Americans are retiring later than they used to, and housing rates might be playing a role.In practically every state, the share of seniors ages 65 and older still in the workforce has actually grown given that 2014, according to an analysis of Census Bureau American Community Survey data by Realtor.com ®.

The pattern is concentrated in some of the most costly housing markets, indicating how rising housing costs (like insurance coverage, real estate tax, and maintenance) might be putting pressure on older property owners to stay in the task market longer.

But Hannah Jones, senior economic research analyst at Realtor.com, states the pressure runs both ways.As continued employment permits more would-be retirees to carry these expenses, it’s keeping stock secured and increasing home rates in addition to it.

“The possibility of selling typically produces less financial relief than expected when the option is buying smaller sized at current prices and rates, and the social expense of relocating is high,” she states. “The outcome is inventory being held back the marketplace by a section of owners who, in a different rate environment, would likely have actually transacted by now.”

Why the 65-plus workforce is outpacing population growth

Over the last decade, the variety of utilized elders (age 65 and older) has actually escalated by 52%– greatly exceeding the wider population growth of simply 33%, according to the data.

That mirrors a broader group shift as life expectancies have increased. Today, a 65-year-old is anticipated to live two more years. In the 1960s, it was closer to 15 more years, according to data from the Social Security Administration.It also mirrors a rise in real estate expenses. Given that 2014, the median price of a home has increased over 60%.

