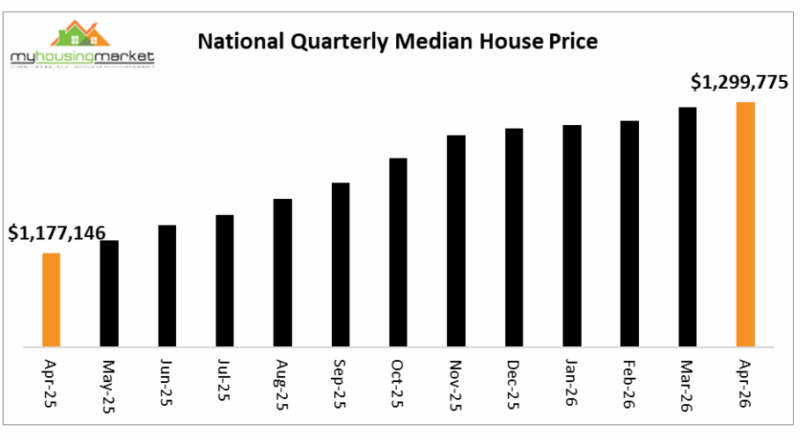

Secret takeaways Capital city home prices have actually continued to increase over April despite greater interest rates and the ongoing unpredictability over the outlook for inflation and the global economy. Development rates nevertheless have actually reduced, reflecting also the normal subduing impact of the prolonged April vacation month The nationwide capital city mean home cost increased partially by 0.3% over the April quarter to $1,299,775 compared to the March quarter, according to the most recent data from My Housing Market.

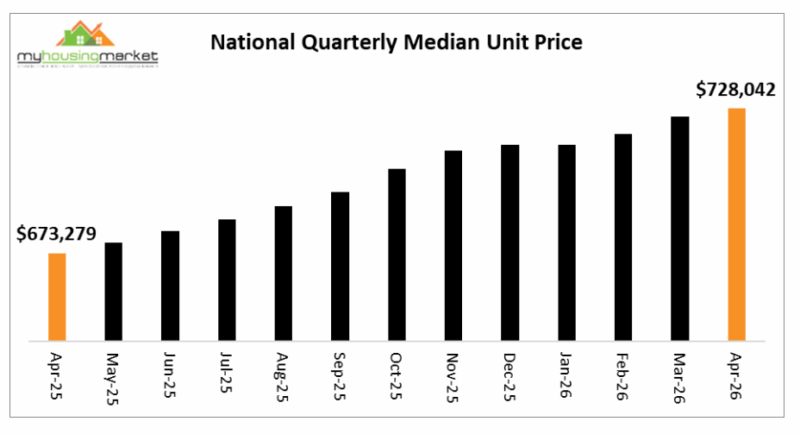

National unit rates were also higher over the April quarter compared to the March quarter, rising by 0.4% to $728,042– and have now increased by 8.1% compared to the April quarter 2025 result.

Brisbane was the top monthly performer over April with unit prices rising by 1.4% followed by Perth and Melbourne each up 1.0%, Canberra greater by 0.9%, Adelaide higher by 0.4% and Hobart up 0.2%. Sydney system costs however were down marginally by 0.1% over the month with Darwin falling 0

Capital city home prices have actually continued to increase over April despite higher interest rates and the continued uncertainty over the outlook for inflation and the worldwide economy.

Growth rates nevertheless have actually relieved, showing also the usual subduing impact of the lengthy April holiday month

The nationwide capital city median house cost increased marginally by 0.3% over the April quarter to $1,299,775 compared to the March quarter, according to the current information from My Real estate Market.

Annual nationwide home costs are however greater by 10.4% and have actually now increased over 14 consecutive months.

Most capitals reported house price boosts over the month with Perth the top entertainer greater by 1.5%followed by Darwin up 1.4 %, Brisbane and Hobart each greater by 1.2%, Adelaide up 0.3%and Sydney higher by 0.1%. Melbourne rates fell 0.4 %with Canberra down 1.8%. Most capitals continue to report strong yearly home rate growth in excess of 10 %, with Perth, Darwin, Brisbane, and Adelaide clearly the greatest, up by 26.0%, 22.8%, 19.9% and 14.3 %respectively.

| Quarterly Median Home Rates | April 2026 | Typical | Month This Year 1 Year | ||

| 2 Year Sydney | $1,777,307 | 0.1% | 0.2% | 6.0% | 9.4% |

| Melbourne | $1,101,207 | -0.4% | -1.8% | 3.7% | 2.7% |

| Brisbane | $1,218,336 | 1.2% | 4.5% | 19.9% | 30.2% |

| Adelaide | $1,141,540 | 0.3% | 3.9% | 14.3% | 26.5% |

| Perth | $1,215,261 | 1.5% | 8.6% | 26.0% | 42.2% |

| Hobart | $764,020 | 1.2% | 1.9% | 11.6% | 12.9% |

| Darwin | $803,763 | 1.4% | 5.7% | 22.8% | 25.3% |

| Canberra | $1,023,725 | -1.8% | 1.6% | 7.2% | 6.5% |

| National | $1,299,775 | 0.3% | 1.7% | 10.4% | 15.1% |

National system costs likewise higher

National unit prices were likewise greater over the April quarter compared to the March quarter, rising by 0.4% to $728,042– and have now increased by 8.1% compared to the April quarter 2025 result.

