, and Insurance (PITI)

The Atlanta Federal Reserve’s Home Ownership Price Display highlighted the combined effect of rising costs. According to the findings, the median-priced home in late 2025 needed 42% of the median earnings. To put it in point of view, the typical principal interest and home loan payment with taxes, property owner’s insurance coverage, and private mortgage insurance coverage doubled in a five-year period between June 2020 and June 2025, increasing from $1,564 to $3,114– far outpacing wage development. Some cities, such as Nashville, are greater.

Doug Duncan, former chief financial expert of Fannie Mae and founder of Duncanomics, laid some of the blame at the Fed’s feet. Duncan told Bankrate:

“That function is having actually driven genuine rate of interest negative and nominal rate of interest basically to no, which brought mortgage rates down to the 3% range for a sustained time period. There was no reasonable reason rates should have been that low, that long, and even that low to start with. However the truth that rates were that low [for] that long moved a whole lot of people forward in time with an once-in-a-lifetime chance to secure an unreasonably low rates of interest. Obviously, that promoted demand, which sped up the speed of rate appreciation.”

The Vicious Circle of Rate Hikes, Low Inventory, and Skyrocketing Rates

The escalating expense of owning a rental has made the concept of attaining short-term capital as difficult as threading a needle in a cyclone. The post-pandemic rates of interest trek led to an absence of stock as prospective sellers hung on to their low rates and buyers balked at buying homes they might no longer pay for.

Consider the boost in costs, tax evaluations, and taxes, and severe weather condition was the final nail in the coffin, driving insurance coverage expenses skyward.

A Bloomberg analysis of ATTOM data found that in 2023, tax levies on single-family homes climbed up 6.9%, the greatest increase in five years, with the average property owner’s tax bill around $4,000.

Thomas Brosy, Tax Policy Center senior research study associate, composed in a September article:

“Rising home worths have amplified calls to cut or perhaps abolish the real estate tax. Because property taxes rise with home values, house owners may fear being squeezed by larger tax expenses. Those fears aren’t unfounded: The mean costs increased about 30% between 2019 and 2024– still far except soaring home worths, but with broad variation throughout states.”

Where Capital Is Under Pressure From High Taxes

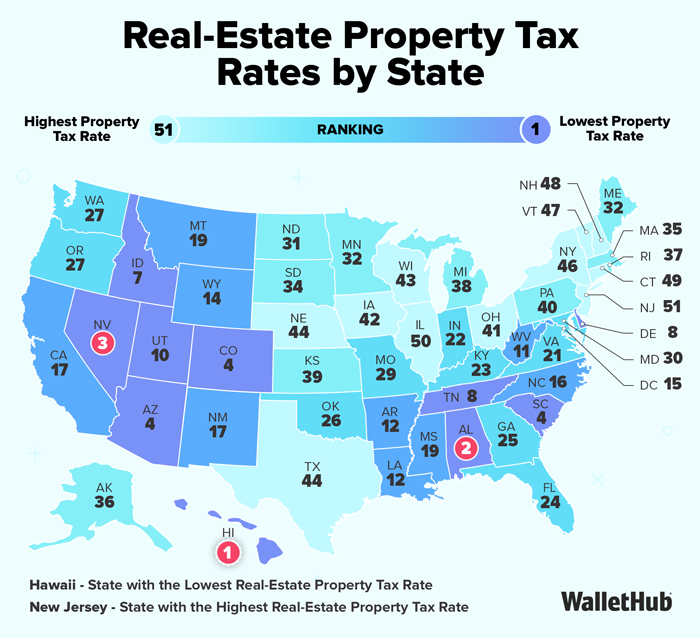

Unless you have owned a rental home in New Jersey for a very long time or bought it complimentary and clear, best of luck seeing any capital. That’s because it has the most pricey effective property tax rate in the country, followed by Illinois and Connecticut. Since early 2026, the average home price in New Jersey was $558,805, according to Zillow figures, which would imply an almost $12,000 tax bill.

By contrast, the lower real estate tax states of Hawaii and Alabama have rates in the 0.27% to 0.38% variety, putting their average yearly tax expenses at a much more workable $2,239 and $788, respectively.

The combined problem of high taxes and insurance coverage now surpasses home loan payments in numerous areas, according to a 2024 Wall Street Journal article mentioning data from Intercontinental Exchange. The continuous upward pressure on expenditures forces proprietors to raise leas, tightening up the squeeze on price.

Leading 10 states with the most affordable property taxes Hawaii: 0.27%; $2,239 typical each year

Leading 10 states with the highest property taxes

You might also like

- New Jersey: 2.11% reliable rate; average of $9,590 yearly

- Illinois: 2.01%; $5,298 annually

- Connecticut: 1.81%; $6,643 yearly

- New Hampshire: 1.66%; $6,667 annual

- Vermont: 1.59%; $5,039 yearly

- New york city: 1.55%; $6,582 yearly

- Nebraska: 1.49%; $3,549 each year

- Texas: 1.49%; $4,232 yearly

- Wisconsin: 1.42%; $3,792 yearly

- Iowa: 1.39%; $2,897 each year

Why Tax Mathematics Is Never That Simple for Financiers

It could never ever be as simple as “low taxes great, high taxes bad,” could it?

Yes, on an even playing field, low taxes would indicate more cash flow and high fives all around. Nevertheless, in the U.S., the playing field is more like the lip of a volcano, and high-tax states often have much better schools and facilities, and as a result higher leas, since more people want to live there.

Lower-tax states might depend on other profits sources, such as sales or income taxes, to money local services, which means a landlord might sustain higher costs for restoration products. In general, when lower-tax states stress school and facilities budgets, desirability drops together with rental and tenant earnings.

There are advantages and disadvantages to every market, and taxes are just part of the equation. For instance, Florida, considered a low-tax sanctuary, is not that low when it concerns real estate taxes, which have increased 9.5% per year from 2019 to 2024, as property rates climbed 14.6%, according to a report by Cotality.

Last Ideas

Numerous property managers, including me, can testify that picking a market and rental home based upon paper cash flow alone is a big error. Low taxes, insurance coverage costs, and costs, as well as good leas– what’s the catch? If something’s too good to be true, it often is.

While there are many affordable markets in the Midwest, Pennsylvania, and the South, where, in theory, it is possible to cash flow, investors need to get ready for a dip in local economies, safe and secure higher-paying jobs, and have access to a quality renter swimming pool. There is also increased turnover, as well as management and maintenance expenses.

Higher taxes do come with a trade-off, but generally it isn’t so bad– much better schools, lower crime, higher rents, and better-qualified tenants. In the existing market with interest rates, taxes, and insurance coverage at high levels, cash flow– like the penny-farthing bike and bonnets– looks like a charming idea from a bygone period.

This is the long-game period. Buy a high-quality rental in a good community at the best rate you can, for tax advantages, high demand from steady occupants, and long-lasting appreciation. Ultimately, it will start cash flowing and stacking on equity– which’s when you’ll look like a genius.