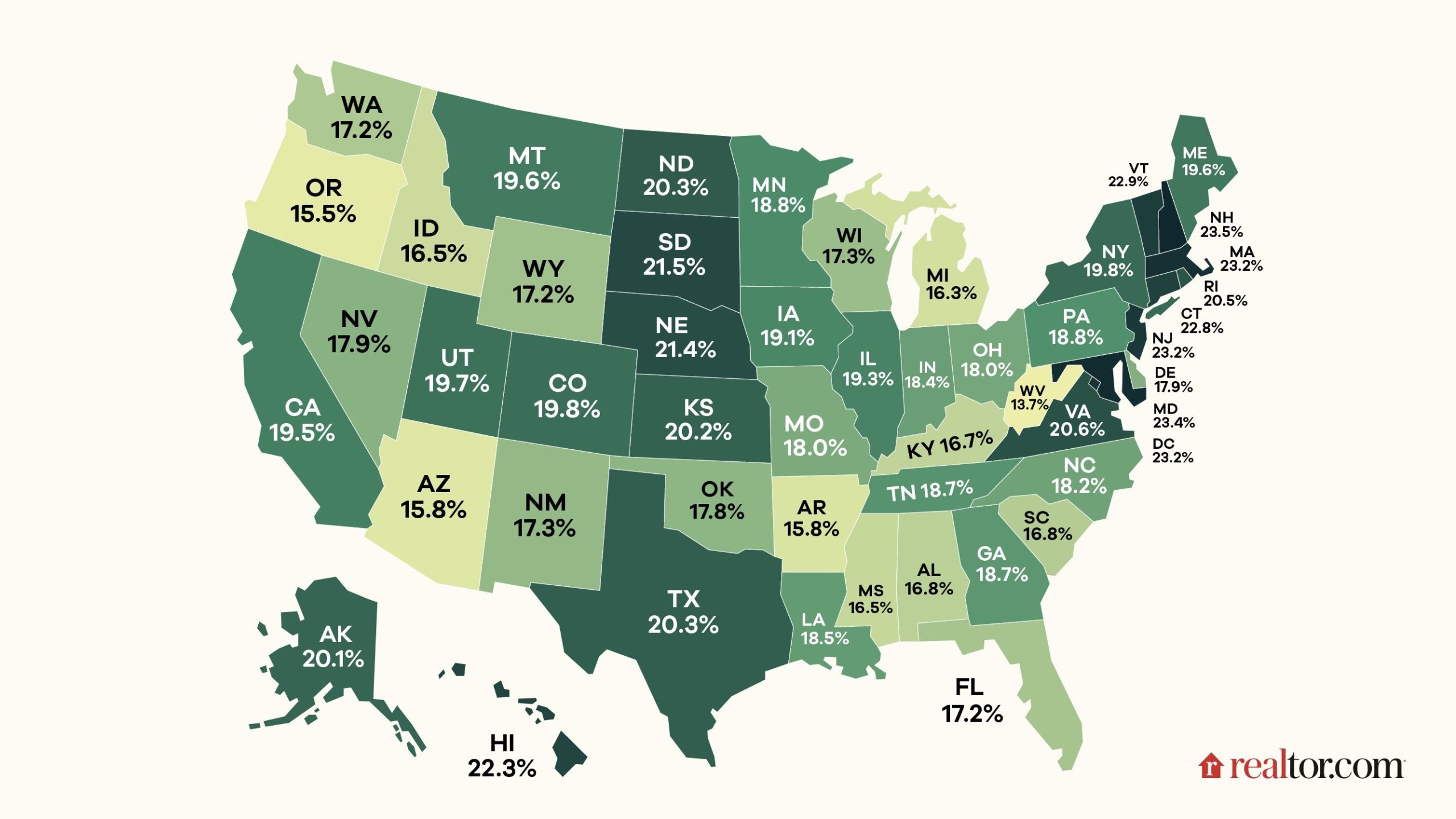

The Northeastern price trap

The Northeast boasts the highest senior labor force participation rate in the country at 21%. The region likewise represents half of the top 10 states with the highest share of elders who currently have a job.New Hampshire takes the leading spot with nearly 24% of senior citizens still working, while Massachusetts, New Jersey, Vermont, Rhode Island, and Connecticut all follow closely behind.The Northeastern corridor is likewise possibly the most plain example of how home costs can put pressure on retirement ages and vice versa.”Regionally, this shows up most clearly in

supply-constrained seaside metros where tight stock, aging ownership demographics, and strong rate floors tend to appear together, “states Jones.To her point, home rates rose 73 %in the region from 2014 to 2024. In New Jersey, it was closer to 80%, and in Massachusetts, home prices increased 90%. Why senior work is dropping in Frontier states While almost every state in the country saw a higher portion of their senior citizens working in 2024

compared with 2014, 6 states bucked the pattern entirely.Wyoming and Alaska provide the most stark drops. The Cowboy State saw the share of senior citizens 65 and older with a job drop over 4 portion

points, while the Last Frontier State saw a drop of just under that threshold.It might be owed to the dominant industries in these states. Unlike the service or understanding economies of the Northeast where remote work or desk tasks abound, it can be much more difficult to age into the labor force when jobs are dominated by heavy market and extreme climates.The Sun Belt paradox States like Florida and Arizona have long been the gold requirement for a leisurely retirement, and the data backs it up– seniors there have some of the most affordable labor market participation.During the pandemic,

these markets ended up being magnets for equity-rich senior citizens looking for a modification of speed– and that sent costs skyward, Jones states. From 2014 to 2024, home rates leapt 89 %in the region.In hot spots, the change was much more remarkable. In Florida, for instance, home costs surged 138%, and in Arizona, they rose 126%. That pressure is beginning to alter, however, Jones states. “We are now seeing some of that inventory return as that population ages out of independent living and new construction activity props up supply, contributing to the buyer-market conditions noticeable in those cities today,”she says.Texas is an interesting outlier.

Home costs there increased 74%, and its senior employment share leapt from 18.1% in 2014 to 20.3 %in 2024. While that 2.2-point dive appears modest compared with the Northeast, the scale is enormous: The raw number of working senior citizens in Texas took off by 66.9%. As real estate expenses keep possible retirees on the clock and their homes off the market, the American labor force is most likely to continue to move. That might indicate that the golden years are no longer defined by stepping away from work, however by financing the high rate of sitting tight.