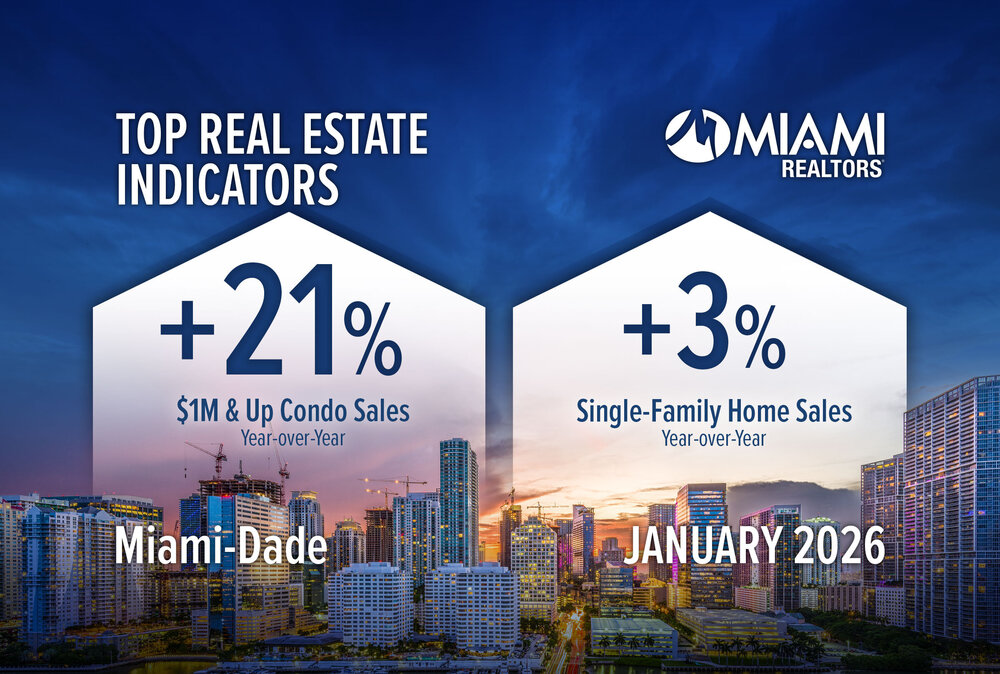

Overall residential deals increased 1.2% from a year earlier to 1,869 closings, while single-family sales climbed 2.8%– the fifth successive month of yearly gains. Condominium activity was effectively flat, down just 0.1%, underscoring a market that has held stable even as greater borrowing costs continue to weigh on price across the country.

High-end and Money Purchasers Drive Momentum

High-end need stayed a specifying feature of South Florida’s property landscape. Combined sales of homes priced at $1 million and above rose more than 21% year over year, with both single-family and condo segments posting almost identical increases.

The region continues to identify itself as the country’s most cash-intensive major real estate market. All-cash purchases accounted for 44% of January closings, far going beyond the U.S. average of roughly 27%. Industry experts say the frequency of liquidity-driven purchasers– consisting of foreign purchasers and domestic migrants moving from higher-priced cities– has insulated Miami from the complete effect of raised mortgage rates.

South Florida also kept its position as the nation’s leading ultra-luxury condo hub in 2025, tape-recording its highest-ever number of $20 million-plus condominium deals and near-record activity in the $10 million-plus tier throughout both condominiums and single-family homes.

Rates Extend Long-Term Climb Up

Home values continued their multi-year ascent. The mean price for a Miami-Dade single-family home increased 3.7% from a year earlier to $699,990, marking cost gains in 168 of the past 170 months. Considering that 2016, single-family mean values have increased more than 159%.

Condominium rates showed comparable strength. The mean condo sale price reached $420,000 in January, up from $415,000 a year ago and more than double the $205,000 level tape-recorded a years previously. Apartment prices have either held company or advanced in 163 of the previous 176 months, a streak spanning nearly 15 years.

Funding Constraints Temper Condominium Benefit

Regardless of stable sales, structural financing constraints continue to limit condominium momentum. Fewer than 1% of condominium structures across Miami-Dade, Broward, and Palm Beach counties are currently authorized for Federal Real estate Administration loans, according to federal housing information. Florida’s more stringent reserve and down-payment requirements for non-approved structures– often mandating 25% down versus 10% in most other states– further narrow the buyer swimming pool.

Supply Still Below Pre-Pandemic Levels

Inventory conditions remain tighter than historical norms even as listings have inched greater. Active property listings totaled 17,942 at the end of January, up 5.6% from a year earlier but still roughly 25% listed below pre-pandemic 2019 levels.

Single-family supply increased 9% year over year to 5,433 homes, translating to a 6.4-month stock– broadly thought about a balanced market. Condo listings increased 4.2% to 12,509 systems, representing a 13.7-month supply and tilting negotiating utilize towards buyers. Nationally, unsold housing inventory stands at a 3.7-month supply, according to the National Association of Realtors.

Dollar Volume and Building And Construction Signal Underlying Strength

Overall dollar volume of Miami-Dade residential transactions jumped 13% from a year earlier to $1.6 billion. Single-family volume rose 15.6% to $936 million, while condo volume advanced 10.3% to $638 million.

Beyond resale activity, Southeast Florida leads the U.S. in multifamily building and construction, with more than 36,000 units underway since late 2025. Developers and policymakers point to the state’s Live Local Act– which grants density rewards to tasks designating 40% of units to workforce real estate– as a prospective long-term catalyst for cost.

Distress Near Historic Lows, Settlements Lengthen

Signs of financial stress remain restricted. Distressed residential or commercial properties, consisting of bank-owned homes and short sales, represented simply 2% of January closings, compared with roughly 70% at the height of the foreclosure crisis in 2009.

Homes are still selling near asking prices, though marketing times have actually extended modestly. Sellers of single-family homes received a typical 94% of initial list price, while condominium sellers caught 93%. The typical single-family home spent 53 days on the market before contract, versus 71 days for condos, both a little longer than a year earlier.

Global Worth Proposition Sustains

In spite of rapid appreciation, Miami continues to compare positively with other worldwide gateway cities on a price-per-square-meter basis. Wealth reports show that $1 million buys considerably more prime residential space in Miami than in markets such as Monaco, New York, or London– a differential that analysts state assists sustain worldwide need.

Taken together, January’s information illustrate a market identified less by speculative surge than by stable, liquidity-supported development: high-end demand stays robust, supply restraints persist, and price appreciation continues– albeit at a more measured pace than the post-pandemic boom years.