Brisbane was the top month-to-month performer over April with system costs increasing by 1.4%followed by Perth and Melbourne each up 1.0 %, Canberra higher by 0.9%, Adelaide higher by 0.4 %and Hobart up 0.2%. Sydney unit rates nevertheless were down partially by 0.1% over the month with Darwin falling 0.3%.

Quarterly Median System Costs April 2026

| Median | Month | This Year | 1 Year | 2 Year | |

| Sydney | $817,241 | -0.1% | 1.0% | 4.2% | 6.3% |

| Melbourne | $591,720 | 1.0% | -1.1% | 4.8% | 3.2% |

| Brisbane | $775,661 | 1.4% | 9.2% | 27.5% | 51.7% |

| Adelaide | $624,578 | 0.4% | -0.8% | 12.7% | 30.6% |

| Perth | $690,820 | 1.0% | 11.4% | 30.2% | 51.9% |

| Hobart | $574,218 | 0.2% | 7.1% | -0.7% | 15.3% |

| Darwin | $436,974 | -0.3% | 1.8% | 11.8% | 22.2% |

| Canberra | $504,707 | 0.9% | -0.6% | 0.6% | -2.5% |

| National | $728,042 | 0.4% | 1.9% | 8.1% | 12.2% |

Similar to houses, Perth, Brisbane, Adelaide and Darwin continue to tape-record clearly the highest yearly system price development to April 2026. up by 30.2%, 27.5%, 12.7% and 11.8% respectively.

Capital city housing markets have normally reported greater home costs over April although rates of growth have actually relieved compared to March.

Relieving housing markets reflect the typical subduing effects of the prolonged April vacation month although greater rates of interest and increased unpredictability over the economic outlook have impacted cost and confidence.

Robust annual home rate development however continues for a lot of capitals with Perth, Darwin, Brisbane, and Adelaide still reporting boomtime results.

Although 2026 is set to continue to produce home rate development usually for a lot of capitals, the rising spectre of further rate of interest increases and elevated unpredictability over the outlook for inflation and the economy will act to continue to dampen price and self-confidence.

Brisbane, Adelaide, Perth and Darwin nevertheless are again set to lead capital city outcomes for both houses and systems – but unlikely to match the amazing 2025 results.

Brisbane, Perth and Adelaide continue to tape greater average house rates than Melbourne, with Perth now closing in fast on Brisbane and set to lead all but Sydney.

Underlying drivers will continue to support overall real estate market activity, although the outlook for RBA interest rates is more problematic, with inflation set to speed up and economic activity to decrease as a consequence of the current sharp boost in oil rates.

The economy nevertheless presently stays strong with a steady and still-low jobless rate and including falling jobless, continued robust jobs development and a high participation rate.

Real estate need continues to outmatch low and decreasing real estate supply and although high post-COVID migration levels have actually clearly alleviated recently, numbers stay strong and will add to chronic housing undersupply supporting high rents and low vacancy rates usually in capital city rental markets. Following a period of relieving rental development, the latest data continues to report extraordinarily low home rental job rates and predictable signs that leas are on the increase again.

High leas and greater costs continue to supply clear incentives for first home purchasers and investors chasing solid financial investment returns. Ongoing government initiatives to support first home buyers will increase need and act to put more upward pressure on costs.

Capital city real estate markets usually tape-recorded greater home and unit prices over 2023, 2024 and surged over 2025 sustained by increasing purchaser and seller self-confidence through sharp cuts to rates of interest.

Although 2026 is once again still likely to report greater home costs, substantial uncertainty has actually just recently emerged over the near-term future for already greater interest rates and financial activity that will normally dampen purchaser and seller confidence– with early indications emerging with current weakening home auction market clearance rates, particularly in Sydney and Melbourne.

< img alt="Andrew Wilson" src="https://propertyupdate.com.au/wp-content/uploads/2018/02/cropped-Ahmad-Imam-square-wide-lo-rez-400.jpgDR-ANDREW-WILSON-148x148.jpg" height="148" width="148"/ >